Dollar is trading with a slightly firmer tone in quiet Asian session. But overall, most major pairs and crosses are stuck inside Friday’s range. Trading would likely remain subdued with Japan and UK on holiday, and the calendar is light. Nevertheless, the week ahead is ultra busy with four central bank meetings and some important economic data too.

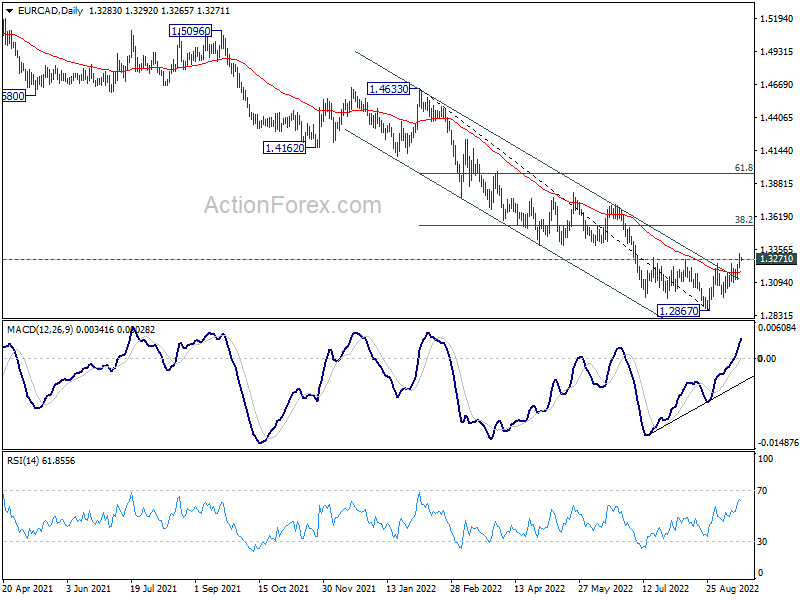

Technically, Euro has made nice bounces in some crosses, on expectation of hawkish ECB. EUR/CAD’s break of 1.3271 resistance confirmed short term bottoming at 1.2867, on bullish convergence condition in daily MACD. The break above 55 day EMA, as well as the falling trend line resistance argues that it’s at least correcting the decline from 1.4633. Further rally is in favor back to 38.2% retracement from 1.4633 to 1.2867 at 1.3542. Such development could help cushion any decline in EUR/USD.

In Asia, Japan is on holiday. Hong Kong HSI is down -0.99%. China Shanghai SSE is down -0.21%. Singapore Strait Times is down -0.09%.

ECB Lane: Tightening is not pain free

ECB Chief Economist Philip Lane said in a conference over the weekend, monetary tightening is “going to dampen demand”, and “we’re not going to pretend this is pain free”.

“Demand is now a source of inflation pressure, it was not six or nine months ago in the same way it now is,” he added.

While rate hikes could continue at each remaining meeting of the year, and extend to early next year, Lane said ECB is open mind on where to stop with a meeting-by-meeting approach.

On the economy, Lane said separately in an RTE interview, “If we think our base case is to barely grow, a technical recession – falling into a mild recession – cannot be ruled out.”

Bundesbank Nagel: We have to be determined, in October and beyond

Bundesbank President Joachim Nagel said on Sunday, “If the data trend continues, more interest-rate increases have to follow — that’s already agreed in the Governing Council. We have to be determined, in October and beyond.”

Nagel added that interest rates are still “somewhat off the levels” to curb inflation. “We must bring inflation back under control,” he said. “We mustn’t let up, even if the economy worsens.”

On the German economy, he said that momentum will likely slow in Q3 and Q4, but he’s confident that it could avoid a steep slump.

NZ BusinessNZ services rose to 58.6, bouncing for how long?

New Zealand BusinessNZ Performance of Services Index rose from 54.4 to 58.6 in August. Looking at some details, activity/sales rose from 54.4 to 67.1. Employment rose from 49.3 to 50.8. New orders/business rose from 53.4 to 66.5. Stocks/inventories rose from 53.8 to 59.6. Supplier deliveries rose from 47.6 to 49.6.

BNZ Senior Economist Doug Steel said that “overall, combining August’s strong PSI with last week’s firmer PMI yields a composite index (PCI) that suggests annual GDP growth up toward 5% in Q3 2022. We currently forecast 5%+ for that period but that strength is mostly a function of the very weak base period. If the PCI is truly bouncing, the key question is for how long?”

Fed, SNB and BoE to hike, BoJ to stand pat

Four central banks will meet this week. Fed is expected hike by another 75bps to 3.00-3.25%. There is some speculation of a 100bps hike, but Fed is unlikely to push the panic button and do that. The new economic projections and dot plot will also be released. Some hawkish surprise could be seen there, which indicates higher terminal rate for current cycle, and a longer period to stay there.

BoJ is expected to stay firmly on hold on monetary policy. Governor Haruhiko Kuroda might reiterate that rapid, one-sided depreciation in the exchange rate is undesirable, but nothing more. SNB is expected to joint the 75bps hike club, and lift interest rate back to positive at 0.50%. SNB will also repeat that appreciation of the Swiss Franc is welcome for now, as it helps curb imported inflation. BoE is expected to deliver another 50bps hike to 2.25%. Given that the UK economy is already in recession, there could be dovish surprises in the voting.

Other central bank activities include release of RBA minutes and ECB monthly bulletin. On the data front, Canada CPI and retail sales will catch much attention, together with PMIs from Australia, Eurozone, UK and the US.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ services; Canada IPPI, RMPI; US NAHB housing index.

- Tuesday: Japan CPI; RBA minutes; Swiss trade balance, SECO economic forecasts Germany PPI; Eurozone current account; Canada CPI, US building permits and housing starts.

- Wednesday: UK public sector net borrowing, CBI industrial order expectations; US existing home sales, FOMC rate decision.

- Thursday: New Zealand trade balance; BoJ rate decision; SNB rate decision; ECB monthly bulletin; BoE rate decision; Canada new housing price index; US jobless claims, current account, consumer confidence.

- Friday: Australia PMIs; Eurozone PMIs; UK PMIs; Canada retail sales; US PMIs.

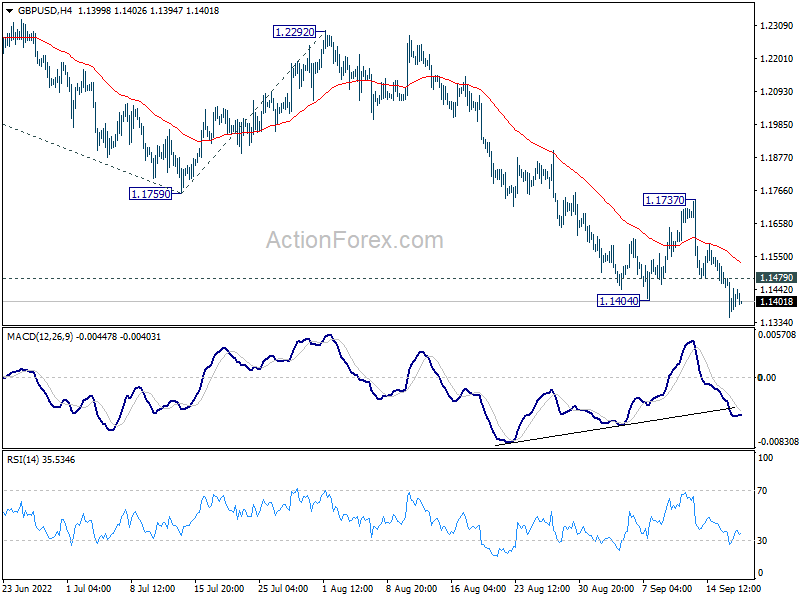

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1355; (P) 1.1418; (R1) 1.1485; More…

Intraday bias in GBP/USD stays on the downside this week. Current down trend should target 61.8% projection of 1.3748 to 1.1759 from 1.2292 at 1.1063. On the upside, above 1.1479 minor resistance will turn intraday bias neutral first. But break of 1.1737 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

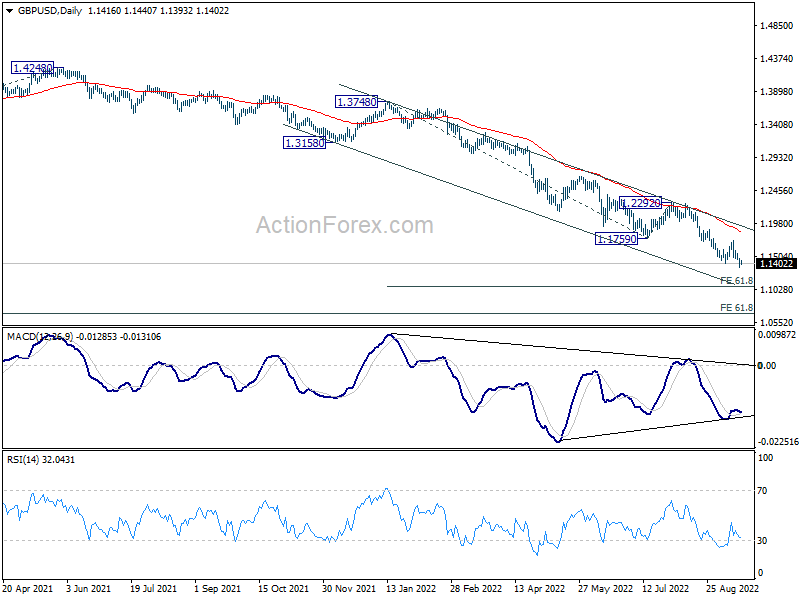

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) is probably resuming long term down trend from 2.1161 (2007 high). Sustained break of 1.1409 will target 61.8% projection of 1.7190 (2014 high) to 1.1409 (2020 low) from 1.4248 (2021 high) at 1.0675. This will remain the favored case for now as long as 1.2292 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 58.6 | 51.2 | 54.4 | |

| 10:00 | EUR | German Buba Monthly Report | ||||

| 12:30 | CAD | Industrial Product Price M/M Aug | 0.20% | -2.10% | ||

| 12:30 | CAD | Raw Material Price Index Aug | 3.20% | -7.40% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 48 | 49 |

{kind=link}