Dollar rises broadly in early US session. Stubbornly high inflation reading might be a factor. But the recovery could also be due to traders paring their positions ahead of the weekend, and next week’s FOMC. Yen is back under some broad based pressure but stays in familiar range. European stocks are mixed, and so are US futures. Markets might start to turn quieter before close.

In Europe, at the time of writing, FTSE is down -0.32%. DAX is down -0.35%. CAC is up 0.04%. Germany 10-year yield is up 0.194 at 2.156. Earlier in Asia, Nikkei dropped -0.88%. Hong Kong HSI dropped -3.66%. China Shanghai SSE dropped -2.21%. Singapore Strait Times rose 1.46%. Japan 10-year JGB yield dropped -0.0110 to 0.242.

US PCE price index unchanged at 6.2% yoy, core CPI rose to 5.1% yoy

US personal income rose 0.4% mom or USD 78.9B in September, above expectation of 0.3% mom. Spending rose 0.6% or USD 113.0B, above expectation of 0.4% mom.

Headline PCE price index rose 0.3% mom, while core PCE price index rose 0.5% mom. Prices for goods dropped -0.1% mom while prices for services rose 0.6% mom. Food prices increased 0.6% mom and energy prices dropped -2.4% mom.

From the same month a year ago, PCE price index was unchanged at 6.2% yoy, above expectation of 5.8% yoy. Core PCE price index rose to 5.1% yoy, up from 4.9% yoy, below expectation of 5.2% yoy. Prices for goods rose 8.1% yoy while prices for services rose 5.3% yoy. Food prices rose 11.9% yoy and energy prices rose 20.3% yoy.

Canada GDP grew 0.1% mom in Aug, above expectations

Canada GDP rose 0.1% mom in August, above expectation of 0.0% mom. Services-producing industries grew 0.3% mom but goods-producing industries contracted -0.3%). 14 of 20 industrial sectors grew.

Advance information indicates that GDP growth continued in September by 0.1% mom. With that, GDP growth reached 0.4% in Q3.

Eurozone economic sentiment dropped to 92.5, EU down to 90.9

Eurozone Economic Sentiment Indicator fell from 93.6 to 92.5 in October. Industrial confidence dropped form -0.3 to -1.2. Services confidence dropped from 4.4 to 1.8. Consumer confidence improved from -28.8 to -27.6. Retail trade confidence rose from -8.4 to -6.9. Construction confidence rose from 1.8 to 2.6. Employment Expectations Indicator dropped from 106.6 to 104.9.

EU Economic Sentiment Indicator dropped from 92.4 to 90.9. Amongst the largest EU economies, the ESI fell in Germany (-1.0) and Italy (-0.9), while it remained essentially unchanged in the Netherlands (-0.3) and France (0.0) and improved in Poland (+0.4) and Spain (+1.4).

Germany GDP grew 0.3% qoq in Q3, avoided contraction

Germany GDP grew 0.3% qoq in Q3, much better than expectation of -0.2% qoq contraction. The economy finally exceeded pre-pandemic level in Q4 2019 for the first time.

Destatis said, “The German economy managed to hold its ground despite difficult framework conditions of the global economy, with the continuing Covid-19 pandemic, supply chain interruptions, rising prices and the war in Ukraine. The economic performance in the third quarter of 2022 was mainly based on private consumption expenditure.”

France GDP growth slowed to 0.2% qoq in Q3

France GDP growth slowed to 0.2% qoq in Q3, matched expectations. That compares to 0.5% qoq growth in Q2.

Final domestic demand (excluding inventories) contributed positively to GDP growth this quarter (+0.4%). Thus, gross fixed capital formation (GFCF) accelerated strongly after an already relatively dynamic start to the year (+1.3%), while household consumption expenditure were stable (+0.0%). Foreign trade contributed negatively to GDP growth (-0.5%),

Swiss KOF dropped to 90.9, economic outlook remains subdued

Swiss KOF Economic Barometer decreased from 93.8 to 90.9 in October, below expectation of 93.0. The index is now below its long-term average for the sixth month in a row. Outlook for the economy in the coming months “remains subdued”.

KOF said: “The downward movement of the barometer is primarily driven by bundles of indicators from the manufacturing as well as the accommodation and food service activities sectors. Indicators for the construction sector, the financial and insurance services, and private consumption remained almost unchanged compared to the previous month. By contrast, indicators for the sector other services showed a slightly positive trend.”

BoJ stands pat, maintains yield cap at 0.25%

BoJ left monetary policy unchanged as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. 10-year JGB yield is kept at around 0%, with bond purchases without upper limit. 0.25% fixed rate purchase operation will continue to be held to cap 10-year JGB yield. The decision was unanimous.

In the new economic projections:

- Fiscal 2022 GDP growth forecast was downgraded from 2.4% to 2.0%.

- Fiscal 2023 GDP growth forecast was downgraded from 2.0% to 1.9%.

- Fiscal 2024 GDP growth forecast was upgraded from 1.3% to 1.5%.

- Fiscal 2022 CPI core forecast was upgraded from 2.3% to 2.9%.

- Fiscal 2023 CPI core forecast was upgraded from 1.4% to 1.6%.

- Fiscal 2024 CPI core forecast was upgraded from 1.3% to 1.6%.

- Fiscal 2022 CPI core-core forecast was upgraded from 1.3% to 1.8%.

- Fiscal 2023 CPI core-core forecast was upgraded from 1.4% to 1.6%.

- Fiscal 2024 CPI core-core forecast was upgraded from 1.5% to 1.6%.

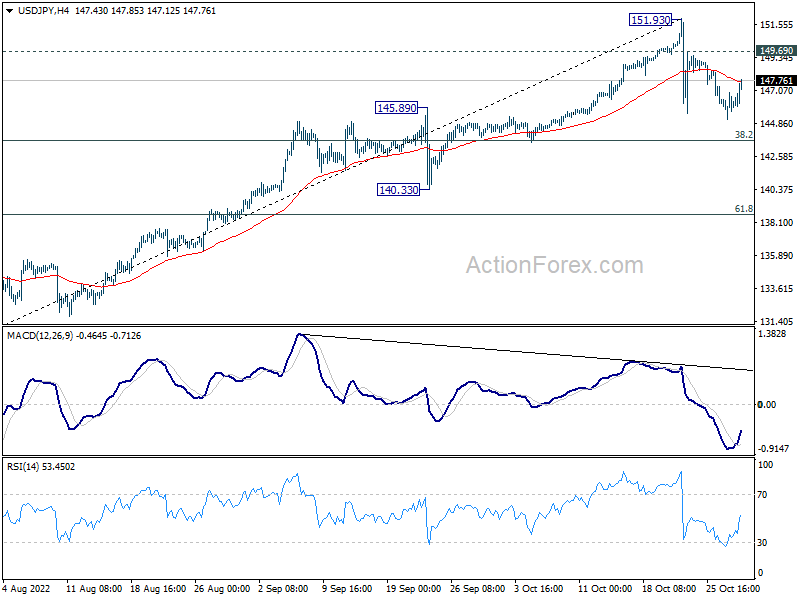

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.62; (P) 147.01; (R1) 147.80; More…

USD/JPY recovers in early US session but outlook is unchanged. Intraday bias stays neutral as corrective pattern from 151.93 would extend. Deeper pull back cannot be ruled out, but downside is expected to be contained by 38.2% retracement of 130.38 to 151.93 at 143.69 to bring rebound. On the upside, above 149.69 minor resistance will bring stronger rebound back towards 151.93 high. But upside should be limited there to continue the corrective pattern.

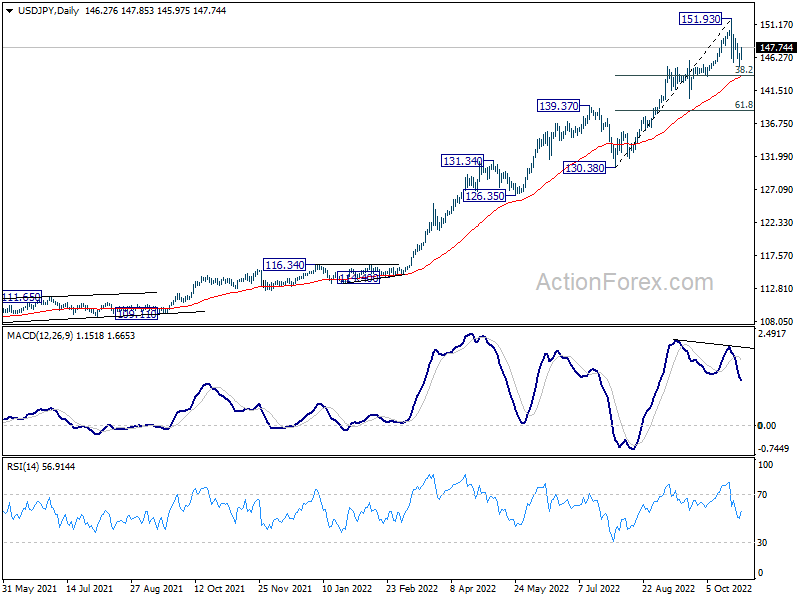

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is no clearly sign of topping yet. In any case, break of 140.33 support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 3.40% | 3.20% | 2.80% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.60% | 2.50% | 2.50% | |

| 00:30 | AUD | PPI Q/Q Q3 | 1.90% | 1.50% | 1.40% | |

| 00:30 | AUD | PPI Y/Y Q3 | 6.40% | 6.40% | 5.60% | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:30 | EUR | France Consumer Spending M/M Sep | 1.20% | 1.20% | 0.00% | 0.10% |

| 05:30 | EUR | France GDP Q/Q Q3 P | 0.20% | 0.20% | 0.50% | |

| 07:00 | CHF | KOF Leading Indicator Oct | 90.9 | 93 | 93.8 | |

| 08:00 | EUR | Germany GDP Q/Q Q3 P | 0.30% | -0.20% | 0.10% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 92.5 | 92.5 | 93.7 | 93.6 |

| 09:00 | EUR | Eurozone Services Sentiment Oct | 1.8 | 3.3 | 4.9 | 4.4 |

| 09:00 | EUR | Eurozone Industrial Confidence Oct | -1.2 | -2 | -0.4 | -0.3 |

| 09:00 | EUR | Eurozone Consumer Confidence Oct F | -27.6 | -27.6 | -27.6 | -28.8 |

| 12:00 | EUR | Germany CPI M/M Oct P | 0.90% | 0.60% | 1.90% | |

| 12:00 | EUR | Germany CPI Y/Y Oct P | 10.40% | 10.10% | 10.00% | |

| 12:30 | CAD | GDP M/M Aug | 0.10% | 0.00% | 0.10% | |

| 12:30 | USD | Personal Income M/M Sep | 0.40% | 0.30% | 0.30% | 0.40% |

| 12:30 | USD | Personal Spending Sep | 0.60% | 0.40% | 0.40% | 0.60% |

| 12:30 | USD | PCE Price Index M/M Sep | 0.30% | 0.50% | 0.30% | |

| 12:30 | USD | PCE Price Index Y/Y Sep | 6.20% | 5.80% | 6.20% | |

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.50% | 0.50% | 0.60% | |

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 5.10% | 5.20% | 4.90% | |

| 12:30 | USD | Employment Cost Index Q3 | 1.20% | 1.30% | 1.30% | |

| 14:00 | USD | Pending Home Sales M/M Sep | -5.30% | -2.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 59.8 | 59.8 |

{kind=link}