Dollar rises mildly in Asian session as investors turned cautious. Euro is also firmer but Sterling is on the softer side together with Aussie and Kiwi. Market focus are on the four central bank meetings this week, and lots of important indicators. Among them, Fed’s new economic projections and dot plot would likely be most market moving.

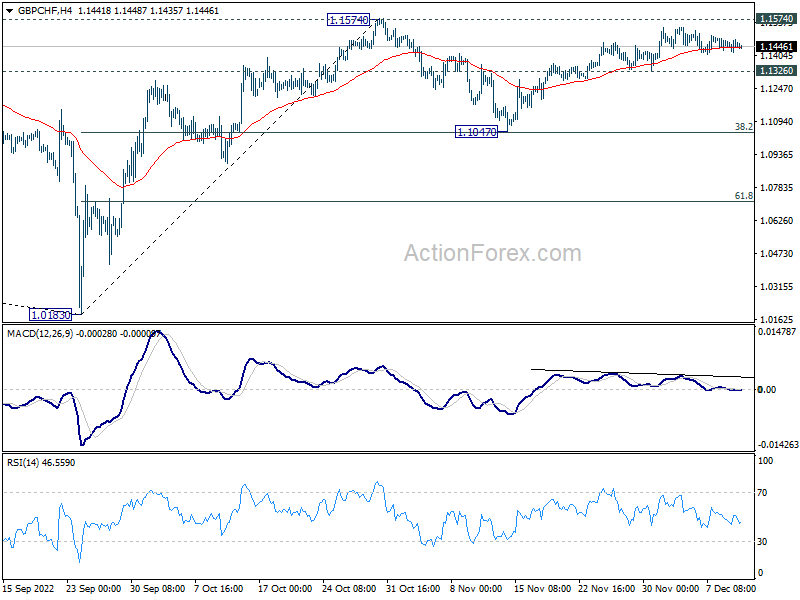

GBP/CHF could be a mover this week with BoE and SNB featured. Technically, rebound from 1.1047 is seen as the second leg of the consolidation pattern from 1.1574. Upside momentum has been diminishing just ahead of this resistance, as seen in 4 hour MACD. For now, break of 1.1574 is not anticipated in case of another rise. Instead, break of 1.1326 support should indicate the start of the third leg, and target 1.1047 again. But downside should be contained there to complete the pattern.

In Asia, at the time of writing, Nikkei is down -0.27%. Hong Kong HSI is down -1.88%. China Shanghai SSE is down -0.63%. Singapore Strait Times is up 0.04%. Japan 10-year JGB yield is up 0.0022 at 0.258.

Japan PPI slowed to 9.3% yoy in Nov, global commodity prices easing

Japan corporate goods price index slowed from 9.4% yoy to 9.3% yoy in November, above expectation of 8.9% yoy. The index, at 118.5, was a record high. Yen-based import price index slowed notably from 42.3% yoy to 28.2% yoy.

“Companies were passing on rising raw material costs for a broad range of goods. But some goods saw the impact of recent easing of global commodity prices,” a BOJ official told a briefing.

Also from Japan, MoF’s Business Survey Index for all large industries rose from 0.4 to 0.7 in Q4. BSI large manufacturing, however, dropped from 1.7 to -3.6. BSI large non-manufacturing improved form -0.2 to 2.7. BSI medium all industries rose from -2.2 to 4.7. BSI small all industries rose from -15.9 to -6.0.

Fed, ECB, BoE and SNB to hike 50bps

Four central banks are expected to raise interest rate this week. Fed is widely expected to slow down the pace of tightening, and hike interest rate by 50bps to 4.25-4.50%. Tightening is certainly not finished and the FOMC statement will make it clear. The main focus is on the new economic projections where three questions would be answered: The terminal rate, the time to get there, and the time to stay there. Currently, markets are expecting the federal funds are to peak at 5.00-5.52% in Q2 next year.

ECB is also expected to slow down and deliver a 50bps rate hike to 2.50%. There are expectations that ECB’s main refinancing rate will peak at 3.00% in Q1. But the central bank reiterate its meeting-by-meeting approach, and reveal little about the path forward, except the direction. Another focus is any announcement regarding quantitative tightening.

BoE is also expected to slow the pace of tightening and hike by 50bps to 3.50%. Opinions on the terminal rate for BoE vary, and it could very much depend on the depth of the recession. Meanwhile, some attention will be on the voting. Last month, only seven MPC members voted for the 75bps hike. Swati Dhingra voted for 50bps, while Silvana Tenreyro voted for 25bps.

SNB is also expected to raise the policy rate by 50bps to 1.00%. With inflation much tamer than other major regions, SNB’s terminal rate will certainly be much lower. A focus in on whether the central bank would indicate how close it is to the end of the cycle. Also, some attention would be on its rhetorics on exchange rates.

The week will also feature a large number of important economic data, before people head off to holidays. Here are some highlights for the week:

- Monday: Japan BSI manufacturing index, PPI, machine tools orders; UK GDP, production, trade balance, NIESR GDP estimate.

- Tuesday: Australia Westpac consumer sentiment, NAB business confidence; UK employment; Swiss SECO economic forecasts; Germany CPI final, ZEW economic sentiment; US NFIB small business index, CPI.

- Wednesday: New Zealand current account; Japan machine orders, Tankan survey; UK CPI, RPI; Swiss PPI; Eurozone industrial production; Canada manufacturing sales; US FOMC rate decision, import prices.

- Thursday: New Zealand GDP; Japan trade balance, tertiary industry index; Australia employment; China industrial production, retail sales, fixed asset investment; SNB rate decision; BoE rate decision; ECB rate decision; Canada housing starts; US retail sales, Philly Fed survey, jobless claims, industrial production, business inventories.

- Friday: New Zealand BusinessNZ manufacturing index; Australia PMIs; Japan PMI manufacturing; UK retail sales, PMIs; Eurozone PMIs, CPI final, trade balance; Canada wholesale sales; US PMIs.

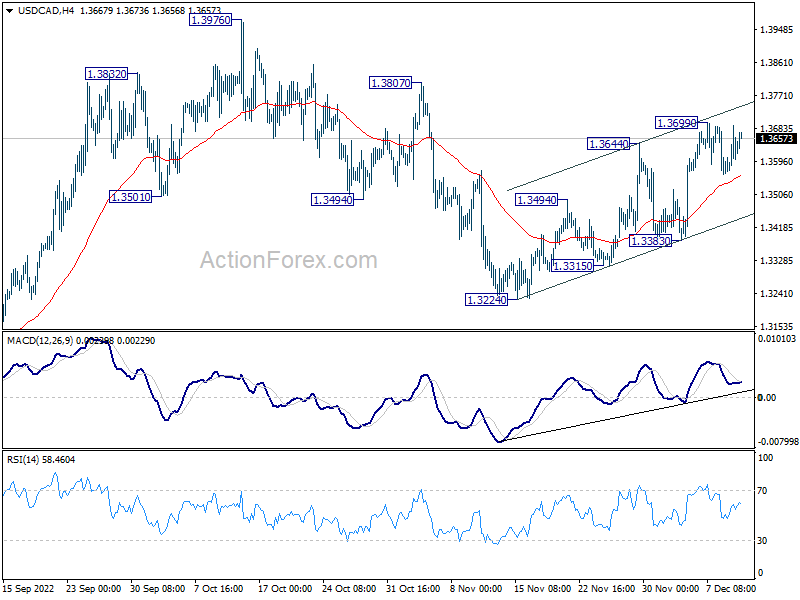

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3579; (P) 1.3635; (R1) 1.3701; More….

Intraday bias in USD/CAD remains neutral as consolidation from 1.3699 is still in progress. The favored case is still that correction from 1.3976 has completed at 1.3224. Above 1.3699 will resume the rebound from there to 1.3807 resistance, and then retesting 1.3976 high. However, break of 1.3383 support will dampen this case and bring retest of 1.3224 low instead.

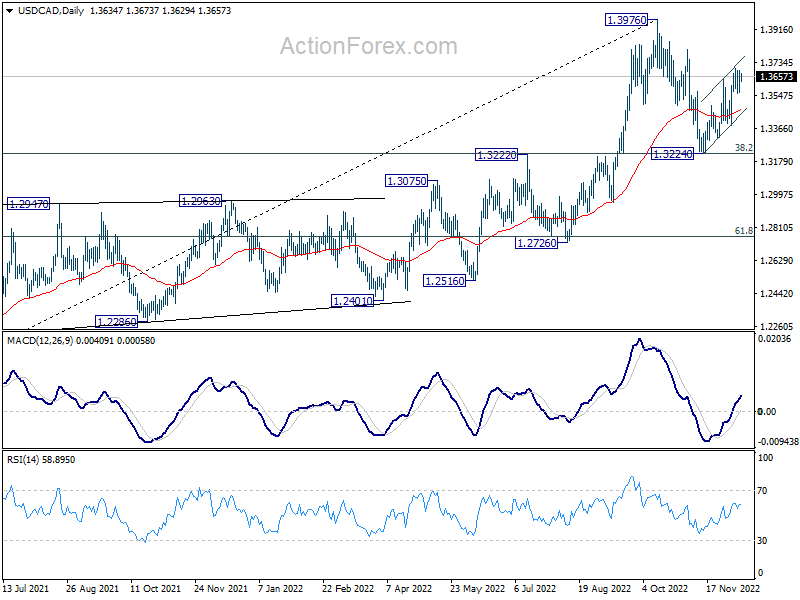

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Nov | 9.30% | 8.90% | 9.10% | 9.40% |

| 23:50 | JPY | BSI Manufacturing Index Q4 | -3.6 | 2.3 | 1.7 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | -5.40% | |||

| 07:00 | GBP | GDP M/M Oct | 0.40% | -0.60% | ||

| 07:00 | GBP | Index of Services 3M/3M Oct | -0.10% | 0.00% | ||

| 07:00 | GBP | Industrial Production M/M Oct | -0.30% | 0.20% | ||

| 07:00 | GBP | Industrial Production Y/Y Oct | -4.20% | -3.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Oct | -0.10% | 0.00% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Oct | -6.30% | -5.80% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | -15.0B | -15.7B | ||

| 13:00 | GBP | NIESR GDP Estimate (3M) Nov | -0.30% |

{kind=link}