Yen is stealing the show in the week of heavy weight events, powering up broadly with help of broad based decline in US and European treasury yields. Swiss Franc is following together with Euro while Dollar is just mixed. On the other hand, Sterling is the worst perform despite BoE rate hike, followed by Aussie and Kiwi. It might look like a risk-off setting, but no, it’s not, considering the strong rally in NASDAQ. Focuses will now turn to US non-farm payroll employment report and more wild rides could lie ahead.

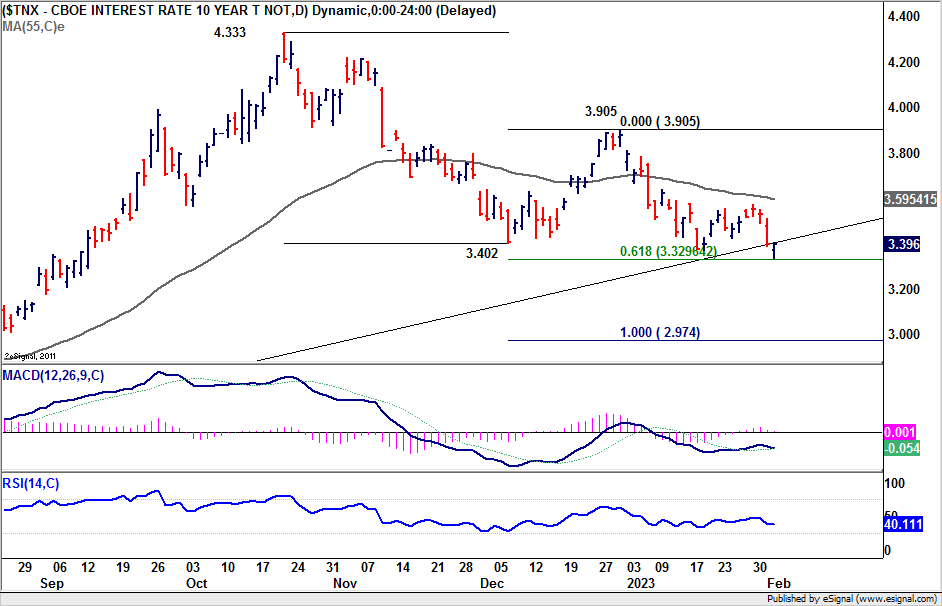

Technically, 10-year yield staged an impressive rebound overnight, closing nearly flat at 3.396 after diving to 3.334. 61.8% projection of 4.333 to 3.402 from 3.905 at 3.329 was nearly met already, and there is prospect of a turn around. Extended rebound from current level, followed by break of 55 day EMA (now at 3.595) later in the month, would confirm completion of the correction from 4.333. However, another dive through 3.329 could prompt downside acceleration to 100% projection at 2.974, which is slightly below 3% handle. We’d probably know which way it takes today, and that would also guide the direction of USD/JPY.

In Asia, Nikkei closed up 0.39%. Hong Kong HSI is down -1.40%. China Shanghai SSE is down -0.67%. Singapore Strait Times is up 0.52%. Japan 10-year JGB yield is down -0.0141 at 0.486. Overnight, DOW dropped -0.11%. S&P 500 rose 1.47%. NASDAQ rose 3.25%. 10-year yield dropped -0.001 to 3.396, after dipping to 3.334.

BoJ Kuroda expects wages to rise quite significantly

BoJ Governor Haruhiko Kuroda told the parliament he expected wages to rise “quite significantly”, thanks to improvement in the economy and a tightening job market.

Nevertheless, he reiterated that “BoJ must maintain the ultra-easy policy to support the economy and create an environment for firms to hike wages.”

China PMI composite rose to 51.1, services a boom and manufacturing a drag

China Caixin PMI Services rose from 48.0 to 52.9 in January, first expansionary reading in five months. PMI Composite rose from 48.3 to 51.1, the first upturn in total business activity since August 2022.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Services activity experienced a boom, as both supply and demand expanded, whereas the manufacturing sector became a drag. Employment remained relatively sluggish, with the manufacturing sector logging a larger contraction. Prices stayed stable. Optimism among businesses improved significantly.”

NASDAQ enjoying best year start in decades as focus turns to NFP

Overall risk sentiment is on the positive side as market focus turn to non-farm payroll report today. The messages from Fed and BoE this week were clear that the tightening cycle is close to a peak. It’s just a matter of 4.75-5.00% or 5.00-5.25% for Fed, and 4.25% or 4.50% for BoE. While ECB is still staying the course and at least two more hikes are on the card according to unnamed source, rate will peak below 4% handle.

Markets are expecting 193k NFP job growth in January, with unemployment rate ticked up from 3.5% to 3.6%. Average hourly earnings are expected to grow 0.3% mom. For investors, the ideal scenario is solid job growth, with gradual uptick in unemployment rate and modest wages growth. That scenario would keep Fed on track to pause in Q2.

NASDAQ rally has been rather impressive, up 16% year-to-day, logging the best performance since 1975. Based on current momentum, 38.2% retracement of 16212.22 to 10088.82 at 12427.95 should be taken out with ease for the near term. The real test is on 13181.05 cluster resistance (50% retracement at 13150.52). Sustained break there will build up the case of bullish trend reversal. But in any case, further rally will be expected as long as 11388.54 support holds. Meanwhile, solid risk-on sentiment could continue to limit Dollar’s rebound.

Elsewhere

China France industrial production, Eurozone PPI and PMI services, as well as UK PMI services will be released in European session. From the US, IFM services will also be featured next to NFP.

USD/JPY Daily Outlook

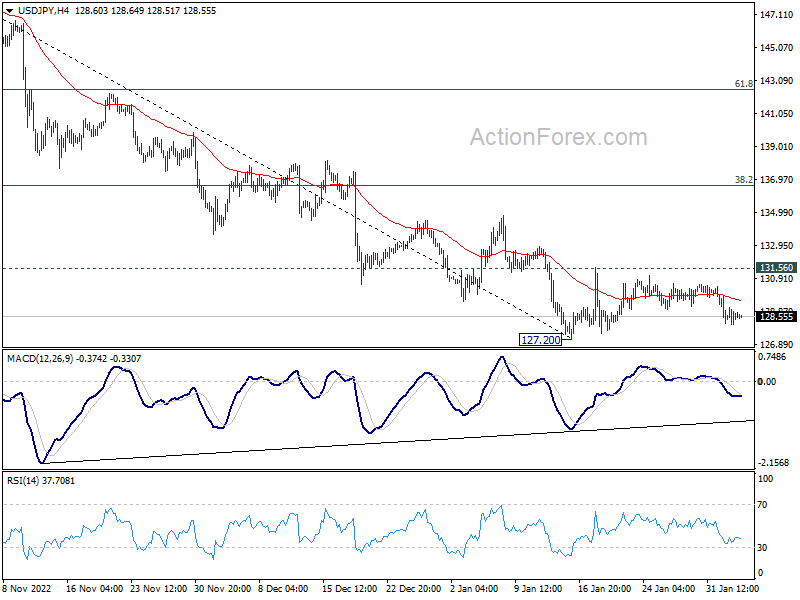

Daily Pivots: (S1) 128.14; (P) 128.64; (R1) 129.18; More…

While USD/JPY weakens this week, downside is still contained above 127.20 support. Intraday bias remains neutral first. On the downside, break of 127.20 will resume the whole decline from 151.93 and target 121.43 fibonacci level. Nevertheless, on the upside, break of 131.56 resistance should confirm short term bottoming, and turn bias back to the upside for stronger rebound to 55 day EMA (now at 133.23) and possibly above.

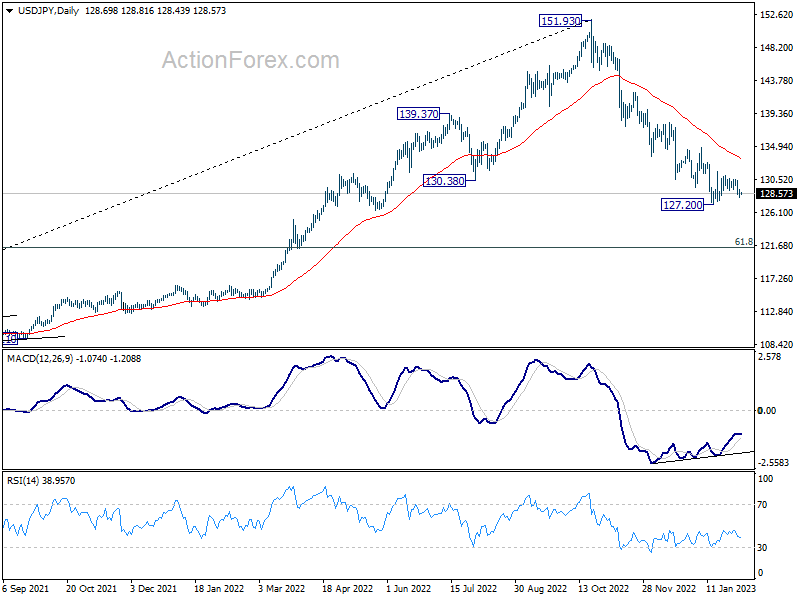

In the bigger picture, the break of 55 week EMA (now at 131.39) raises the chance of medium term bearish reversal, but that’s not confirmed yet. Strong support could be seen around 61.8% retracement of 102.58 to 151.93 at 121.43 and 38.2% retracement of 75.56 to 151.93 at 122.75 to bring rebound. But break of 131.56 resistance is needed to indicate bottoming first. Otherwise further fall will remain in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Jan | 52.9 | 51.6 | 48 | |

| 07:45 | EUR | France Industrial Output M/M Dec | 0.20% | 2.00% | ||

| 08:45 | EUR | Italy Services PMI Jan | 50.9 | 49.9 | ||

| 08:50 | EUR | France Services PMI Jan F | 49.2 | 49.2 | ||

| 08:55 | EUR | Germany Services PMI Jan F | 50.4 | 50.4 | ||

| 09:00 | EUR | Eurozone Services PMI Jan F | 50.7 | 50.7 | ||

| 09:30 | GBP | Services PMI Jan F | 48 | 48 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | -1.70% | -0.90% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 30.20% | 27.10% | ||

| 13:30 | USD | Nonfarm Payrolls Jan | 193K | 223K | ||

| 13:30 | USD | Unemployment Rate Jan | 3.60% | 3.50% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.30% | ||

| 14:45 | USD | Services PMI Jan F | 46.6 | 46.6 | ||

| 15:00 | USD | ISM Services PMI Jan | 50.4 | 49.6 |

{kind=link}