Dollar experienced a significant fall during early US trading hours following a mixed non-farm payroll report. Although the headline job growth was strong, the increase in the unemployment rate and the slowdown in wage growth could give the Federal Reserve something to think about beyond March. Meanwhile, Canadian dollar did not receive much support from better-than-expected job data.

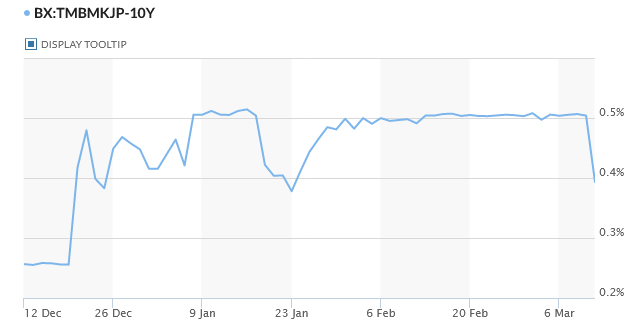

On the other hand, Swiss Franc was the star of the day, buoyed by risk aversion and falling US and European benchmark yields. In contrast, Yen was the second-worst performer of the day after the BoJ left its ultra-loose monetary policy unchanged. 10-year JGB yield also tumbled sharply away from the 0.5% cap.

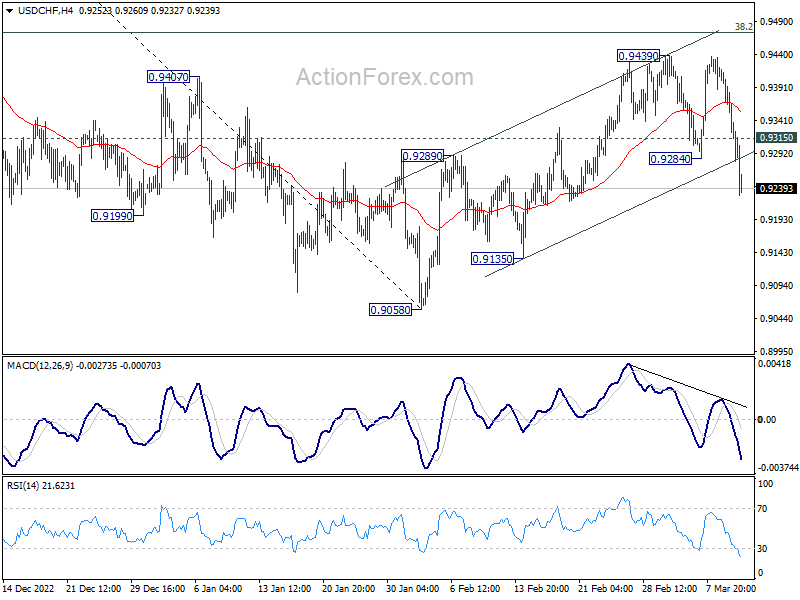

From a technical perspective, the break of 0.9284 support in USD/CHF is a signal of a deeper selloff in Dollar, but other currencies need to follow suit. Key levels to watch include 1.0693 resistance in EUR/USD, 0.6694 resistance in AUD/USD, 135.35 support in USD/JPY, and 1.3751 support in USD/CAD. As long as these levels hold, the selloff in the greenback may only be temporary.

In Europe, at the time of writing, FTSE is down -1.42%. DAX is down -0.99%. CAC is down -0.88%. Germany 10-year yield is down -0.1283 at 2.517. Earlier in Asia, Nikkei dropped -1.67%. Hong Kong HSI dropped -3.04%. China Shanghai SSE dropped -1.40%. Singapore Strait Times dropped -1.15%. Japan 10-year JGB yield dropped -0.1107 to 0.393.

US NFP rose 311k, unemployment rate rose to 3.6%

US non-farm payroll employment rose 311k in February, well above expectation of 200k. January’s figure was revised just slightly down from 517k to 504k. That compared with average monthly gain of 343k over the prior 6 months.

Unemployment rate rose from 3.4% to 3.6%, above expectation of 3.4%. Participation rate rose from 62.4% to 62.5%.

Average hourly earnings rose 0.2% mom, below expectation of 0.3% mom. Average workweek edged down by -0.1 hour to 34.5 hour.

Canada employment rose 21.8k, unemployment rate unchanged at 5.0%

Canada employment rose 21.8k in February, well above expectation of 2.5k. Unemployment rate was unchanged at 5.0%, versus expectation of 5.1%. But that’s just shy of record-low 4.9% in June and July 2022. Labor force participation rate held steady at 65.7%. Total hours worked rose 0.6% mom. Average hourly waves rose 5.4% yoy

UK GDP grew 0.3% mom in Jan as services rose 0.5%

UK GDP grew 0.3% mom in January, better than expectation of 0.1% mom. Services rose 0.5% mom. Production declined -0.3% mom. Construction fell by -1.7% mom.

For the three months to January, however, GDP was flat. Services was flat. Production grew by 0.3% while construction contracted -0.7%.

Also published, manufacturing production came in at -0.4% mom, -5.2% yoy in January, versus expectation of -0.1% mom, -5.0% yoy. Industrial production was at -0.3% mom, -4.3% yoy, versus expectation of -0.1% mom, -4.0% yoy. Goods trade deficit narrowed from GBP -19.3B to GBP -17.9B, versus expectation of GBP -17.5B.

NIESR forecasts UK GDP to contract -0.1% in Q1, outlook continues to improve

NIESR forecasts UK GDP to contract -0.1% in Q1, a shallower contraction of -0.2% in prior forecast.

Paula Bejarano Carbo, Associate Economist, NIESR, said “The outlook for the first quarter of 2023 continues to improve as higher-frequency data, including the services and construction February PMIs, indicate that activity will continue to pick-up in February, suggesting that any contraction we might see over Q1 is likely to be shallow.”

BoJ stands pat and maintains easing bias

As anticipated, BoJ left its monetary policy unchanged today, maintaining its easing bias. Despite a rise in inflation expectations, CPI is projected to slow down during the current fiscal year before experiencing a moderate increase once again.

Under yield curve control, short-term policy rate was held at -0.10%. Long-term interest rate will remain at around 0% with necessary purchase of JGBs without an upper limit. The band for 10-year JGB yield to fluctuate stayed at plus and minus 0.5%.

BoJ maintained the pledge to continue with QQE with YCC for “as long as it is necessary”. It “will not hesitate to take additional easing measures if necessary”. It also expects “short- and long-term policy interest rates to remain at their present or lower levels”.

BoJ said the economy “has picked up” with exports and industrial production “more or less flat”. The economy is projected to “continue growing at a pace above its potential growth rate” as a virtuous cycle form income to spending intensifies gradually.

Inflation expectations “have risen”. But, CPI is “likely to decelerate toward the middle of fiscal 2023”, then “accelerate moderately” on the back of improvement in output gap, rises in medium- to long-term inflation expectations in wage growth, and waning down of energy prices measures.”

The meeting was the last one to be chaired by Governor Haruhiko Kuroda. Kazuo Ueda was approved by both houses of the parliament this week as the next BoJ Governor.

New Zealand BNZ manufacturing rose to 52, gearshift but not strong

New Zealand BusinessNZ Performance of Manufacturing Index rose from 51.2 to 52.0 in February, signalling further increase in expansion. But the reading was still below its long-term average of 53.0.

Looking at some details, production dropped from 52.0 to 49.4. Employment rose from 51.6 to 54.0. New orders rose from 49.2 to 52.0. Finished stocks rose from 52.7 to 55.8. Deliveries was unchanged at 51.8.

BNZ Senior Economist, Craig Ebert stated that “it’s been a New Year gearshift, out of reverse. However, these are not what you’d call strong results – in total, and especially when delving into the details. That said, February’s PMI, like January’s, did denote expansion, overall, and is not all that far shy of its long-term average of 53.0”.=

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9291; (P) 0.9359; (R1) 0.9395; More…

USD/CHF’s strong break of 0.9284 support should now confirm that corrective rebound from 0.9058 has completed at 0.9439. That came ahead of 38.2% retracement of 1.0146 to 0.9058 at 0.9474. Intraday bias is back on the downside for retesting 0.9058 low. Firm break there will resume larger down trend from 1.0146. On the upside, however, break of 0.9315 minor resistance will mix up the outlook and turn bias neutral again.

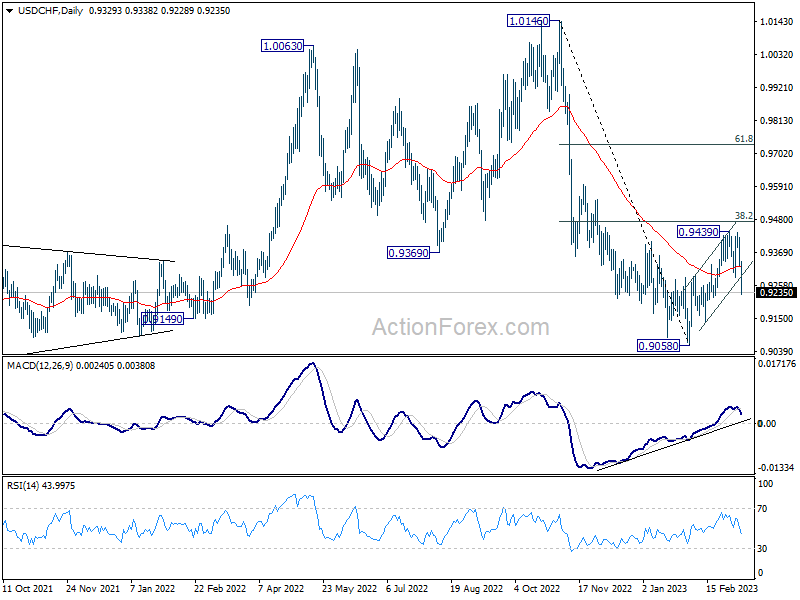

In the bigger picture, decline from 1.0146 is seen as part of a long term sideway pattern. As long as 38.2% retracement of 1.0146 to 0.9058 at 0.9474 holds, another fall is in favor through 0.9058. However, sustained trading above 0.9474 will indicate that the medium term trend has reversed, and open up further rally to 61.8% retracement at 0.9730 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 52 | 50.8 | 51.2 | |

| 21:45 | NZD | Manufacturing Sales Q4 | -0.40% | 5.10% | ||

| 23:30 | JPY | Household Spending Y/Y Jan | -0.30% | -0.20% | -1.30% | |

| 23:50 | JPY | PPI Y/Y Feb | 8.20% | 8.60% | 9.50% | |

| 02:31 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | EUR | Germany CPI M/M Feb F | 0.80% | 0.80% | 0.80% | |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 8.70% | 8.70% | 8.70% | |

| 07:00 | GBP | GDP M/M Jan | 0.30% | 0.10% | -0.50% | |

| 07:00 | GBP | Manufacturing Production M/M Jan | -0.40% | -0.10% | 0.00% | |

| 07:00 | GBP | Manufacturing Production Y/Y Jan | -5.20% | -5.00% | -5.70% | |

| 07:00 | GBP | Industrial Production M/M Jan | -0.30% | -0.10% | 0.30% | |

| 07:00 | GBP | Industrial Production Y/Y Jan | -4.30% | -4.00% | -4.00% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -17.9B | -17.5B | -19.3B | |

| 11:40 | GBP | NIESR GDP Estimate (3M) Feb | -0.10% | -0.10% | ||

| 13:30 | USD | Nonfarm Payrolls Feb | 311K | 200K | 517K | 504K |

| 13:30 | USD | Unemployment Rate Feb | 3.60% | 3.40% | 3.40% | |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.20% | 0.30% | 0.30% | |

| 13:30 | CAD | Net Change in Employment Feb | 21.8K | 2.5K | 150.0K | |

| 13:30 | CAD | Unemployment Rate Feb | 5.00% | 5.10% | 5.00% | |

| 13:30 | CAD | Capacity Utilization Q4 | 83.30% | 82.60% |

{kind=link}