Today’s trading remains relatively subdued, as many markets are still closed for holidays. Canadian and US Dollars are showing mild strength, while Yen struggles as the weakest currency, followed by New Zealand Dollar and Euro. Sterling, Australian Dollar, and Swiss Franc exhibit mixed performance. Most pairs and crosses stay within Friday’s range, except for Yen pairs, which have been influenced by new BoJ Governor Kazuo Ueda’s dovish comments.

The week ahead is packed with events, including the BoC’s rate decision, which may not prompt significant volatility. Meanwhile, Dollar anticipates key data releases such as CPI, PPI, retail sales, and the University of Michigan Consumer Sentiment, along with FOMC minutes. In other regions, UK GDP and Australian employment data releases are expected to carry more weight than others.

Dollar braces for CPI release, a look at EUR/USD and DXY

This week promises to be eventful for Dollar, with key data releases including CPI, PPI, retail sales, and University of Michigan Consumer Sentiment. Additionally, Fed will publish minutes from March FOMC meeting, and numerous policymakers are expected to share their views on the economy and interest rates.

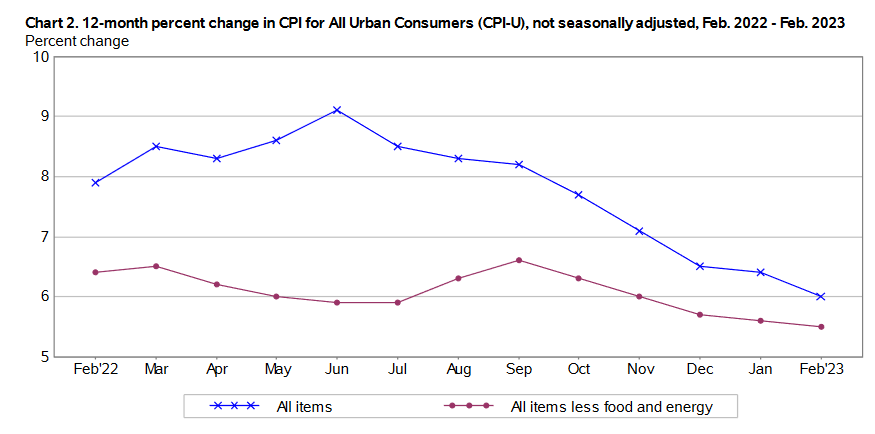

Specifically, headline CPI is forecasted to drop further from 6% to 5.2% in March. This marks a significant improvement from last year’s 9.1% peak in July and represents the ninth consecutive month of cooling consumer inflation. If realized, the headline CPI reading would be the lowest since June 2021’s 5.0%, nearly two years ago. Conversely, core CPI is projected to tick up from 5.5% to 5.6%, breaking the five-month downtrend since September last year.

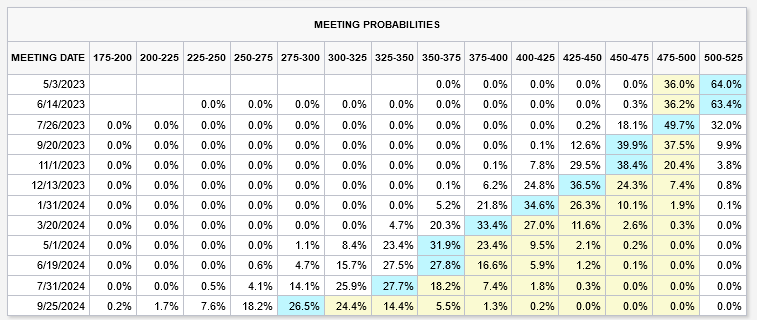

Following last week’s robust job data, traders have increased bets on a 25bps rate hike in May, with over a 60% chance. However, whether Fed opts for one, two, or no additional rate hikes may not make a significant difference. The primary focus is when Fed will start reversing course and cutting interest rates, which largely depends on how quickly core inflation falls back to a level consistent with price stability or remains stuck above the Fed’s target.

Presently, fed fund futures indicate a nearly 70% chance of a cut back to 4.50-4.75% in July, far from the Fed’s own projections. According to the March dot plot, only one policymaker envisions rates ending below 5% this year.

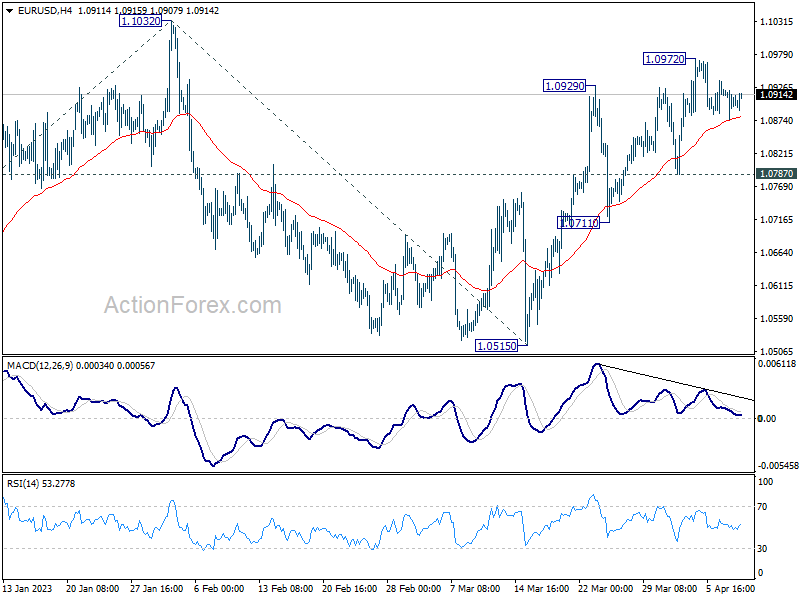

EUR/USD began losing upside momentum last week, stalling before 1.0320 resistance. It appears that a clear downside surprise in core CPI is needed to push EUR/USD past 1.0320 to resume the larger uptrend from the 2020 low at 0.9534. Conversely, breaking 1.0787 support will extend the consolidation pattern from 1.0320 with a third leg back towards 1.0515 support.

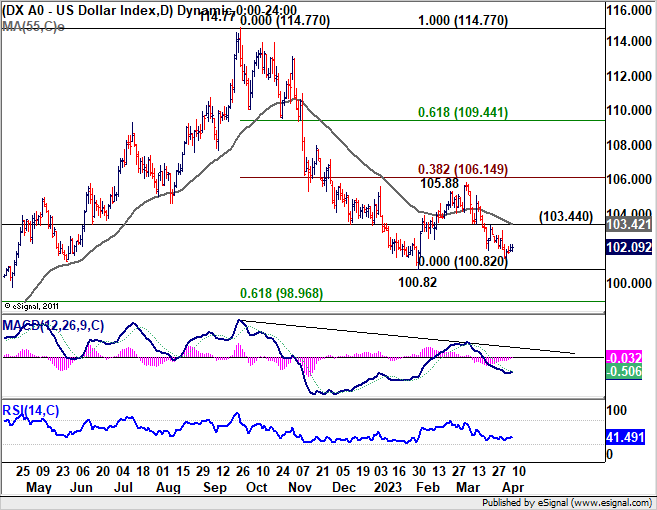

In parallel, for Dollar index, intense selling pressure is required to push DXY below 100.82 low to resume the downtrend from 114.77. Breaking above 103.44 resistance will extend the consolidation pattern from 100.82 with another upleg towards 105.88 resistance.

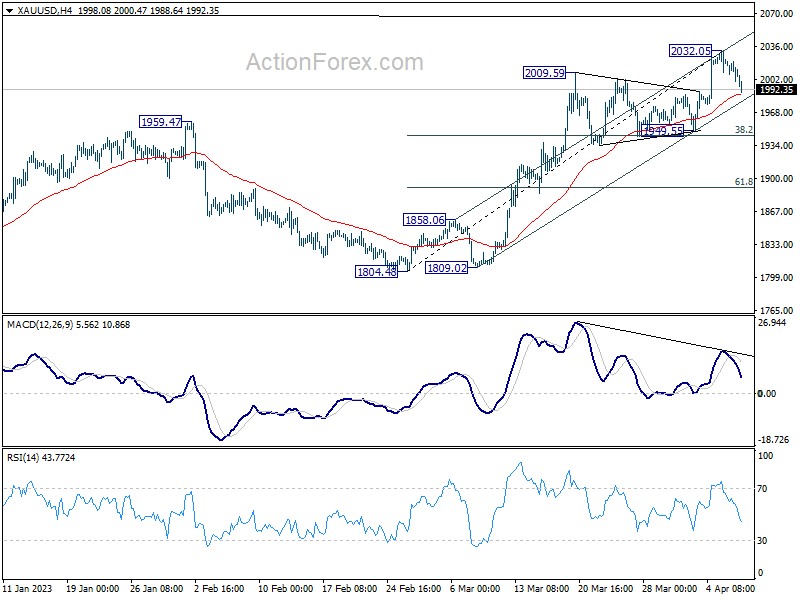

Gold falls below 2000 as expectations of anther Fed hike firm up

Gold dipped below 2000 as near-term pullback extended into Asian session, with many markets still on holiday. Shift appears to be driven by growing market conviction that Fed will implement another 25bps hike in May, as fed fund futures now indicate a 66% probability. This sentiment follows last week’s robust US non-farm payroll report. However, expectations could still change after release of March CPI data and FOMC minutes on Wednesday.

Technically, a short-term top for Gold may have formed at 2032.05, evidenced by a bearish divergence in 4-hour MACD. Rally from 1084.48 might have completed a five-wave sequence and stalled just ahead of key resistance zone between 2070.06 and 2074.84 record high.

Considering this, a deeper pullback is now anticipated. Crucial near-term support level can be found at 38.2% retracement of 1804.48 to 2032.05 at 1945.11 which is in proximity to 1949.55 support level. As long as this support zone holds, current price action from 2032.05 should be regarded as a brief corrective phase, and a rally to new record highs is expected sooner rather than later.

However, sustained break of 1945.11/1949.55 support zone could signal a deeper fall in underway, possibly extending the long-term consolidation pattern from 2074.84 with another downward leg. In this scenario, gold prices could decline to 61.8% retracement of 1804.48 to 2032.05 at 1894.41 or even further towards 1084.48.

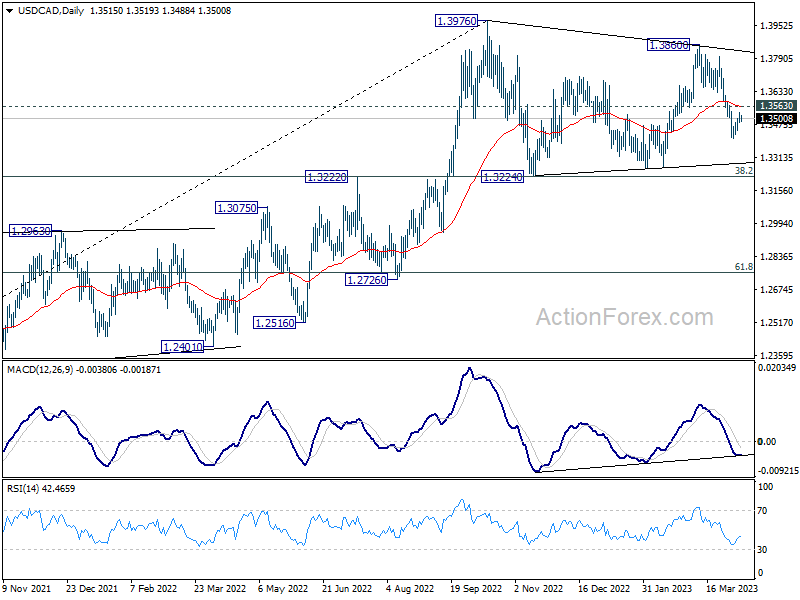

BoC expected to hold steady: Loonie’s fate lies in oil prices and US data

Bank of Canada (BoC) is widely anticipated to maintain its pause this week, leaving interest rates unchanged at a 15-year high of 4.50%. Governor Macklem has emphasized that there’s no need for additional rate hikes if the economy unfolds according to central bank’s projections, which forecast stalling growth for the rest of the year, subsequently cooling inflation. Macklem also stated that an “accumulation of evidence” would be required before considering resuming tightening.

Consequently, it’s unlikely that BoC’s announcement on Wednesday or Macklem’s speech on Thursday will trigger significant volatility in Canadian Dollar. Instead, Loonie is expected to be more reactive to developments in oil prices, as WTI crude remains stuck around 80 mark. Additionally, the currency could be influenced by US CPI data and the release of FOMC minutes when paired against the greenback.

From a technical perspective, USD/CAD appears to be in the third leg of the corrective pattern from 1.3967. Deeper decline is expected as long as 1.3563 minor resistance holds. However, robust support is anticipated around 1.3224, which should contain the downside and complete the pattern. On the other hand, a sustained break of 1.3563 and 55-day EMA (now at 1.3562) would likely result in a stronger rally back towards 1.3860 resistance level. Ultimately, the larger uptrend is envisaged to resume through 1.3976 at a later stage.

BoJ Ueda stands firm on monetary easing and negative rates

In his first press conference as new Bank of Japan Governor, Kazuo Ueda stated that the central bank will maintain its massive stimulus program, echoing the stance of the previous leadership. Ueda commented, “The BOJ’s current monetary easing is a very powerful one. We need to strive, as we have done so far, to appropriately grasp economic, price, and financial developments to see whether trend inflation will stably and sustainably achieve 2%.”

The governor acknowledged the side-effects of the BOJ’s negative rates, particularly on banks, but noted that banks seem to have sufficient buffers and financial intermediation is functioning. Ueda emphasized the necessity of maintaining negative rates, stating, “Given trend inflation has yet to hit 2%, it’s appropriate to maintain negative rates.”

Regarding Yield Curve Control (YCC), Ueda said, “When looking at current economic, price, and financial developments, it’s appropriate to maintain YCC for now.” He added that any major changes to YCC should be determined by evaluating the economic, price, and financial trends, while also weighing the benefits and costs of the policy.

Ueda noted some positive signs in inflation and wages, saying, “Trend inflation is rising somewhat. There’s also some positive signs in wages. There’s a good chance this will lead to stable, sustained achievement of higher, trend inflation.”

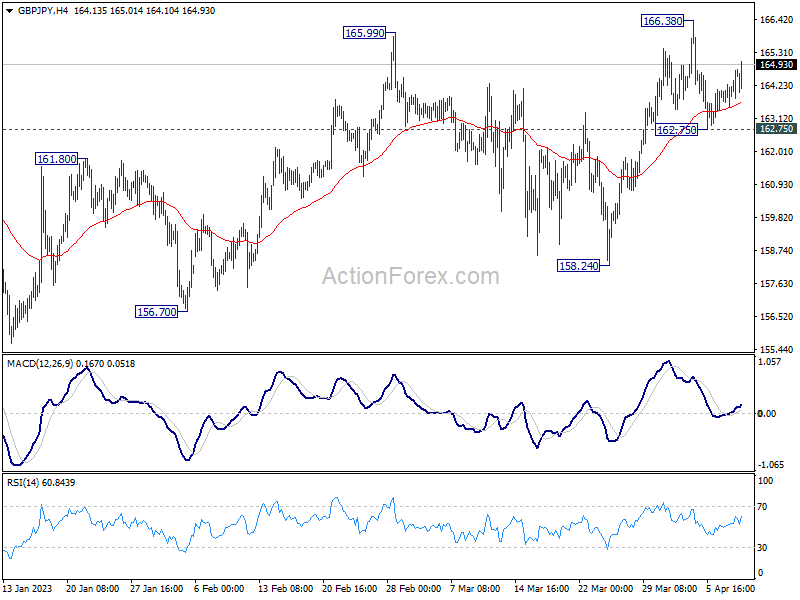

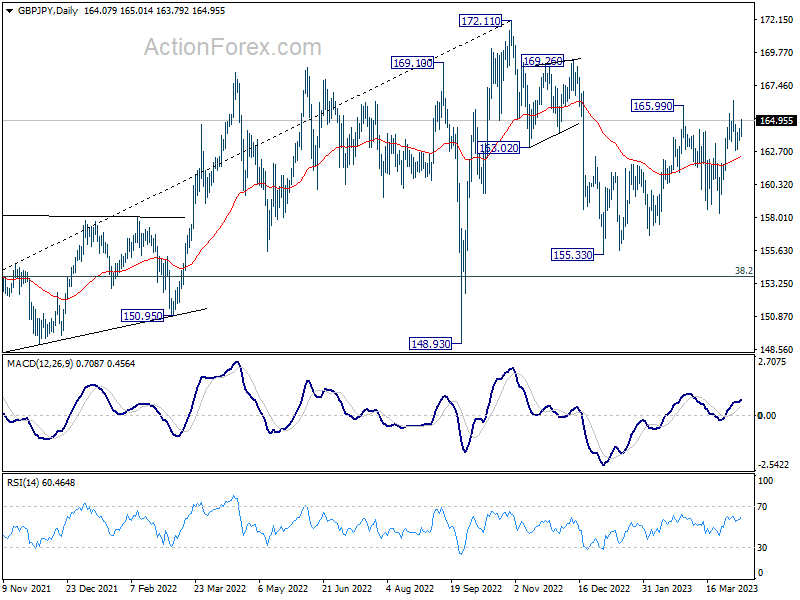

GBP/JPY Daily Outlook

Daily Pivots: (S1) 163.63; (P) 164.00; (R1) 164.43; More…

GBP/JPY recovers higher today but stays below 166.38 resistance. Intraday bias remains neutral at this point. On the upside, break of 166.38, and sustained trading above 165.99 resistance will resume the whole rebound from 155.33 to 169.26 resistance next. On the downside, however, break of 162.75 minor support will mix up the outlook and turn intraday bias to the downside for 158.24 support instead.

In the bigger picture, as long as 38.2% retracement of 123.94 (2020 low) to 172.11 (2022 high) at 153.70 holds, medium term bullishness is retained. That is, larger up trend from 123.94 (2020 low) is still in progress. Break of 172.11 high to resume such up trend is expected at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account (JPY) Feb | 1.09T | 1.42T | 0.22T | 0.20T |

| 05:00 | JPY | Consumer Confidence Index Mar | 33.9 | 31.6 | 31.1 | |

| 06:00 | JPY | Eco Watchers Survey: Current Mar | 53.3 | 50.4 | 52 | |

| 14:00 | USD | Wholesale Inventories Feb F | 0.20% | 0.20% |

{kind=link}