In the wake of BoJ’s decision to hold its monetary policy steady, we have seen an amplified sell-off in Yen, which is not surprising given the ongoing divergence in monetary policy with other major global central banks. The breaking of key levels in some crosses suggests that we might witness further declines in Yen, at least until Japanese authorities intervene once again.

Dollar, closely tailing Yen, is also displaying weakness and is ranked as the second poorest performer of the week. Nevertheless, it’s yet to be ascertained if the greenback’s trajectory is now inversely linked with risk sentiment, reverting to its norm.

On the other end of the spectrum, Australian Dollar is currently the week’s top performer, but Euro is also trying to close the gap. The common currency has been buoyed by yesterday’s rate hike by ECB and its hawkish economic projections. British Pound is holding up as the third strongest currency, as markets anticipate tightening by BoE next week. Meanwhile, Swiss Franc and New Zealand Dollar are showing a mixed performance, while Canadian Dollar is slightly on the softer side.

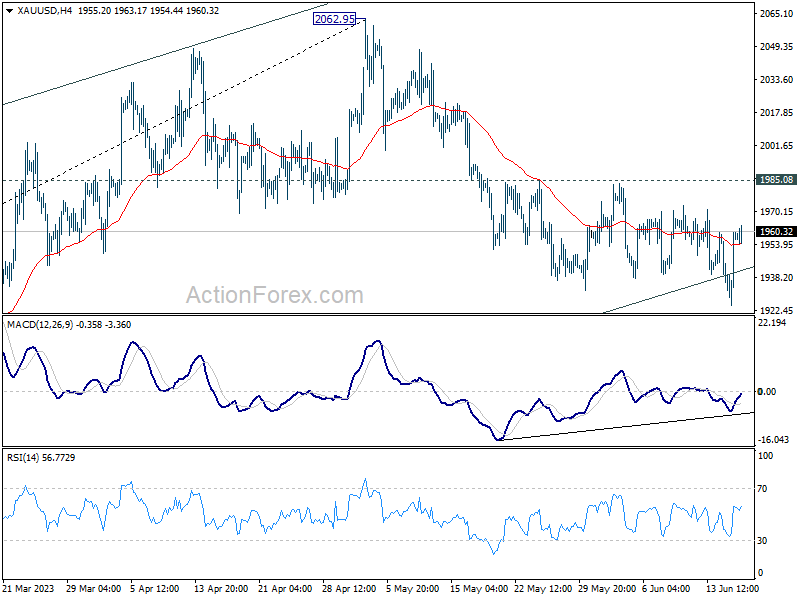

Technically, Gold recovered after just brief to 1924.61, back above medium term channel support. Bullish convergence is seen in 4H MACD. Break of 1985.08 resistance will argue that corrective fall from 2062.95 has completed. In this case, stronger rebound would be seen back to retest 2062.95 high. If realized, this could be a confirmation signal more deeper decline in Dollar elsewhere.

In Asia, Nikkei closed up 0.66%. Hong Kong HSI is up 1.00%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.57%. Japan 10-year JGB yield dropped -0.0187 to 0.413. Overnight, DOW rose 1.26%. S&P 500 rose 1.22%. NASDAQ rose 1.15%. 10-year yield dropped -0.068 to 3.728.

BoJ holds steady, core CPI to decelerate towards middle of fiscal 2023

In a widely expected move, BoJ today unanimously voted to maintain its existing ultra-loose monetary policy. The central bank kept short-term policy rate at -0.10% under its yield curve control. Yield target on 10-year JGB remains around 0%, with fluctuation band allowed also maintained at about plus and minus 0.50% from the target level. BoJ reiterated its commitment to carry on with its Quantitative and Qualitative Monetary Easing with Yield Curve Control “as long as it is necessary” and affirmed it “will not hesitate to take additional easing measures if necessary.”

In its accompanying statement, BoJ noted that it anticipates Japan’s economy to witness moderate recovery by around middle of the fiscal year 2023. “Thereafter, as a virtuous cycle from income to spending gradually intensifies, Japan’s economy is projected to continue growing at a pace about its potential growth rate,” the central bank said.

Discussing the inflation outlook, the bank stated: “The year-on-year rate of increase in the CPI (all items less fresh food) is likely to decelerate toward the middle of fiscal 2023, with a waning of the effects of the pass-through to consumer prices of cost increases led by the rise in import prices.

“Thereafter, the rate of increase is projected to accelerate again moderately, albeit with fluctuations, as the output gap improves and as medium- to long-term inflation expectations and wage growth rise, accompanied by changes in factors such as firms’ price- and wage-setting behavior.”

NZ BNZ PMI ticked up to 48.9, staying in relatively tight band of contraction

New Zealand BusinessNZ Performance of Manufacturing Index ticked up from 48.8 to 48.9 in May, staying well below long-term average activity rate of 53.0. Looking at some details, production dropped from 47.0 to 45.7. Employment rose from 47.7 to 49.5. New orders rose from 49.6 to 50.8. Finished stocks dropped from 52.5 to 51.5. Deliveries dropped from 50.7 to 46.0.

BusinessNZ’s Director, Advocacy Catherine Beard said: “New Zealand’s manufacturing sector has remained in a relatively tight band of contraction for the last three months. While the overall activity result has crept upwards over that time.”

BNZ Senior Economist, Craig Ebert stated that “the range of results in the sub-components is mirrored in the breadth of issues manufacturers are now highlighting in the survey. Gone is the dominance of supply-side laments, especially regarding staff. But new negatives have arisen, for all of them to (still be) outnumbering the positive issues referenced”.

Looking ahead

Eurozone CPI final and US U of Michigan consumer sentiment are the main features for the rest of the day.

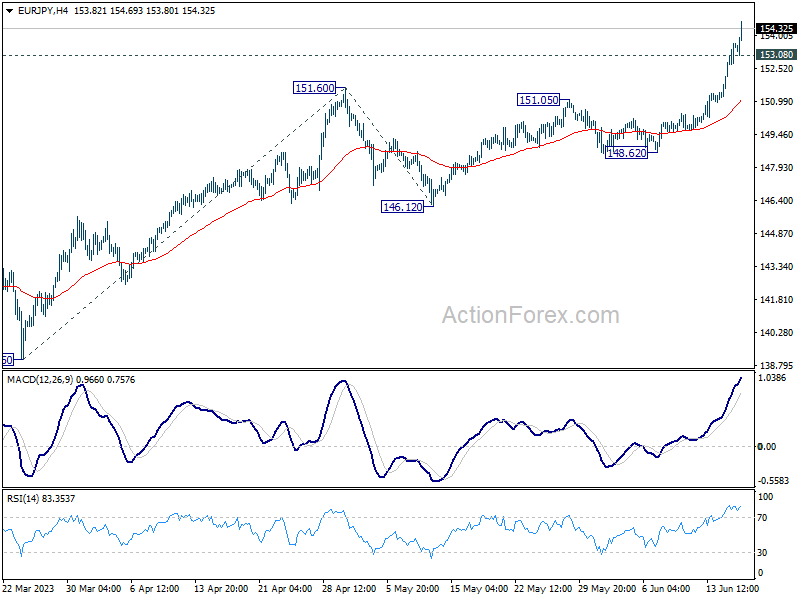

EUR/JPY Daily Outlook

Daily Pivots: (S1) 152.22; (P) 152.95; (R1) 154.29; More….

EUR/JPY accelerates to as high as 154.63 so far today. There is no sign of topping after breaking 153.63 medium term projection level. Intraday bias stays on the upside for 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, below 153.08 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64 is already met but there in no sign of topping. Further rally should be seen to 100% projection at 162.82 next. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 48.9 | 49.1 | ||

| 02:47 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 08:30 | GBP | Consumer Inflation Expectations | 3.90% | |||

| 09:00 | EUR | Eurozone CPI Y/Y May F | 6.10% | 6.10% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 5.30% | 5.30% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.00% | -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 60.2 | 59.2 |

{kind=link}