Euro turns weaker after ECB’s expected rate hike. Downside momentum is also picking up when ECB President Christine Lagarde indicated that even minor alterations in the statement’s phrasing were intentional. ECB has shifted its wording from interest rates “will be brought to” to will be “set” at a sufficiently restrictive level, providing a basis to that it’s now restrictive enough for a pause.

Meanwhile, Dollar is making a robust comeback, triggered by stronger than expected GDP data, among other positive economic indicators. Despite being the second weakest currency for the week so far, sharing the spot with Euro, the greenback now appears to have a chance to alter its positive given the current momentum. However, the eventual picture for the week remains uncertain given that Yen might have some moves, as BoJ gears up for its policy announcement tomorrow. Meanwhile, it’s starting to look hard for commodity currencies to maintain earlier gains.

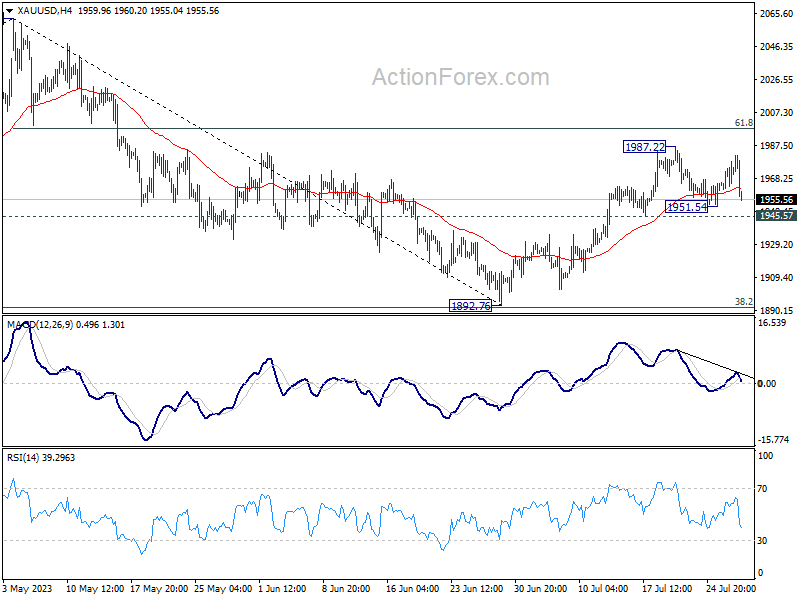

On the technical front, Gold experienced a downturn with the Dollar’s resurgence, having failed to surpass the 1987.22 resistance mark. The consolidation from 1987.22 is extending with another drop. However, prospects for a further rise are still viable as long as the 1945.57 support level holds. Nevertheless, a firm break below 1945.57 could indicate the completion of the overall rebound from 1892.76 and may serve as a confirmation signal for an extended rally in the greenback.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 1.36%. CAC is up 1.89%. Germany 10-year yield is down -0.047 at 2.439. Earlier in Asia, Nikkei rose 0.68%. Hong Kong HSI rose 1.41%. China Shanghai SSE dropped -0.20%. Singapore Strait Times rose 0.98%. Japan 10-year JGB yield dropped -0.0071 to 0.441.

US GDP grew 2.4% in Q2, faster than Q1 and above expectations

US GDP grew 2.4% annualized in Q2, according to the “advance” estimate, well above expectation of 1.6%. That’s also a faster growth than Q1’s 2.0% annualized. PCE price index slowed from 4.1% to 2.6% while PCE core price index also fell form 4.9% to 3.8%.

BEA said: “Compared to the first quarter, the acceleration in GDP in the second quarter primarily reflected an upturn in private inventory investment and an acceleration in nonresidential fixed investment. These movements were partly offset by a downturn in exports, and decelerations in consumer spending, federal government spending, and state and local government spending. Imports turned down.”

Also released, in June, durable goods orders rose 4.7% versus expectation of 1.0%. Ex-transport orders rose 0.6%, versus expectation of 0.1%. Goods trade deficit narrowed to USD -87.8B, versus expectation of USD -91.8B.

Initial jobless claims dropped slightly to 221k in the week ending July 21, below expectation of 233k.

ECB hikes 25 bps, maintains data-dependent approach

ECB sticks to the script and delivers another 25bps hike on its three key interest rates today, meeting market expectations. The main refinancing, marginal lending, and deposit rates now stand at 4.25%, 4.50%, and 3.75% respectively, effective August 2.

In its statement, the ECB highlighted the ongoing concerns around inflation, indicating it was poised to remain “above the target for an extended period”, despite expectations of a decrease over the remainder of the year. It also noted that while some measures showed signs of easing, “underlying inflation remains high overall.”

ECB reiterated that it is committed to setting interest rates at “sufficiently restrictive” levels “for as long as necessary”. Stressing the bank’s ongoing commitment to a data-dependent strategy, it added, “The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction.”

ECB President Christine Lagarde said in post meeting press conference:

ECB President Christine Lagarde, struck a somber tone during the post-meeting press conference. She acknowledged that the economic outlook for Eurozone has “deteriorated” in the near term, citing persistent high inflation and tighter financial conditions as key factors pressuring the manufacturing output.

Lagarde stated, “High inflation and tighter financing… is weighing especially on manufacturing output, which is also being held down by weak external demand.” Though she noted the resilience in the services sector, she cautioned that its “momentum is slowing”. The economy is expected to “remain weak in the short run.”

She then noted a shift in the drivers of inflation. External sources are easing, she noted, but domestic price pressures, including from rising wages and robust profit margins, are gaining prominence. “While some measures are moving lower, underlying inflation remains high overall,” Lagarde pointed out.

Germany Gfk consumer sentiment edged up to -24.4 on declining inflation

Germany Gfk Consumer Sentiment for August improved from -25.2 to -24.4, slightly above expectation of -24.7. In July, Economic Expectations was unchanged at 3.7. Income Expectations rose from -10.6 to -5.1. Propensity to buy ticked up from -14.6 to -14.3.

“Currently, only income expectations are contributing to the improvement in consumer sentiment. The main reason for the decrease in pessimism is the hope of declining inflation rates,” explains GfK consumer expert Rolf Bürkl.

“This has somewhat improved the chances of consumer sentiment resuming its recovery course. However, the level will still remain low in the coming months, and private consumption will therefore not be able to make a positive contribution to overall economic development.”

Australia export price down -8.5% qoq in Q2, largest fall since 2009

Australia’s Q2 Export Price Index registered -8.5% qoq drop, the most substantial quarterly decline since Q3 2009. Concurrently, the index declined -11.2% yoy compared to the same quarter last year. On the flip side, Import Price Index dipped slightly by -0.8% qoq, – 0.3% yoy.

Michelle Marquardt, Head of Price Statistics at Australian Bureau of Statistics (ABS), attributed this steep fall in the Export Price Index to a substantial contraction in global energy demand. “Global economic slowdown and eased supply pressures are contributing to a retreat in energy prices from their 2022 peak,” said Marquardt.

The dampening effect of weaker energy prices extended to the Import Price Index, which saw a decline of -0.8% in Q2 2023. More specifically, the prices of petroleum and petroleum products decreased by -7.0% in this quarter. Nevertheless, this decline in energy prices was somewhat counterbalanced by inflationary pressures on various imported consumption and capital goods.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1047; (P) 1.1077; (R1) 1.1115; More…

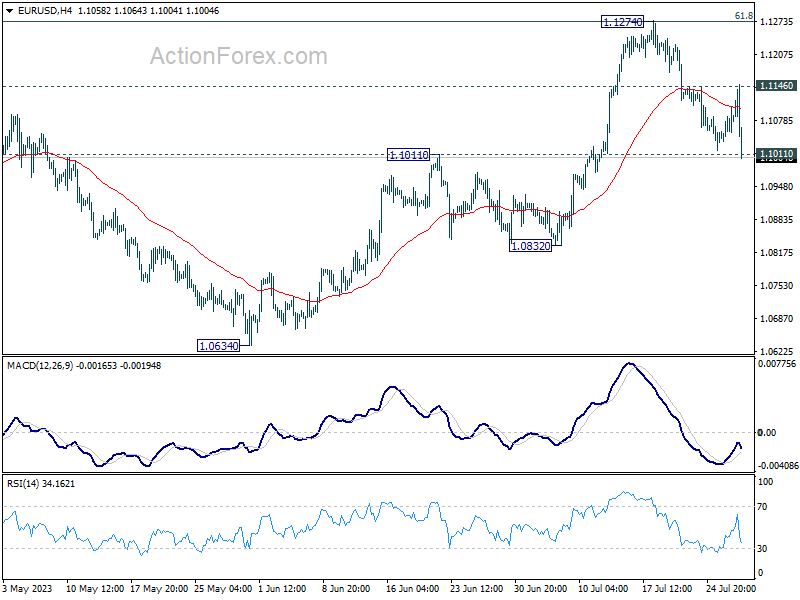

EUR/USD falls sharply after rejection by 1.1146 resistance and immediate focus is now on 1.1011 resistance turned support. Decisive break there will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support next. Nevertheless, rebound from current level, followed by firm break of 1.1146, will bring retest of 1.1274 high instead.

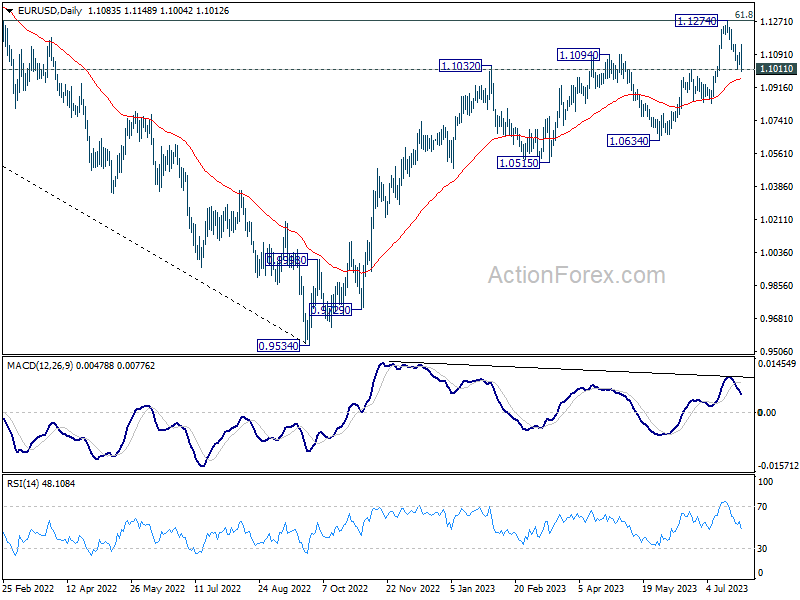

In the bigger picture, rise from 0.9534 is still expected to continue as long as 1.1011 resistance turned support holds. Decisive break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next. However, firm break of 1.1011 will indicate rejection by 1.1273 and raise the chance of reversal. Deeper fall would be seen back to 1.0634 support first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.80% | -0.80% | -4.20% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | -24.4 | -24.7 | -25.4 | -25.2 |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.25% | 4.00% | |

| 12:15 | EUR | ECB Rate On Deposit Facility | 3.75% | 3.75% | 3.50% | |

| 12:30 | USD | Initial Jobless Claims (Jul 21) | 221K | 233K | 228K | |

| 12:30 | USD | GDP Annualized Q2 P | 2.40% | 1.60% | 2.00% | |

| 12:30 | USD | GDP Price Index Q2 P | 2.60% | 3.10% | 4.10% | |

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -87.8B | -91.8B | -91.1B | -91.9B |

| 12:30 | USD | Wholesale Inventories Jun P | -0.30% | -0.10% | 0.00% | |

| 12:30 | USD | Durable Goods Orders Jun | 4.70% | 1.00% | 1.80% | |

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | 0.60% | 0.10% | 0.70% | |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:00 | USD | Pending Home Sales M/M Jun | -0.50% | -2.70% | ||

| 14:30 | USD | Natural Gas Storage | 12B | 41B |

{kind=link}