The beginning of the week is marked by heightened risk aversion and increasing geopolitical uncertainties, primarily stemming from escalating conflicts in the Middle East. The upswing in geopolitical tensions is casting a shadow, prompting a noticeable shift towards safe-haven assets like gold, oil, safe-haven currencies.

Japanese Yen emerges as the strongest contender in Asian session, exhibiting resilience even as Japan observes a bank holiday. Canadian Dollar, buoyed by a resurgence in oil prices, and Dollar and Swiss Franc, are also riding the wave of risk aversion. Conversely, Australian and New Zealand Dollars find themselves on shaky ground, echoing the vulnerability of Euro and Sterling amid the prevailing unrest.

However, the vibrancy typically associated with currency market movements seems subdued. This restraint could be attributed to holidays in both the US and Canada. There is a discernible hesitance among traders who are wary of making moves until the geopolitical panorama attains more clarity. While the world watches the Middle East with bated breath, crucial economic data sets, including US CPI and UK GDP, also loom on the horizon, ready to impact market sentiments.

Furthermore, the market’s attention remains divided as questions about the possible resumption of Yen’s selloff, in the aftermath of last week’s yet unconfirmed intervention by Japan. Reinforcing this sentiment, Naoyuki Shinohara, a former top currency diplomat, was quoted by Reuters. He emphasized that Japan is unlikely to counteract Yen’s downtrend, as changing the fundamental-driven market direction is not feasible. He advocates for the Bank of Japan’s shift towards normalizing its ultra-accommodative monetary policy as a viable response to the weakening Yen.

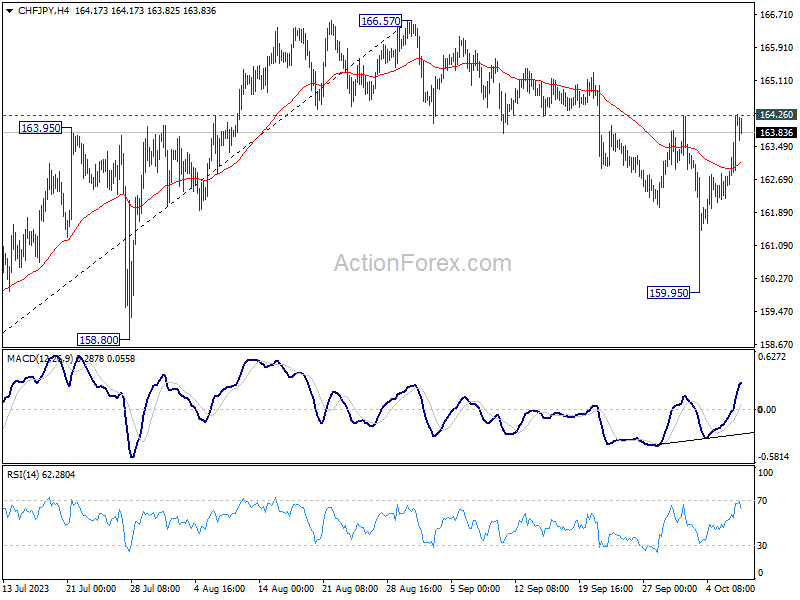

Technically, CHF/JPY is now pressing 164.26 resistance with the strong rebound from 159.95. Decisive break there will argue that the correction from 166.57, while deep, has completed. Stronger rally would be seen back to retest 166.57 high, and even above to resume the larger up trend. Such a development might be interpreted as an early indicator of a generalized Yen selloff.

In Asia, at the time of writing, China Shanghai SSE is down -0.39%. Singapore Strait Times is down -0.25%. Japan is on holiday while Hong Kong market is closed in the morning due to typhoon.

Gold, Oil, and Franc Surge: Safe-Haven Assets Respond to Israeli Crisis

As geopolitical tensions escalate, markets are swiftly reacting, with notable rises observed in Gold, Oil, and Swiss Franc at the beginning of the week. The eruption of hostilities between Israel and Hamas following a sweeping incursion by the Palestinian group into Israeli towns has sounded alarms worldwide, drawing unequivocal condemnation from Western nations, introducing a fresh element of uncertainty into the global financial markets.

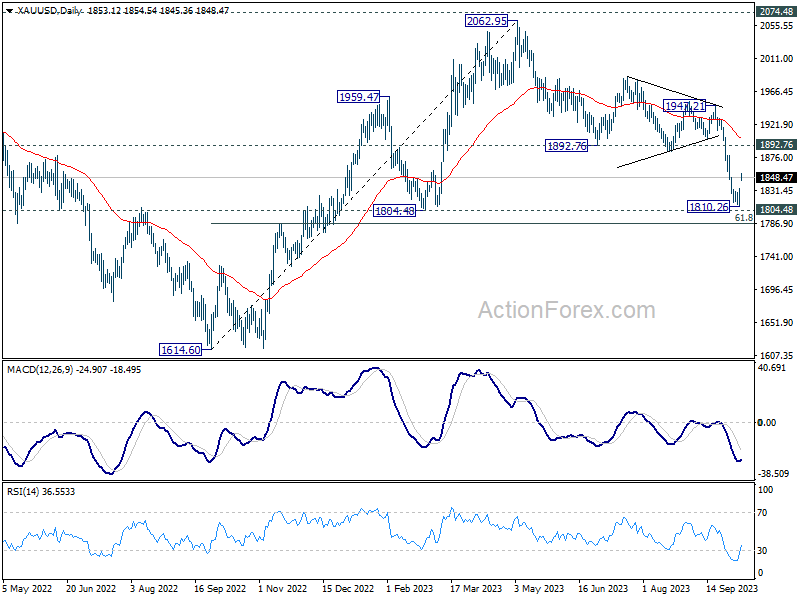

The immediate impact of these developments is most palpable in Gold. The precious metal’s resurgence marks short-term bottoming at 1810.26, just above 1804.48 medium-term support. If the ongoing geopolitical crises further deteriorate, we might see a continued upswing in the precious metal’s price. However, a significant barrier awaits at the 1900 handle, slightly above the 1892.76 support turned resistance. Return to normalized sentiment will inevitably refocus market attention on the anticipation of persistently high Fed interest rates and towering benchmark treasury yields, potentially exerting downward pressure on gold again.

In tandem with gold, WTI crude oil has also responded to the geopolitical shockwaves, posting robust gains. With 77.95 support remains unbreached, there’s an absence of concrete confirmation pointing towards reversal of the rally initiating at 63.67. However, it’s worth noting a marked attenuation in upside momentum recently, as seen in D MACD. Even though a more substantial rise isn’t off the table in the short term, the ceiling is likely to be established below 95.50 resistance, for an extended phase of range trading.

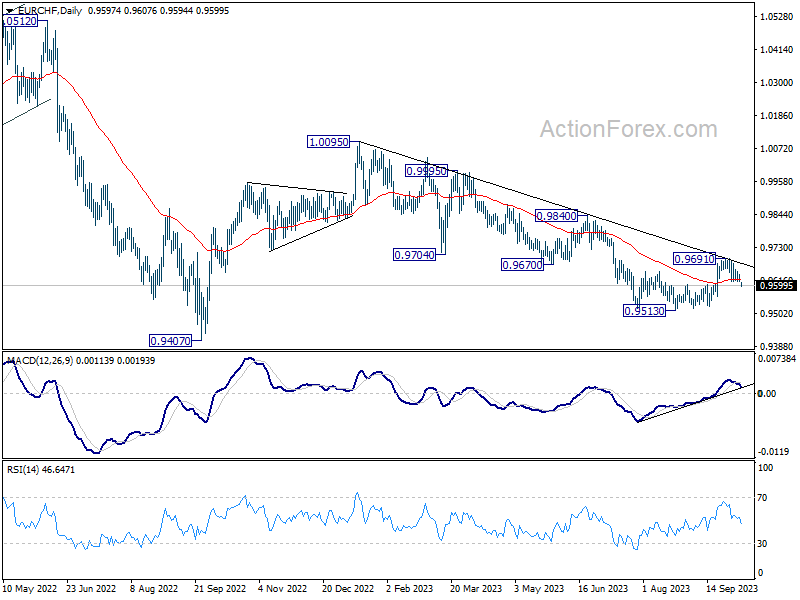

The currency markets are not immune to these developments either. EUR/CHF pair is emblematic of the shifts underway, with a decisive break of 55 D EMA arguing that that recovery from 0.9513 has completed at 0.9691. This comes on the heels a rejection by medium-term falling trend line resistance. If the pair fails to recapture ground above 55 D EMA in the coming days, deeper descent is likely on the cards, potentially surpassing the 0.9513 low to resume the broader downtrend originating from 1.0095.

Fed’s Bowman: Rate hike needed amid inflation, solid growth

Fed Governor Michelle Bowman emphasized her ongoing concerns about inflationary pressures, underscoring the need for sustained vigilance. Speaking on Saturday, she reiterated that, despite notable progress in curbing inflation, the levels remain worryingly high.

She highlighted the necessity for further rate hikes, stating, “it will likely be appropriate for the Committee to raise rates further and hold them at a restrictive level for some time to return inflation to our 2 percent goal in a timely way.”

Bowman pointed to the recent rise in the PCE index as a tangible indication of inflationary pressures. This increase, she believes, is partly attributed to climbing oil prices, which, if they persist or grow, could derail some of the achievements in inflation control observed over the past few months.

On a brighter note, Bowman acknowledged the overall positive health of the US economy. “Real gross domestic product has been growing at a solid pace,” she remarked, signifying a robust economic backdrop. This growth is supported by strong consumer spending, a rejuvenating housing sector, and encouraging labor market data that reflects consistent job gains.

However, Bowman concluded by emphasizing flexibility in the Fed’s approach, suggesting that monetary policy remains adaptable to the evolving economic landscape. “It is important to note that monetary policy is not on a pre-set course,” she clarified, ensuring that she and her colleagues will make informed decisions rooted in the most recent economic data and the broader implications for the economic future.

ECB’s Lagarde not pessimistic about short term outlook

In an interview with La Tribune Dimanche, fielding the topic of a possible recession risk in Europe, ECB President Christine Lagarde didn’t offer a direct response but instead focused on the preparations and countermeasures Europe has adopted. She highlighted, “This allows us to look towards the coming winter, if not calmly, then at least with a lot more confidence,” emphasizing the role of the Next Generation EU program, structural reforms, and the replenishment of over 90% of gas reserves.

Germany, a powerhouse of the European economy, was also discussed. Lagarde candidly noted that Germany’s previously successful economic model, which leveraged cheap energy supplies and significant export opportunities, especially to China, is undergoing transformation. She admitted that Germany is “one of the factors that is indeed weighing on the outlook for European growth.”

In addressing concerns about whether the ECB harbors a pessimistic view on the short-term economic horizon for Europe, Lagarde was clear, stating, “There are three reasons why we are not pessimistic.” She pointed to an expected rise in growth figures next year, a significant reduction in inflation, and a historically high employment rate in Europe that seems to be holding steady.

However, one of the challenges the European businesses face revolves around salary negotiations and wage structures. Lagarde posed, “The big question right now concerns businesses. Will they accept absorbing part of the salary increases that will be negotiated this year and next in their margins – which didn’t change much in 2022?”

The Week ahead: How US inflation and UK growth will shape the markets?

As we step into a holiday-shortened week in the US, investors and analysts alike are turning their focus towards the release of inflation data. An essential metric for financial markets, core CPI data can often offer essential insights into the ongoing inflationary pressures and their potential influence on Fed’s policy direction. While annual core CPI is expected to cool, it’s crucial to understand this is more about the base effect than a true reduction in inflation. The real meat of the matter lies in the monthly changes in this price index, especially the core.

Markets are forecasting a 0.3% month-on-month rise in core CPI, a figure slightly higher than what would align with the Fed’s 2% target. So, will this data end the ongoing debate regarding Fed’s own projected one more rate hike ? We’ll soon find out.

The upcoming release of the minutes from the Fed’s September meeting promises another opportunity for insights into the central bank’s mindset. As investors and analysts, we’re keen to grasp how strongly the central bank officials are considering an interest rate increase before 2023 draws to a close. With the next policy decision slated for November 1, these minutes could significantly impact market expectations, currently hovering at a little over a 40% likelihood of another 25 basis points hike either in November or December.

Meanwhile, across the Atlantic, BoE left market watchers somewhat baffled with its decision to halt rate hikes in September. While the decision was closely contested with a 5-4 vote, what stood out was the stance of the bank’s heavyweights. Notably, Governor Andrew Bailey, along with Deputies Ben Broadbent and Dave Ramsden, and Chief Economist Huw Pill, all leaned towards maintaining the status quo. Their collective weight in such decisions cannot be overlooked, and their unanimous preference to hold off on rate hikes was telling.

For a change in this stance, robust GDP data might be the ticket to sway these significant voices within the BoE. However, the next inflation data release could play the pivotal role in determining the bank’s next move.

Here are some highlights for the week:

- Monday: Germany industrial production. Eurozone Sentix investor confidence.

- Tuesday: Australia Westpac consumer sentiment, NAB business confidence; Italy industrial production; US NFIB small business index.

- Wednesday: Germany CPI final; Japan machine tool orders; Canada building permits; US PPI, FOMC minutes.

- Thursday: Japan bank lending, machine orders, PPI; UK GDP, production, trade balance; US CPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing; China CPI, PPI, trade balance; Swiss PPI; Eurozone industrial production; US import prices, U of Michigan consumer sentiment.

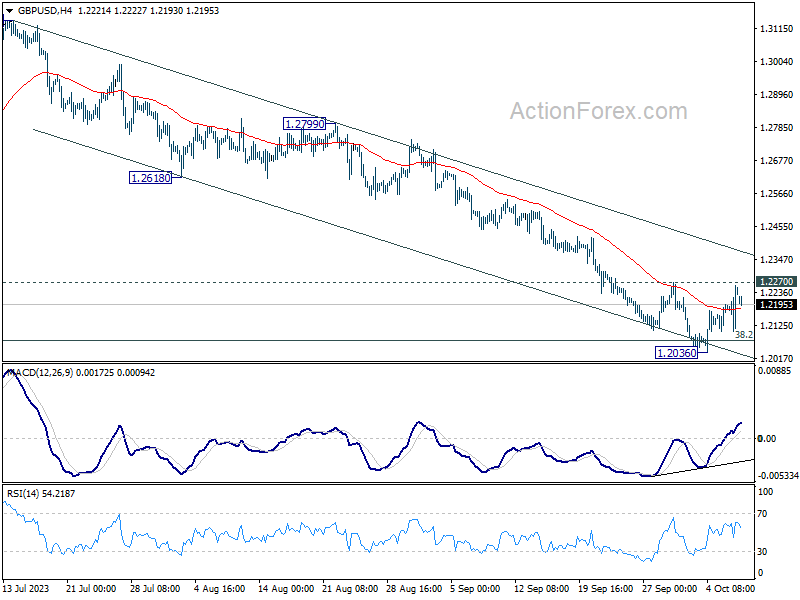

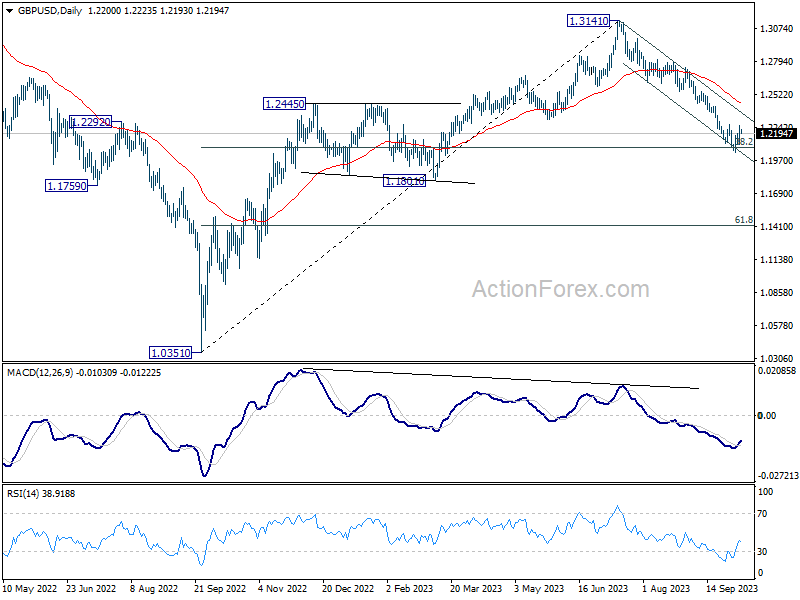

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2143; (P) 1.2202; (R1) 1.2298; More

GBP/USD dips mildly today but stays well inside range of 1.2036/2270. Intraday bias remains neutrla at this point. On the upside, firm break of 1.2270 resistance will confirm short term bottoming. Intraday bias will be back to the upside for stronger rebound. Nevertheless, rejection by 1.2270 will retain near term bearishness. Decisive break of 1.2075 fibonacci level would carry larger bearish implication and target 1.1801 support next.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2446) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany Industrial Production M/M Aug | -0.10% | -0.80% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Oct | -24 | -21.5 |

{kind=link}