Australian Dollar trades broadly lower in today’s Asian session, influenced by notable decline in Hong Kong and Chinese stock markets as driven by selloff in technology stocks in these regions. Additionally, there is growing investor caution ahead of impending economic data from China, which is anticipated to highlight deepened deflation and challenges in the export sector. This cautious sentiment has led to Australian Dollar being the weakest performers so far, with Swiss Franc, British Pound, and Kiwi following.

On the flip side, Japanese Yen, Dollar, and Euro are showing slight gains in what has been a relatively subdued session. Notably, apart from a few Yen currency pairs, most forex markets are trading within the ranges established on Friday, indicating the lack of significant volatility at the moment. However, this is expected to change as focus shifts to forthcoming economic inflation data from major economies including US, Japan, China, Australia, Switzerland, as well as UK GDP.

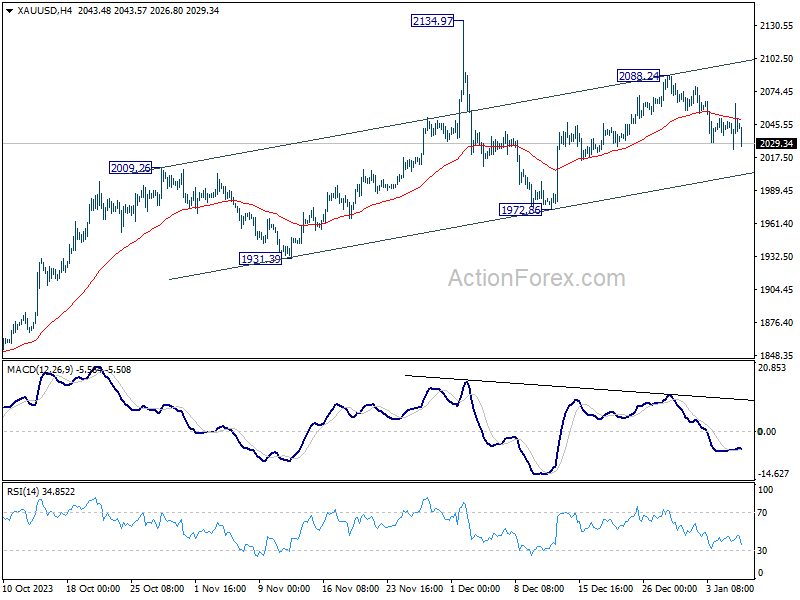

Technically, Gold’s recovery last Friday was rather brief. The decline from 2088.24 short term top is still in progress for near term channel support (now at 2004), which is close to 2000 psychological level. Strong rebound is expected from the channel to bring rebound, for resuming near term up trend through 2088.24. However, sustained break there will raise the chance of reversal and target 1972.86 support instead.

In Asia, at the time of writing, Hong Kong HSI is down -2.08%. China Shanghai SSE is down -1.08%. Singapore Strait Times is up 0.01%. Japan is on holiday.

Fed’s Logan emphasizes need for tight financial conditions to curb inflation

Dallas Fed President Lorie Logan, in her speech on Saturday, emphasized the importance of maintaining tight financial conditions to prevent resurgence of inflation. She expressed concern that if these conditions are not sustained, progress made in controlling inflation could be reversed.

Logan Logan underscored the significant role that restrictive financial conditions have played in “bringing demand into line with supply and keeping inflation expectations well-anchored”.

However, she noted a recent reversal in this trend, pointing out that long-term yields have relinquished much of the tightening observed over the summer. She warned, “We can’t count on sustaining price stability if we don’t maintain sufficiently restrictive financial conditions.”

Logan also addressed the Federal Reserve’s balance sheet runoff. She indicated that it might be appropriate to consider slowing the pace of this runoff, particularly as overnight reverse repurchase agreement balances approach lower levels.

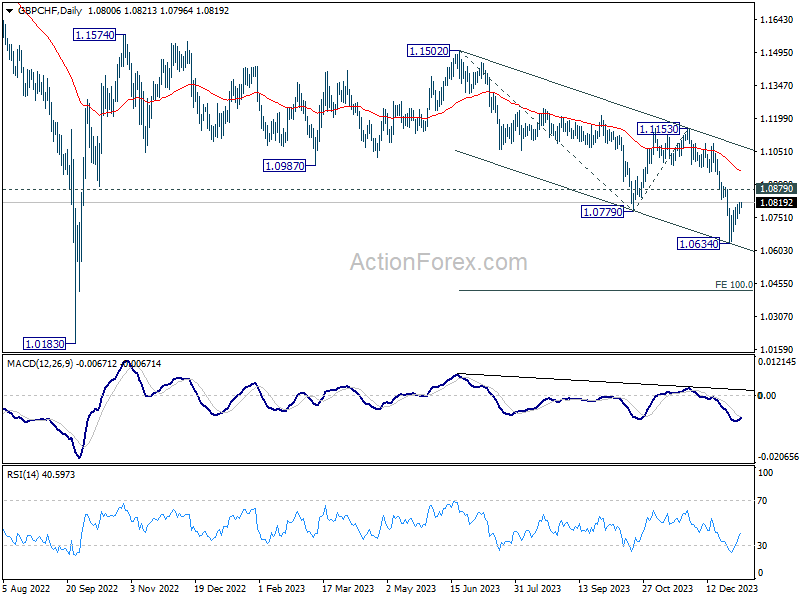

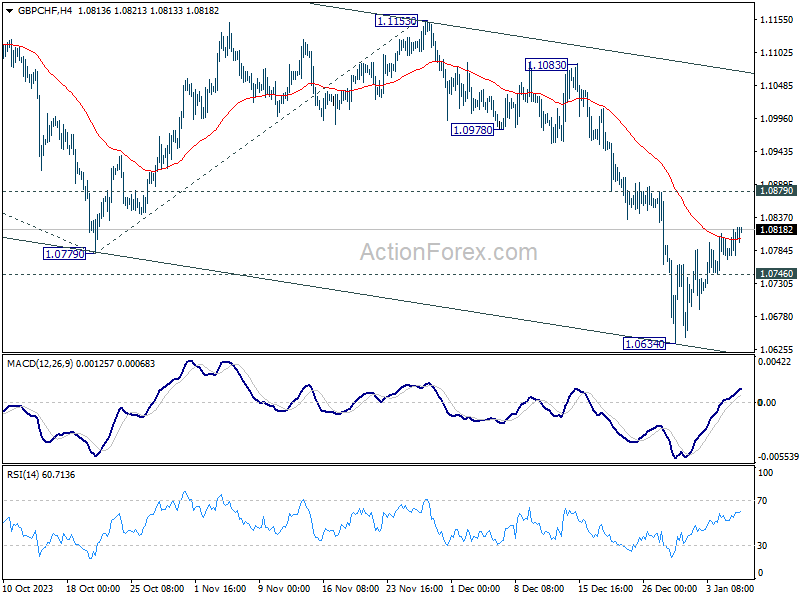

Swiss Franc awaits CPI, GBP/CHF in corrective recovery

Traders of Swiss Franc are closely monitoring Swiss CPI release today. Headline inflation is anticipated to increase from 1.4% yoy to 1.7% yoy in December. This expected rise aligns with SNB’s own conditional inflation forecast, which projects inflation to reaccelerate from 1.6% in Q4 of last year to 1.8% in Q1, peaking at 2.0% in Q2 before tapering off to 1.9% in Q4.

Regarding SNB’s monetary policy, current interest rate stands at 1.75%, which is comparatively unrestrictive. Unlike the more aggressive rate hikes implemented by counterparts like ECB and Fed, SNB’s past rate increases have had much less detrimental impact on the Swiss economy. Consequently, there is no immediate pressure for a rate cut, and it is generally anticipated that SNB will maintain current interest rate at least until Q3 of this year. Should today’s inflation reading surpass expectations, it could increase the likelihood of SNB holding interest rate unchanged for the remainder of the year.

GBP/CHF recovered after hitting 1.0634, being supported by falling channel support line. Price actions since there are corrective looking. Also, the recovery is kept below 1.0879 minor resistance. Thus, outlook is staying bearish. Break of 1.0746 minor support will bring retest of 1.0634 low first. Further break there will resume recent down trend to 100% projection of 1.1502 to 1.0779 from 1.1153 at 1.0430.

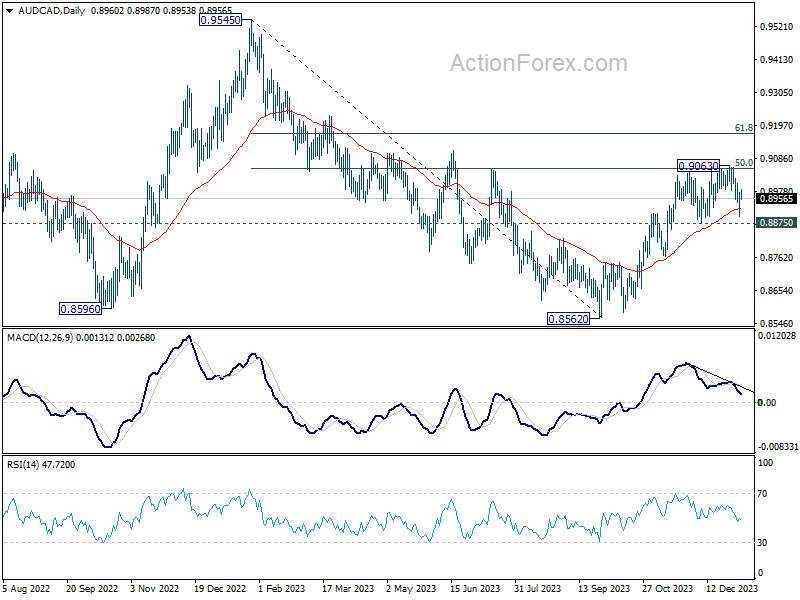

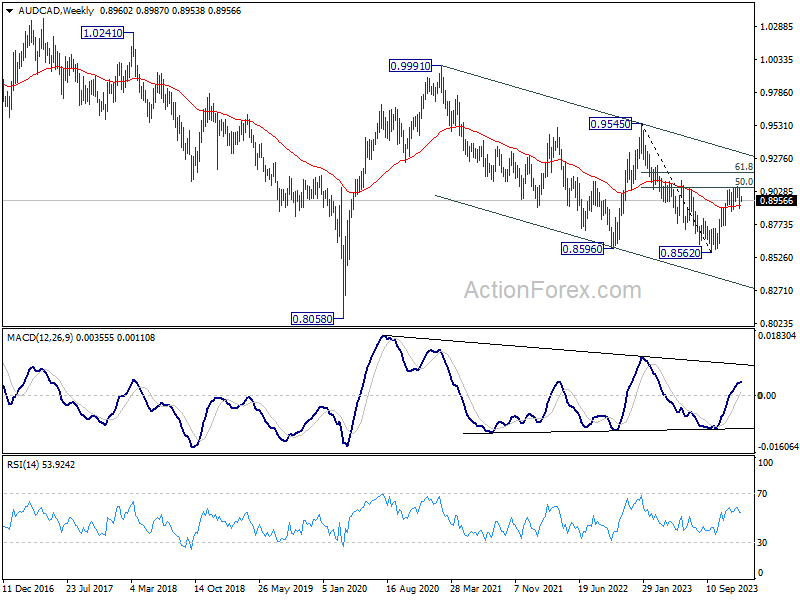

AUD/CAD eyes 0.8875 support, await Australia CPI

The recovery of AUD/CAD since last September has been largely attributed to the divergence in monetary policies between RBA and BoC. While RBA extended its tightening cycle, BoC’s interest rate reached a plateau. The rally in December was particularly driven by speculations of an additional RBA rate hike, although the momentum lost steam after briefly surpassing 0.9 handle.

Technically speaking, this recovery from 0.8562 is more corrective looking than impulsive. The notable decline since the start of the year indicates that a short term top was already formed at 0.9063, on bearish divergence condition in D MACD. Break of 0.8875 support should also confirm rejection by 50% retracement of 0.9545 to 0.8562 at 0.9054. That would turn near term outlook bearish for retest 0.8562 low.

The upcoming release of Australia’s monthly CPI data could serve as a catalyst for a downturn in AUD/CAD. However, the sustainability of downside momentum, especially in breaking through 0.8562 support, will very much depend on which central bank between RBA and BoC starts cutting interest rates first and the subsequent policy paths they adopt.

Global Focus on Inflation Data: US, Japan, China, Australia and Swiss

Inflation data across various economies are set to be the primary focus for financial markets this week. In the US, the pace of core inflation’s deceleration will be closely monitored, as it is a crucial determinant for the timing of Fed’s first interest rate cut. While a rate cut in March is still considered unrealistic, any lower-than-expected figures in the upcoming CPI and core CPI data could lead traders to increase their bets on a sooner-than-anticipated rate reduction.

In Japan, Tokyo CPI is widely regarded as a reliable precursor to the national CPI figures. Upcoming labor earnings data will also be essential, offering insights into wage growth pressures. These factors are critical for BoJ to consider as it deliberates on exiting negative interest rate policies this year.

China is slated to release several key economic indicators, including CPI,PPI, and trade balance data. The market’s attention will be focused on the depth and duration of China’s deflationary trends and the ongoing slump in exports and imports. For Australia, the release of the monthly CPI will provide some perspective on inflationary developments and whether any new data might prompt RBA to respond, given its “low tolerance” for inflation surprises.

Additionally, the UK will report GDP and production data, while Eurozone will release Sentix investor confidence figures. Switzerland’s CPI data will also be featured, adding to the wealth of economic information influencing markets in Europe.

Here are some highlights for the week:

- Monday: Germany factory orders, trade balance; Swiss CPI, retail sales; Eurozone Sentix investor confidence, retail sales.

- Tuesday: Japan Tokyo CPI, household spending; Australia retail sales, building approvals; Swiss unemployment rate; Germany industrial production, France trade balance; Eurozone unemployment rate; Canada building permits, trade balance; US trade balance.

- Wednesday: Japan average cash earnings; Australia monthly CPI; France industrial production.

- Thursday: Australia trade balance; Japan leading index; ECB monthly bulletin; US CPI, unemployment rate.

- Friday: Japan banking lending, current account; China CPI, PPI, trade balance; UK GDP, production, trade balance; France consumer spending; US PPI.

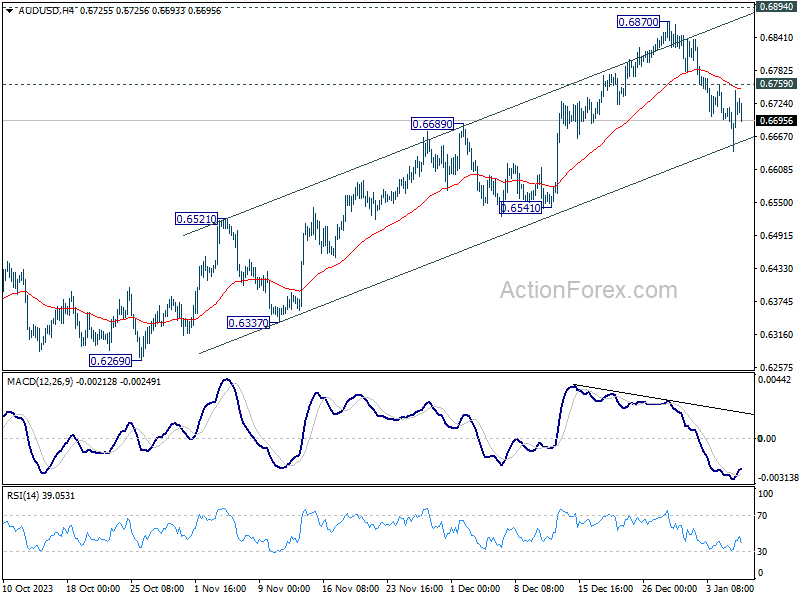

AUD/USD Daily Report

Daily Pivots: (S1) 0.6655; (P) 0.6702; (R1) 0.6762; More…

With 0.6759 minor resistance intact, further decline is expected in AUD/USD. Fall from 0.6870 short term top would target 55 D EMA (now at 0.6612). Some support could be seen there to bring rebound on first attempt. On the upside, however, break of 0.6759 minor resistance will suggest that the pull back is over, and bring retest of 0.6870 instead.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany Factory Orders M/M Nov | 1.10% | -3.70% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 17.9B | 17.8B | ||

| 07:30 | CHF | Real Retail Sales Y/Y Nov | 0.00% | -0.10% | ||

| 07:30 | CHF | CPI M/M Dec | -0.10% | -0.20% | ||

| 07:30 | CHF | CPI Y/Y Dec | 1.70% | 1.40% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | -15.4 | -16.8 | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | 93.8 | |||

| 10:00 | EUR | Eurozone Industrial Confidence Dec | -9.5 | |||

| 10:00 | EUR | Eurozone Services Sentiment Dec | 4.9 | |||

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | -15.1 | -15.1 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | -0.10% | 0.10% |

{kind=link}