Trading activity is relatively subdued today, with most major currency pairs and crosses hovering within the previous day’s range. Australian and New Zealand Dollars are showing some resilience, maintaining their position as the firmer currencies, albeit without significant momentum. Swiss Franc has also edged higher in the daily performance chart, benefiting a recovery against both the Euro and the Sterling. On the other hand, Dollar and Yen find themselves on the softer side, while Euro and the Pound show mixed performances.

The spotlight for the rest of the day is firmly on the upcoming FOMC minutes. Investors and traders alike will dissect for clues regarding the timing of the first rate cut, although expectations for concrete hints are tempered. However, it should also be pointed out that the narrative within certain market segments is increasingly complex.

Discussions are emerging around the possibility of Fed’s next move being a rate hike rather than a cut. This debate gained traction following comments from former US Treasury Secretary Lawrence Summers, who last week suggested a “meaningful chance” of the next adjustment being an “upside in rates, not downwards.”

This perspective is echoed by some economists who acknowledge the formidable challenges that lie in the final stages of the inflation battle. However, more would believe, at least at this stage, that maintaining the current interest rate level for an extended period may be more pragmatic than implementing another hike, only to revert to cuts more swiftly.

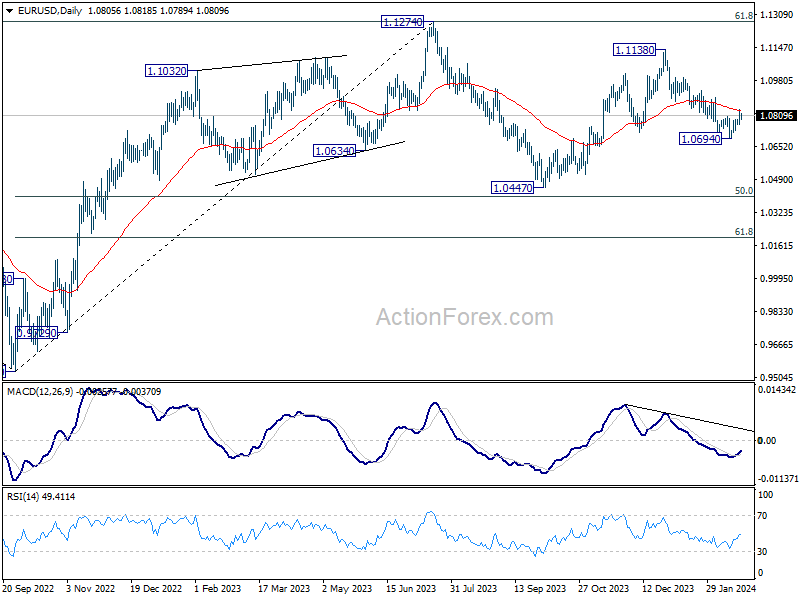

From a technical standpoint, EUR/USD’s response to FOMC minutes will be particularly telling. Sustained, decisive break of 55 D EMA (now at 1.0832) will argue that the pull back from 1.1138 has completed at 1.0694. That would also argue that rise from 1.0447 is ready to resume through 1.1138 to retest 1.1274 high. Meanwhile, rejection by 55 D EMA will retain near term bearishness for another fall through 1.0694. We could know the answer very soon. The market’s reaction to the FOMC minutes could provide clarity on this front shortly.

In Europe, at the time of writing, FTSE is down -0.95%. DAX is up 0.17%. CAC is flat. UK 10-year yield is up 0.0132 at 4.057. Germany 10-year yield is up 0.0212 at 2.398. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI rose 1.57%. China Shanghai SSE rose 0.97%. Singapore Strait Times fell -0.83%. Japan 10-year JGB yield fell -0.0070 to 0.726.

Fed’s Barkin: Recent data makes things harder for Fed

Richmond Fed President Thomas Barkin characterized the stronger-than-expected inflation data for January as a significant challenge.

At an interview, Barkin acknowledged that the recent date “definitely did not make things easier” for Fed. Instead, “it made things harder.” Nevertheless, he was still cautious about overemphasizing the significance of these figures, citing “seasonal measurement issues” that might distort the month’s data.

Barkin also emphasized that the US States is “on the back end of its inflation problem.” The critical question is “how much longer it will take” for inflation to align with Fed’s target.

Japan’s government reports stall in consumption and manufacturing slide

The Japanese government maintains its assessment that the economy is “recovering at a moderate pace”, but with a of caution with the observation that the recovery “recently appears to be pausing.”

A critical shift noted in the Monthly Economic Report concerns private consumption, which has been downgraded from “picking up” to “pausing for picking up.” Additionally, while there was optimism surrounding industrial production, the report highlights a recent decline in manufacturing activities attributed to production and shipment suspensions by some automotive manufacturers.

The report maintains unchanged assessments in several other economic indicators. Business investment and exports, similar to private consumption and industrial production, are described as “pausing for picking up.”

On a positive note, corporate profits are reported to be improving overall, and firms’ judgments on current business conditions are becoming more favorable.

Additionally, employment situation is showing signs of improvement. Consumer prices, meanwhile, continue to rise “moderately”.

Australia Westpac leading index falls to -0.25%, sub-par growth to continue

Australia’s economy is bracing for continued “sub-par growth” into 2024, as indicated by the downturn in the Westpac Leading Index, which dipped from -0.01% to -0.25% in January. Westpac anticipates the economic growth rate to hover around an annualized 1.3% in the first half of this year, marking an improvement from the latter half of 2023’s 0.8%, yet remaining significantly below the usual trend rate of about 2.5%.

In the realm of monetary policy, Westpac’s analysis suggests a measured approach by RBA. The central bank is expected to take additional time to gain “sufficient confidence” that inflation will revert to target range within a reasonable timeframe. Economic indicators leading up to the March meeting are projected to reinforce a narrative of “weak growth and demand environment domestically,” which would justify RBA’s decision to maintain its current policy stance.

This cautious period of observation is likely to precede any shift towards a more definitive “on hold” position by the Board, with considerations for interest rate cuts anticipated to emerge further down the line.

Japan’s exports rises 11.9% yoy in Jan, imports down -9.6% yoy

Japan’s export recorded 11.9% yoy increase to JPY 7333B in January, marking the second consecutive month of growth. However, imports saw a contrasting trend, decreasing by -9.6% yoy to JPY 9091B. This resulted in a trade deficit of JPY -1758B for the month.

A notable highlight from the trade data was Japan’s trade surplus with the US, amounting to JPY 415B, as exports reached an all-time high for the month at JPY 1.42T.

Conversely, Japan faced a JPY -959.52B trade deficit with China, another significant trading partner. Despite this deficit, exports to China were supported by strong demand for chip-making equipment and cars.

On seasonally adjusted basis, exports registered decline of -3.6% mom to JPY 8765B, while imports fell more sharply by -10.5% mom to JPY 8230B. This shift led to trade surplus of JPY 235B.

Australia’s Q4 wage growth hits 4.2%, driven by sharp public sector increase

Australia’s wage price index rose 0.9% qoq in Q4, decelerating from the previous quarter’s 1.3% qoq increase, but in line with market expectations. Annually, wage growth ticked up from 4.1% yoy to 4.2% yoy, marking the highest rate since Q1 2009.

A closer look at sector-specific data reveals that private sector annual wage growth slowed slightly from 4.3% yoy to yoy. In contrast, public sector wage growth accelerated sharply from 3.5% yoy to 4.3% yoy, the highest rate since Q1 2010.

The surge in public sector wages underscores the impact of cyclical patterns of enterprise bargaining, as highlighted by Michelle Marquardt, ABS head of prices statistics. She noted, “In the December quarter 2023, 38 percent of public sector jobs saw a wage rise, considerably higher than the 29 percent from the same quarter in the previous year.”

Furthermore, average hourly wage change for these jobs escalated to 4.3%, surpassing 2.8% recorded at the same time last year and achieving the highest level since September 2008.

USD/CHF Mid-Day Outlook

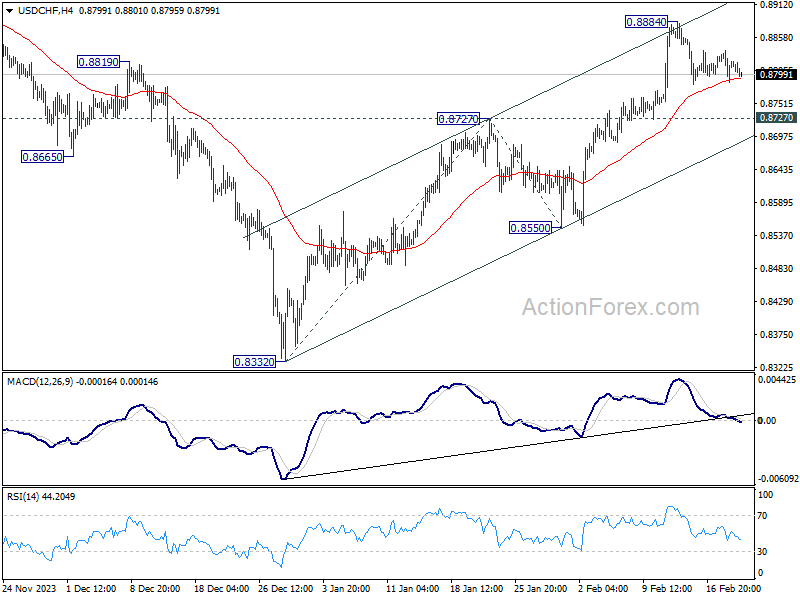

Daily Pivots: (S1) 0.8791; (P) 0.8814; (R1) 0.8843; More….

USD/CHF dips mildly today but stays in range of 0.8727/8884. Intraday bias remains neutral and more consolidations could be seen. With 0.8727 resistance turned support intact, further rally is still expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

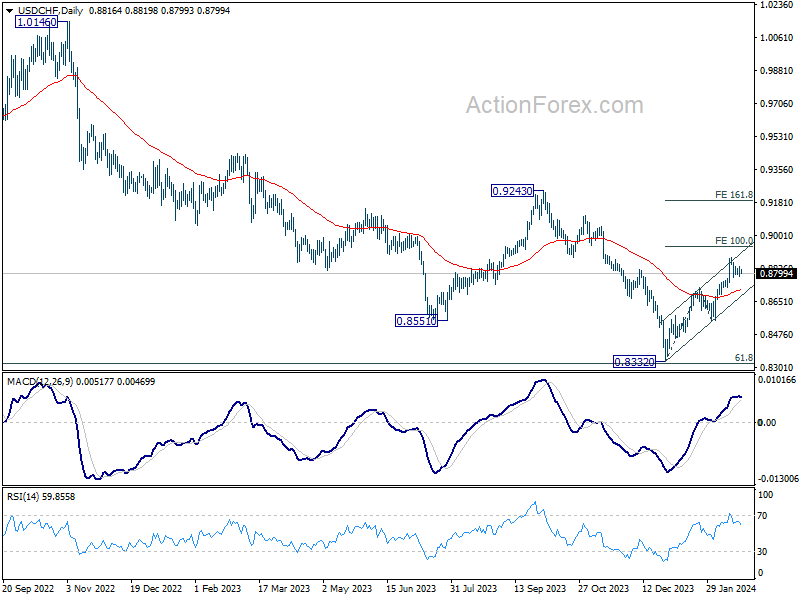

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It’s still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q4 | 0.90% | 0.40% | 1.20% | |

| 21:45 | NZD | PPI Output Q/Q Q4 | 0.70% | 0.40% | 0.80% | |

| 23:50 | JPY | Trade Balance (JPY) Jan | 0.24T | -0.23T | -0.41T | -0.44T |

| 00:00 | AUD | Westpac Leading Index M/M Jan | -0.10% | 0.00% | ||

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.90% | 0.90% | 1.30% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Jan | -17.6B | -18.4B | 6.8B | 6.5B |

| 13:30 | CAD | New Housing Price Index M/M Jan | -0.10% | 0.10% | 0.00% | |

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | -16 | -16 | ||

| 19:00 | USD | FOMC Minutes |

{kind=link}