Dollar’s rebound on upbeat US jobs and services data proved short-lived, as the greenback faded again in early Friday trading. The greenback failed to hold gains amid a broader risk-on tone with both S&P 500 and NASDAQ closed at fresh record highs.

Strong employment data gave policymakers room to wait, especially as they assess the fallout from tariffs following the July 9 truce deadline. Futures markets now assign a 95% probability Fed will hold rates steady at this month’s meeting. Meanwhile, expectations for aggressive easing are also fading. Markets now price in less than a 40% chance of three cuts in 2025, compared to higher odds earlier this month. Even so, reduced Fed cut expectations haven’t translated into Dollar strength.

The greenback also found no lift from Washington. The House narrowly passed President Donald Trump’s tax-and-spending bill, marking a major political win but also reviving deficit concerns. The IMF flagged the bill’s likely impact on worsening the fiscal outlook, noting in its press briefing that fiscal consolidation remains a priority the US has yet to address. The Fund will update its growth projections in late July to reflect the bill’s effects.

On trade, Trump escalated his tactics by announcing that tariff letters will be sent out to individual countries starting today. This would mark a clear pivot from deal-based diplomacy toward flat-rate enforcement. Each country will reportedly be told what tariff rates — typically between 20% and 30%. Trump called the unilateral approach “easier” and “more efficient.”

For the week so far, Sterling is still the weakest major currency. Dollar ranks second from the bottom, just ahead of Yen. Loonie leads the performance board, followed by Swiss Franc and Aussie. Euro and Kiwi are holding middle ground as the week winds down.

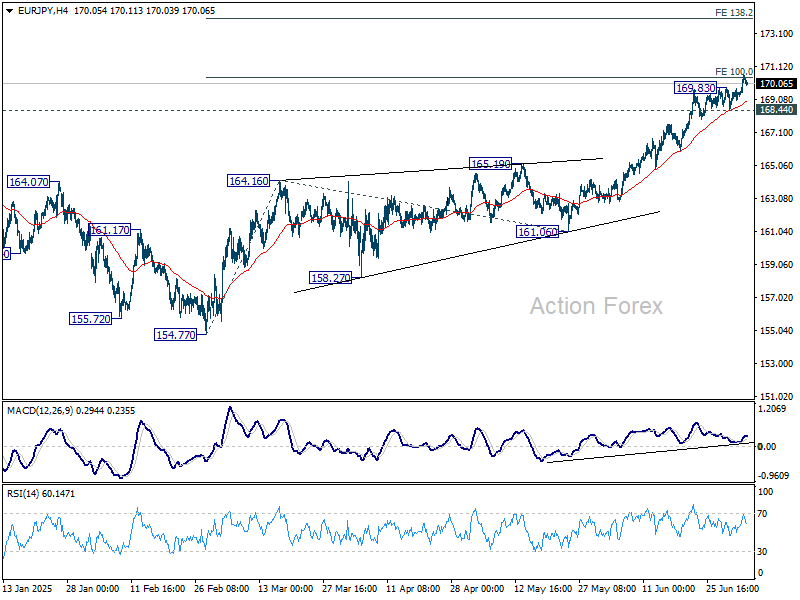

Technically, EUR/JPY’s rally resumed after brief consolidations and met 100% projection of 154.77 to 164.16 from 161.06 at 170.45. Further rally is expected as long as 168.44 support holds. Firm break of 170.45 will pave the way to 138.2% projection at 174.03.

In Asia, at the time of writing, Nikkei is up 0.12%. Hong Kong HSI is down -0.20%. China Shanghai SSE is up 0.87%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.014 at 1.457. Overnight, DOW rose 0.77%. S&P 500 rose 0.83%. NASDAQ rose 1.02%. 10-year yield rose 0.055 to 4.348.

Japan household spending surges 4.7% yoy in May, fastest in bearly three years

Japan’s household spending rose 4.7% yoy in May, sharply above expectations of 1.2% yoy and marking the fastest pace of growth since August 2022. Seasonally adjusted monthly spending also surged 4.6% mom, well ahead of the 0.4% mom consensus and the strongest gain since March 2021. The internal affairs ministry attributed the jump to robust demand for cars, dining out, and summer-related appliances.

By category, transportation and communications spending soared 25.3% yoy, while recreation and leisure climbed 11.1% yoy. Furniture and home appliance purchases rose 9.3% yoy as households prepared for a hot summer. Food spending, which accounts for nearly a third of total consumption, rose 1.0% yoy as price pressures eased and dining out increased.

Officials highlighted that the three-month moving average of household spending has remained positive since December 2024, suggesting a durable recovery in consumer demand.

Fed’s Bostic sees prolonged inflation from tariff impact

Fed’s Raphael Bostic signaled strong resistance to near-term rate cuts, citing uncertainty around trade policy and a still-resilient US economy. “This is no time for significant shifts in monetary policy,” he said, emphasizing that the FOMC should avoid decisions it may be forced to “quickly reverse”. With macro conditions steady, Bostic sees “space for patience” while waiting for greater clarity.

The Atlanta Fed chief pushed back on assumptions that the economic impact of Trump administration’s tariff and fiscal policies would be “a short and simple one-time shift in prices”. Instead, he argued that the adjustment process will likely take a year or more, and that both prices and growth may respond in drawn-out, non-linear ways. The implication is that the economy may undergo a “longer period of elevated inflation readings” as it digests structural shifts.

Bostic remains at the cautious end of the FOMC, projecting just one rate cut this year—compared to the median forecast of two.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1713; (P) 1.1762; (R1) 1.1805; More…

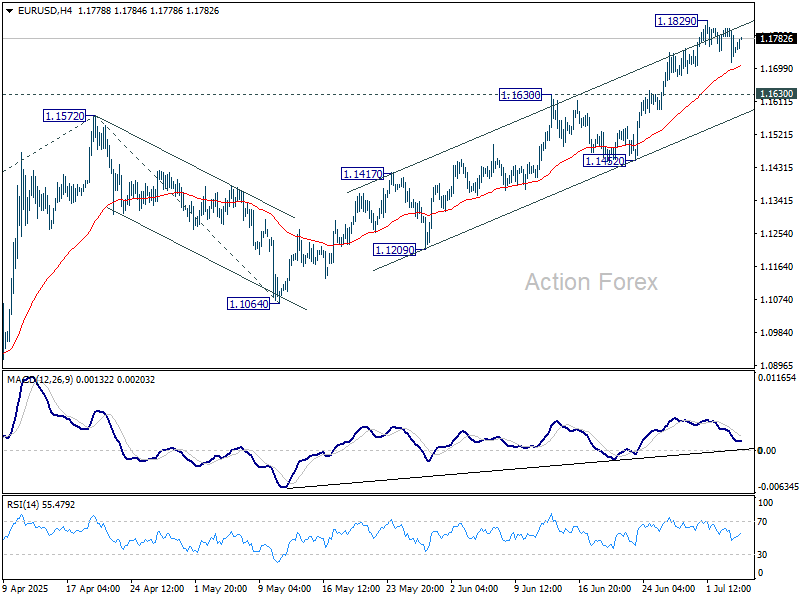

EUR/USD is staying below 1.1829 despite today’s recovery. Intraday bias remains neutral and more consolidations could be seen. Deeper retreat cannot be ruled out, but downside should be contained by 1.1630 resistance turned support to bring another rally. On the upside, break of 1.1829 will target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

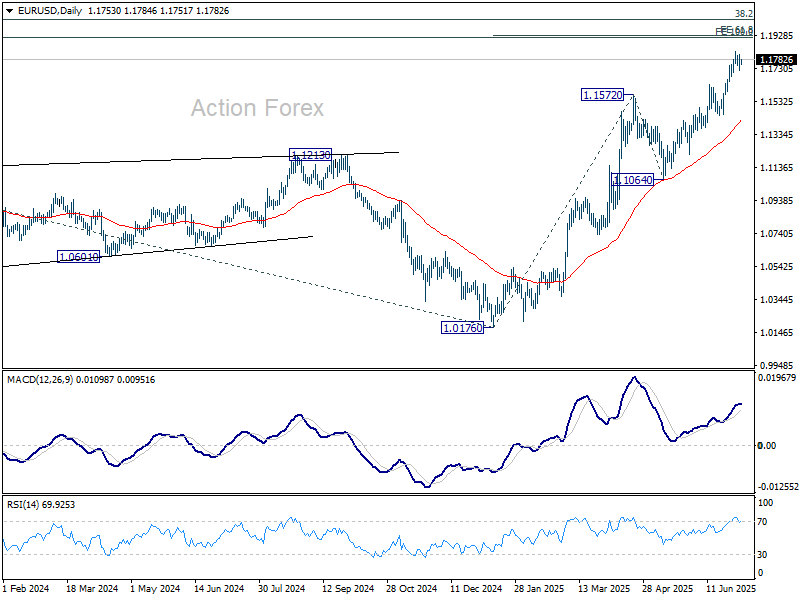

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

{kind=link}