Dollar steadied today, recovering modestly after yesterday’s selling, though the move lacked conviction. With investors convinced the Fed will cut rates next week, the greenback remains capped, unable to mount a broader rebound. For now, the greenback is only outperforming Yen and Loonie. Yen remains under pressure from buoyant risk appetite, with the Nikkei setting fresh records just shy of the 45,000 mark. Loonie, meanwhile, is weighed down by expectations that the BoC will resume easing at its upcoming meeting.

Attention later in the session may briefly turn to University of Michigan consumer sentiment and inflation expectations. Still, any reaction is likely to be fleeting, as traders begin winding down ahead of the weekend and with next week’s FOMC meeting looming.

Weekly performance rankings show Aussie comfortably in the lead, followed by Kiwi and then Sterling. The Pound drew some support from a BoE survey showing rising public inflation expectations. At the bottom of the table, Yen is the weakest performer, followed by Loonie and then Euro. Dollar and Swiss Franc are positioned in the middle.

In Europe, at the time of writing, FTSE is up 0.36%. CAC is down -0.06%. CAC is down -0.26%. UK 10-year yield is up 0.047 at 4.657. Germany 10-year yield is up 0.06 at 2.72. Earlier in Asia, Nikkei rose 0.89%. Hong Kong HSI rose 1.16%. China Shanghai SSE fell -0.12%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.024 to 1.602.

UK inflation expectations rise, BoE survey shows

The BoE/Ipsos Inflation Attitudes Survey showed UK households nudging inflation expectations higher. Median expectations for inflation over the next year rose to 3.6% from 3.2% in May, while two-year expectations climbed to 3.4% from 3.2%. Longer-term inflation expectations, five years out, also ticked up to 3.8% from 3.6%.

Concerns over rising prices were tied to broader pessimism about growth. By a margin of 69% to 6%, respondents said the economy would end up weaker rather than stronger if inflation accelerated, compared with 67% to 5% in May.

On the interest rate outlook, 33% of respondents expected rates to rise over the next 12 months, unchanged from May. But more people now expect stability, with 26% seeing no change versus 21% in May. The share expecting cuts fell to 29% from 34%, suggesting households are adjusting to the prospect of “higher for longer” rates.

When asked what would be best for the economy, 33% favored lower rates, down from 37% in May. Meanwhile, 28% preferred no change, up from 26%, and 14% wanted higher rates, up slightly from 12%. The responses suggest growing acceptance that policy will remain restrictive even as concerns about inflation remain elevated.

UK GDP stalls in July, services offset weak production

UK GDP was flat in July, matching expectations, as modest growth in services and construction offset a sharp drop in production. Services output rose 0.1% and construction gained 0.2%, while production fell -0.9%, highlighting ongoing weakness in the industrial sector.

Over the three months to July, GDP rose 0.2% compared with the previous three-month period. Services expanded 0.4% and remained the key driver of growth, while production fell -1.3% and construction rose 0.6%.

ECB officials stress uncertainty, keep options open after rate hold

Several ECB policymakers weighed in after the Governing Council held deposit rate steady at 2.00% yesterday.

Latvian member Martins Kazaks argued the central bank should not provide forward guidance given high geopolitical and economic uncertainty. He said December’s meeting will be crucial, as new staff forecasts will help determine whether inflation is deviating from target in a significant or persistent way.

Kazaks also flagged external factors, including the Euro’s strength— which can suppress import prices— and potentially deflationary Chinese exports as downside risks. “Uncertainty is high,” he said, adding this justifies a cautious, meeting-by-meeting policy stance.

Olli Rehn of Finland struck a similar note, warning about the disinflationary impact of cheaper energy and a stronger currency. He stressed the importance of avoiding inflation moving “too much below or too much above” the 2% objective,.

France’s Francois Villeroy de Galhau left the door open to further easing, saying “another rate cut is entirely possible” in coming meetings.

NZ BNZ manufacturing slips to 49.9, sector weakness persists, optimism patchy

The latest BusinessNZ PMI showed New Zealand’s manufacturing sector stalling in August, with the index slipping to 49.9 from 52.8. BusinessNZ’s Catherine Beard noted the industry “has yet to turn the corner toward sustained growth,” with the reading underscoring patchy conditions and fragile confidence despite being only marginally below the neutral threshold.

The breakdown highlighted a mixed picture. New Orders rose strongly to 55.2, the highest in two years, hinting at improving demand momentum, while raw material deliveries remained in expansion at 50.5. Offsetting this, production fell to 46.6, while employment (49.1) and finished stocks (47.1) also contracted, dragging the overall index lower.

Nearly six in ten respondents offered negative comments, citing flat sales, customer caution, rising costs, and global uncertainty as key drags. Although the proportion of negative feedback has eased from June’s high, sentiment remains weak, and businesses see recovery as tentative at best.

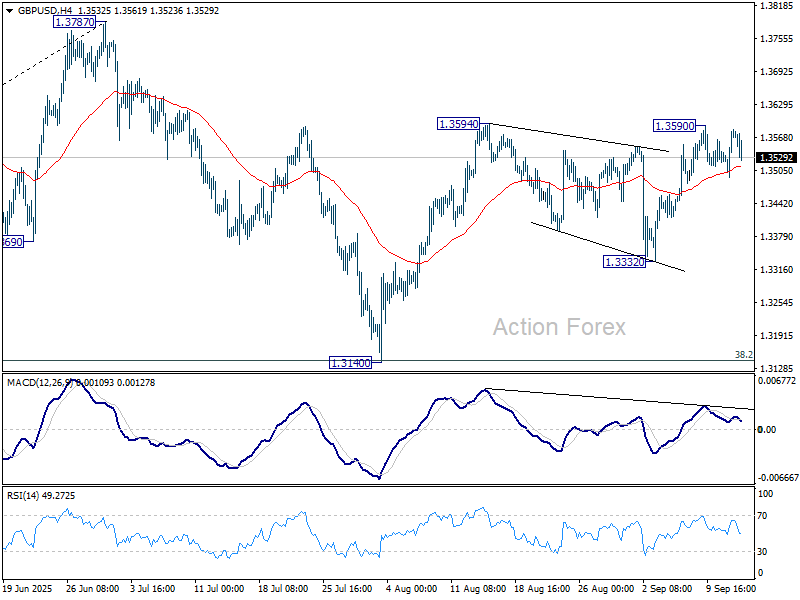

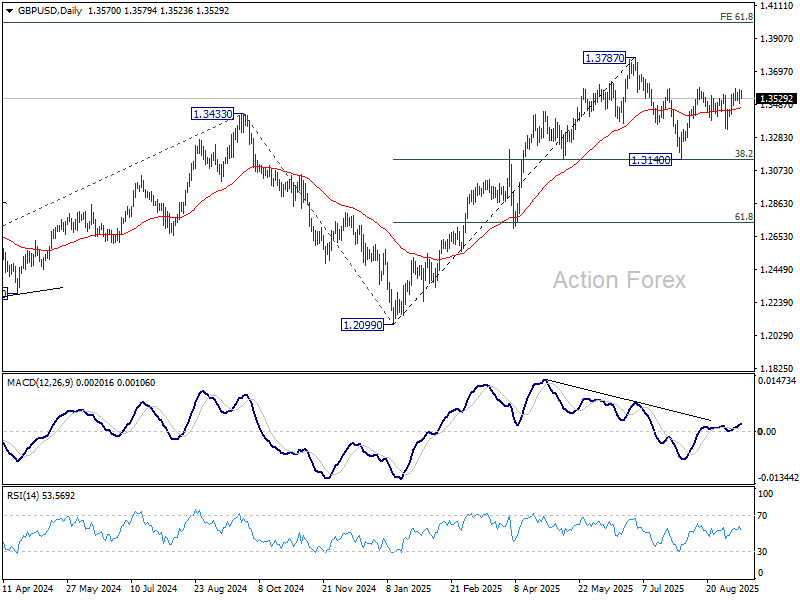

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3517; (P) 1.3550; (R1) 1.3606; More…

GBP/USD retreats mildly as consolidations continues below 1.3590 and intraday bias stays neutral. Further rise is expected with 1.3332 support intact. Firm break of 1.3594 will resume the rally from 1.3140 and target a retest on 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

{kind=link}