Gold stole the spotlight in global markets today, surging past the 4,000 mark for the first time ever as investors poured into the metal amid mounting geopolitical risks and growing conviction that the Fed will deliver another rate cut later this month. The historic milestone marks another powerful leg in Gold’s multi-year rally.

The metal has now gained more than 50% year-to-date and has doubled in value over the past three years, outperforming most major asset classes. The rally has been powered by a potent combination of central bank buying, ETF inflows, and expectations of monetary easing, alongside a steady bid from investors seeking protection against global instability.

Still, questions remain about whether the metal can sustain its hold above 4,000, particularly as Dollar shows signs of rebound across currency markets. Technical indicators suggest conditions are stretched, and a short-term pullback could follow if profit-taking accelerates around the milestone level. But underlying momentum remains firmly bullish as long as expectations for rate cuts persist.

In Asia, Japanese prime minister-in-waiting Sanae Takaichi faces early headwinds from her ruling coalition partner Komeito. The socially liberal party, long a brake on the LDP’s hawkish tendencies, has criticized Takaichi’s rhetoric toward foreigners and her past visits to the Yasukuni Shrine, a move likely to strain relations within the alliance.

While Takaichi is still expected to secure parliamentary approval later this month to become Japan’s first female prime minister, LDP sources say the vote could be delayed beyond the original October 15 date as negotiations drag on. Komeito’s leader Tetsuo Saito said talks with Takaichi lasted 90 minutes without a resolution, with more discussions planned in the coming days.

Moving to the U.S., investors are watching for clues from the FOMC minutes and a series of Fed speeches later today. With the government shutdown stretching into its second week, many analysts believe the absence of key data will encourage policymakers to deliver another “insurance cut” at the October 29 meeting rather than risk policy overtightening. Market pricing reflects that conviction: Fed fund futures now imply a 95% probability of a 25bps cut this month.

For the week so far, Loonie leads gains, followed by Dollar and Aussie, while Yen, Kiwi, and Euro trail at the bottom. The Kiwi remains under pressure after the RBNZ’s dovish 50bps cut. Sterling and Swiss Franc trade quietly mid-pack.

In Europe, at the time of writing, FTSE is up 0.81%. DAX is up 0.58%. CAC is up 0.83%. UK 10-year yield is down 0.022 at 4.704. Germany 10-year yield is down -0.039 at 2.673. Earlier in Asia, Nikkei fell -0.45%. Hong Kong HSI fell -0.48%. China was still on holiday. Singapore Strait Times fell -0.36%. Japan 10-year JGB yield rose 0.023 to 1.704.

RBNZ delivers 50bps cut, signals readiness to ease further if needed

RBNZ delivered a larger 50 bps rate cut, lowering the Official Cash Rate (OCR) to 2.50% at today’s meeting. The central bank maintained its easing bias, saying it “remains open to further reductions in the OCR” to ensure inflation returns sustainably to 2% over the medium term.

Minutes of the meeting showed the Monetary Policy Committee debated between a 25bps and 50bps move, with the majority favoring a bolder step to mitigate downside risks to medium-term growth and inflation. The Committee judged that prolonged spare capacity warranted a “clear signal” to support consumption and investment, helping anchor expectations amid a slowing economy.

While the Q2 GDP contraction was “considerably larger than expected,” the RBNZ attributed much of the weakness to temporary seasonal factors. It expects the distortion to reverse later in the year and said it does not see the short-term softness as materially altering the broader policy outlook.

The central bank noted that it had only marginally revised down its assessment of spare capacity but acknowledged “some downside risk” to activity. Inflation is projected to converge toward the 2% midpoint in the first half of next year, supported by easing tradables inflation and gradually moderating domestic cost pressures.

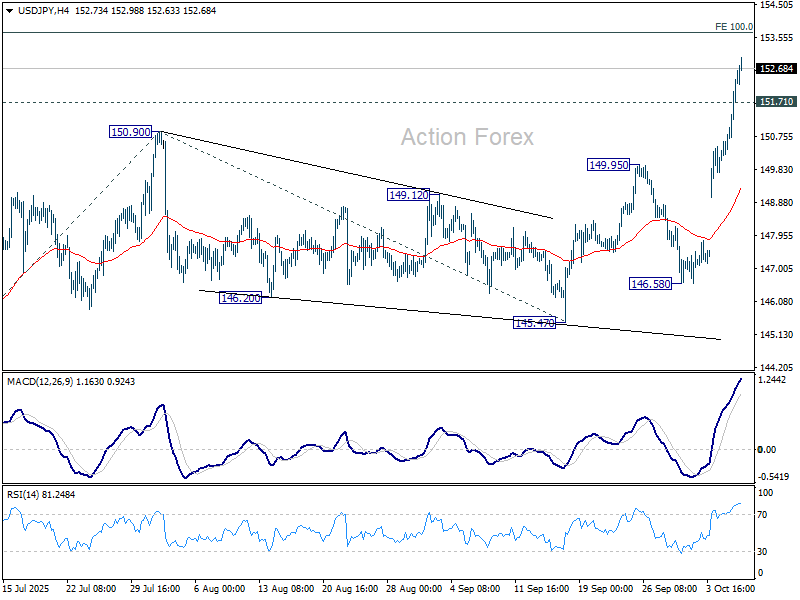

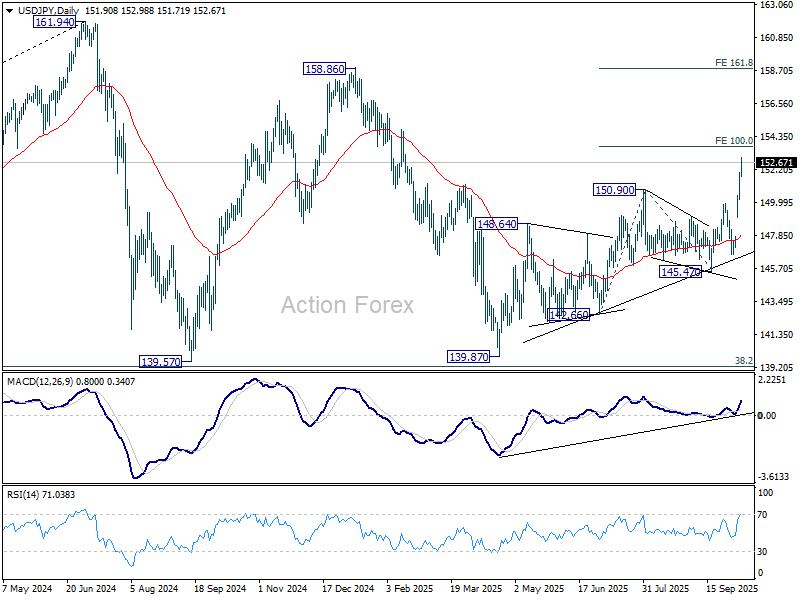

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.72; (P) 151.39; (R1) 152.55; More…

Intraday bias in USD/JPY stays on the upside for the moment, and further rally should be seen to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. On the downside, below 151.71 minor support will turn bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

{kind=link}