{kind=link}

A volatile trading environment looks all but guaranteed as markets face a rare clustering of major event risks today. BoE and ECB rate decisions headline the European session, while US CPI later on is likely to determine whether recent risk jitters deepen or stabilize.

In FX, much attention centers on EUR/GBP. While the ECB is expected to hold steady with little surprise, the BoE’s rate cut could prove far more influential. The tone of guidance and the voting split will be closely watched for clues on how far easing may extend. The technical backdrop already favors upside in EUR/GBP. Any indication that the BoE’s easing bias is strengthening—especially via reduced hawkish resistance—could quickly propel the cross higher.

Beyond Europe, however, the US CPI release would carry the greatest weight. This comes at a time when risk sentiment is deteriorating, even as markets price in a slightly higher chance of further Fed easing early next year. AI-related valuation concerns remain a persistent overhang, as seen in the sharp selloff in NASDAQ yesterday.

In that context, the danger is not a CPI shock, but what follows once the data risk is removed. With the event out of the way, markets may resume the risk-off behavior already visible beneath the surface.

Currency markets are already reflecting that risk aversion tilt. Kiwi underperforms for the week so far, followed by Aussie and Loonie. Swiss Franc leads, ahead of Dollar and Yen. Euro and Sterling remain caught in the middle.

BoE Tone, Not ECB, Likely to Drive EUR/GBP

BoE and ECB rate decisions dominate the European session today, with EUR/GBP likely to be the key FX mover. Technical signals suggest scope for the cross to retest November’s short-term top, though direction will depend primarily on the BoE outcome rather than the ECB.

The BoE is widely expected to resume policy easing by cutting Bank Rate by 25bps to 3.75%. That move should be seen as a return to form rather than a shift in strategy. The BoE has already been operating on a quarterly cut cadence since mid last year, and today’s move was effectively delayed from November due to the Autumn Budget.

The key questions now are whether the easing cycle continues and how deep it ultimately runs. The answer to the first is likely yes, while the second remains far less clear. Inflation has cooled meaningfully, but it is still above target, leaving policymakers cautious about how far rates can fall.

This week’s weaker-than-expected employment and inflation data may start to soften resistance among more hawkish MPC members. That shift could show up in today’s vote split. Markets will be watching closely for any dissent, and whether a clear majority emerges in favor of the cut.

If the vote shows broad support, expectations for a follow-up cut in February would firm. That would simply mark a return to the quarterly easing rhythm, aligned with the first meeting of the quarter and the release of new economic projections, rather than signaling a more aggressive easing stance.

By contrast, the ECB decision is likely to be a non-event. Policymakers have been clear that rates are comfortable at current levels for the foreseeable future, with inflation anchored close to the 2% target and no immediate risk of deviation.

While speculation has emerged that the ECB’s next move could be a hike, potentially by late 2026, that discussion appears premature. President Christine Lagarde is likely to push back against such talk today.

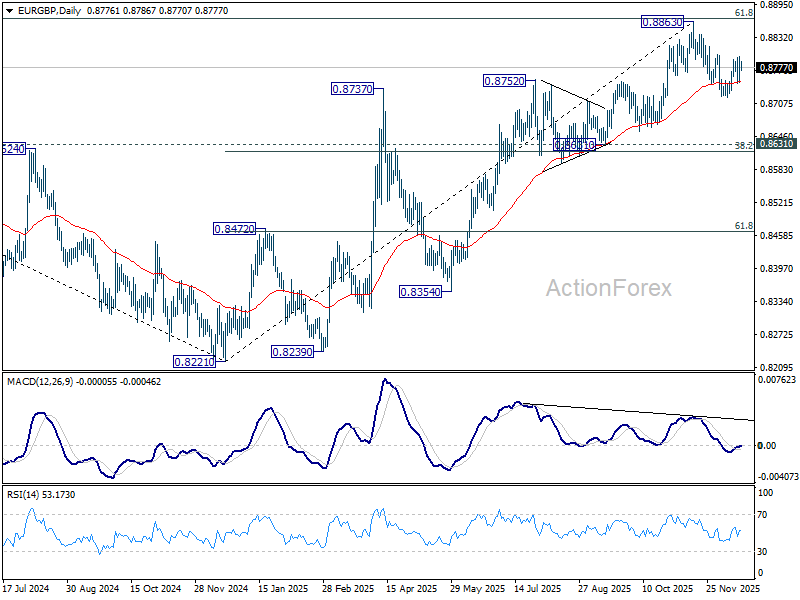

Technically, near term price actions suggests that EUR/GBP’s corrective fall from 0.8863 has completed at 0.8720 after drawing support from 55 D EMA. Firm break of 0.8800 resistance will solidify this bullish case. And more importantly, that would suggest that rise the up trend from 0.8221 is in progress and ready to resume through 0.8863. Though, rejection by 0.8800 will open up another fall through 0.8720 towards 0.8631 support instead.

US CPI in focus as NASDAQ breakdown raises risk-off stakes

Attention in US markets centers on November CPI today, against a backdrop of deteriorating risk sentiment. Despite a slight post-NFP lift in March Fed cut pricing, equities have failed to find support, and risk appetite deteriorated sharply overnight.

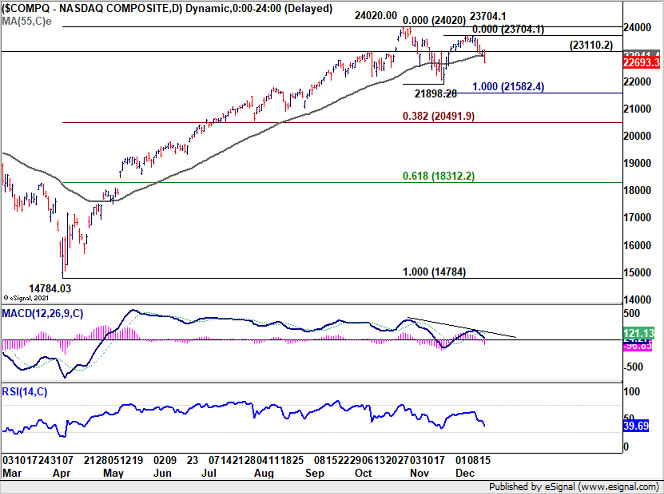

NASDAQ led the downside overnight, breaking decisively below key near-term support and its 55 D EMA. That move shifts the technical picture bearish for the near term and raises the risk of further downside once the CPI event risk passes.

The inflation data itself will be incomplete. The BLS confirmed that the release will omit certain one-month changes due to missing October data after the extended government shutdown. As a result, the CPI print may lack the usual granularity markets rely on for strong directional signals.

Consensus expects headline CPI to tick up to 3.1% yoy, with core CPI holding at 3.0%. Absent a major deviation, Fed expectations should remain broadly stable. A January hold remains the base case, while March cut odds sit near 55%, with three more months of jobs and inflation data still to come.

Technically, NASDAQ’s strong break of 23110.2 support as well as 55 D EMA suggests that corrective pattern from 24020.00 high is now in the third leg. Deeper fall should be seen to 21898.2 support, and possibly below to 100% projection of 24020.0 to 21898.28 from 23704.1 at 21582.4.

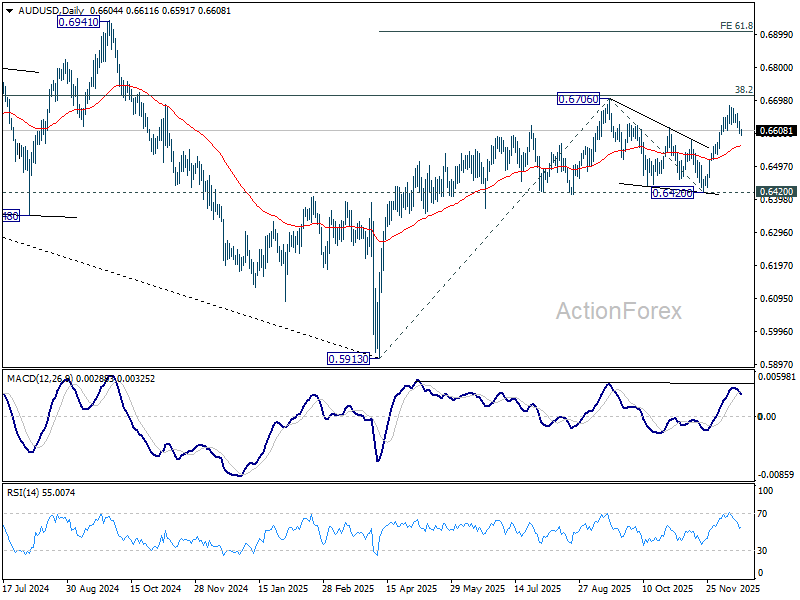

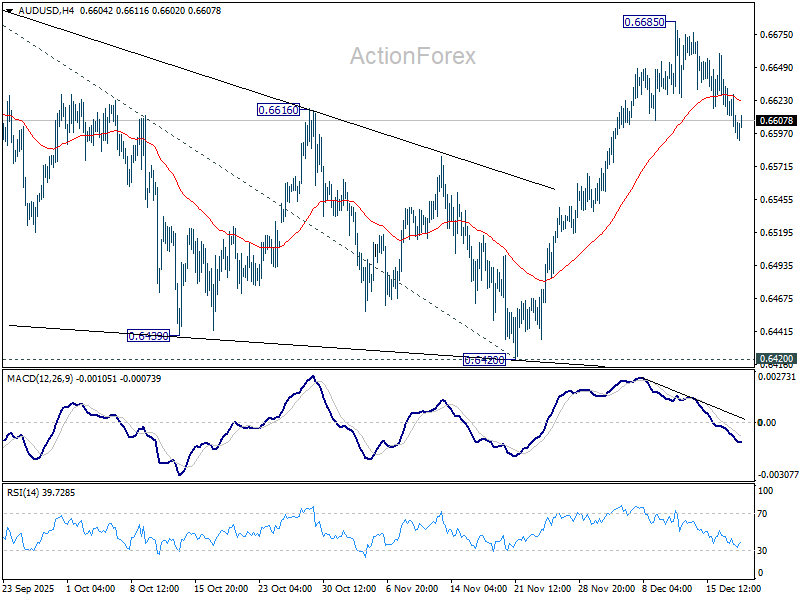

AUD/USD Daily Report

Daily Pivots: (S1) 0.6591; (P) 0.6614; (R1) 0.6628; More...

AUD/USD’s fall from 0.6685 extends lower today. But for now, it’s seen as a near term corrective retreat, and intraday bias remains neutral. On the upside, firm break of 0.6706 will confirm resumption of whole rise from 0.5913. Next target is 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. However, sustained break of 55 D EMA (now at 0.6561) will extend the corrective pattern from 0.6706 with another falling leg, and target 0.6420 support.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.