{kind=link}

Yen selling remains the dominant theme heading into the weekend, with the currency staying as the weakest performer. The renewed slide comes despite the BOJ lifting interest rates to their highest level since 1999. The problem for Yen bulls is not the direction of policy, but the pace. BoJ normalization is widely expected to remain slow and cautious, with policymakers clearly unwilling to risk choking off fragile momentum in growth and wages.

Market consensus has now converged on the view that the next BoJ hike is unlikely to arrive until mid-2026. Even then, policy rates would only move toward the lower bound of the estimated neutral range, roughly between 1.00% and 2.50%. Some investors are already questioning whether the cycle will go any further. There is growing speculation that 1.00% could ultimately mark the terminal rate of the current tightening phase, limiting the scope for sustained Yen appreciation.

While there is theoretical room for rates to move deeper into neutral, that would require tangible evidence of stronger domestic demand. In particular, markets will look for results from Prime Minister Sanae Takaichi’s fiscal stimulus efforts, alongside clear proof that wage growth can be sustained into 2026.

Elsewhere, Dollar trading has steadied after New York Fed President John Williams reinforced skepticism around November’s CPI data. His remarks that the report was likely distorted validated market hesitation to push Dollar lower earlier in the week. As a highly influential Fed voice, Williams’ comments were taken seriously and helped anchor expectations that policy repricing will remain limited in the near term, probably until the December NFP data after holidays.

For the week so far, Kiwi sits at the bottom of the FX performance table, followed by Yen and Aussie. Swiss Franc leads, ahead of Sterling and Dollar, while Euro and Loonie remain positioned in the middle as markets.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.19%. CAC is down -0.06%. UK 10-year yield is up 0.041 at 4.531. Germany 10-year yield is up 0.044 at 2.897. Earlier in Asia, Nikkei rose 1.03%. Hong Kong HSI rose 0.75%. China Shanghai SSE rose 0.36%. Singapore Strait Times fell -0.02%. Japan 10-year JGB yield rose 0.057 to 2.024.

Fed’s Williams flags CPI distortions, plays down urgency to cut again

New York Fed President John Williams said today that November’s inflation data were likely distorted by “technical factors”, cautioning against overinterpreting the downside surprise. He estimated that such distortions may have pushed the CPI reading down by around a tenth of a percentage point.

Williams said it remains difficult to fully assess the size of the impact until December data become available, which should provide a clearer picture of how much the technical effects influenced November’s figures.

On policy, Williams struck a measured tone, saying he does not feel a “sense of urgency” to lower interest rates further. He argued that the cuts already delivered have positioned the Fed well to continue easing inflation pressures while also supporting a labor market that is cooling in an orderly fashion.

Canada retail sales fall -0.2% mom in October, November rebound eyed

Canada’s retail sales edged down by -0.2% mom to CAD 69.4B in October, extending signs of soft consumer demand. Sales declined in four of nine subsectors, led by weakness at food and beverage retailers, pointing to ongoing pressure on discretionary spending.

Underlying momentum was weaker than the headline suggested. Core retail sales, excluding autos and gasoline, fell -0.5% mom. Sales volumes declined -0.6% mom.

Statistics Canada’s advance estimate points to a 1.2% mom rebound in November. While the estimate is based on a lower-than-usual response rate of 60%, it hints at a potential stabilization in consumption as financial conditions ease, though confirmation will depend on the final data.

BoJ raises rates to 0.75%, keeps tightening bias intact

The BoJ raised its policy rate by 25bps to 0.75%, as widely expected, marking another step in its gradual normalization process. Despite the hike, the BoJ emphasized that financial conditions remain highly accommodative, with real interest rates still “significantly negative.”

In its statement, the BoJ reaffirmed a tightening bias. If the outlook laid out in the October 2025 Outlook Report is realized, the Bank said it will “continue to raise the policy interest rate”. Policymakers also expressed increased confidence that the likelihood of realizing the outlook “has been rising”.

At the post-meeting press conference, Governor Kazuo Ueda stressed future adjustments will depend on incoming data on economic, price, and financial conditions, with policy decisions reassessed at every meeting rather than following a preset path.

On the neutral rate, Ueda acknowledged substantial uncertainty. He described the estimate as sitting within a wide range and said they would assess how the economy and prices respond to each rate move. “We will seek to produce new estimates on Japan’s neutral rate, if needed, though I don’t think that will help us narrow the range that much,” he added.

NZ trade deficit narrows to ND -163m on 9.2% yoy exports surge

New Zealand’s trade balance surprised to the upside in November, with the deficit narrowing sharply to NZD -163m, far smaller than expectations for a shortfall of around NZD -1.2B. The improvement was driven by a solid pickup in exports, which rose 9.2% yoy, or NZD 588m, to NZD 7.0B.

Export performance was mixed by destination. Shipments to Australia surged by 31% yoy, while exports to the EU also rose strongly by 51% yoy. By contrast, exports to China slipped modestly by -0.7%yoy, while shipments to the US fell sharply by -17% yoy, and Japan by -1.9% yoy.

Imports rose at a more moderate pace of 4.4% yoy to NZD 7.2B. Gains were led by stronger inflows from the US (36% yoy), EU (17% yoy) and South Korea (20% yoy). Imports from China rose a modest 1.7% yoy. Imports from Australia declined (-7.7% yoy).

NZ ANZ business confidence hits 30-year high as cyclical recovery gathers pace

New Zealand business confidence surged in December, with the ANZ headline index jumping from 67.1 to 73.6. Firms’ own activity outlook rose sharply from 53.1 to 60.9. Both readings are the strongest in 30 years, pointing to a broad-based improvement in sentiment as the economic cycle turns.

Inflation indicators ticked up modestly but remain contained. The share of firms expecting to raise prices in the next three months rose one point to 52%, while those anticipating cost increases climbed two points to 76%. Inflation expectations, however, were unchanged at 2.69%, suggesting confidence is improving without triggering a renewed inflation scare.

ANZ said “things are clearly looking up,” noting that the earlier slowdown was deliberately engineered by tight monetary policy. With that restraint easing, interest rates and the exchange rate both well below their peaks, and the RBNZ signaling no intention to hike rates any time soon, cyclical forces appear firmly supportive of recovery.

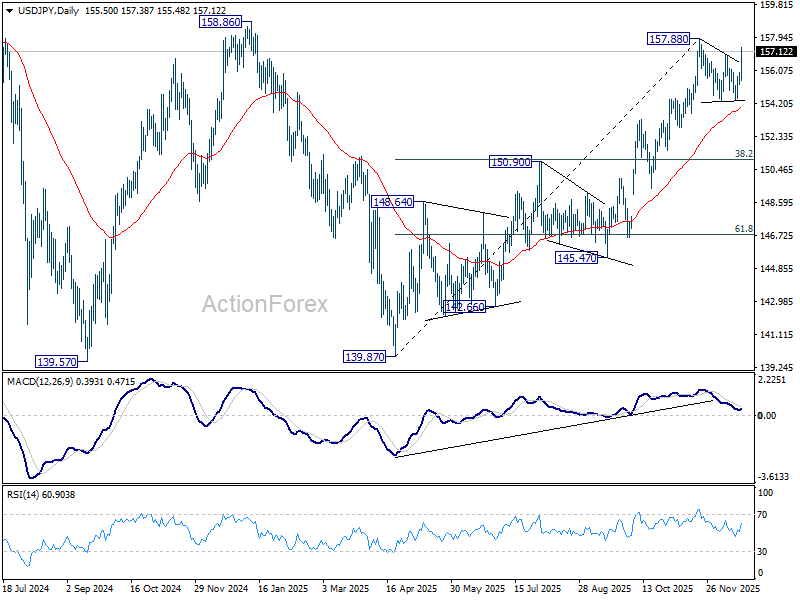

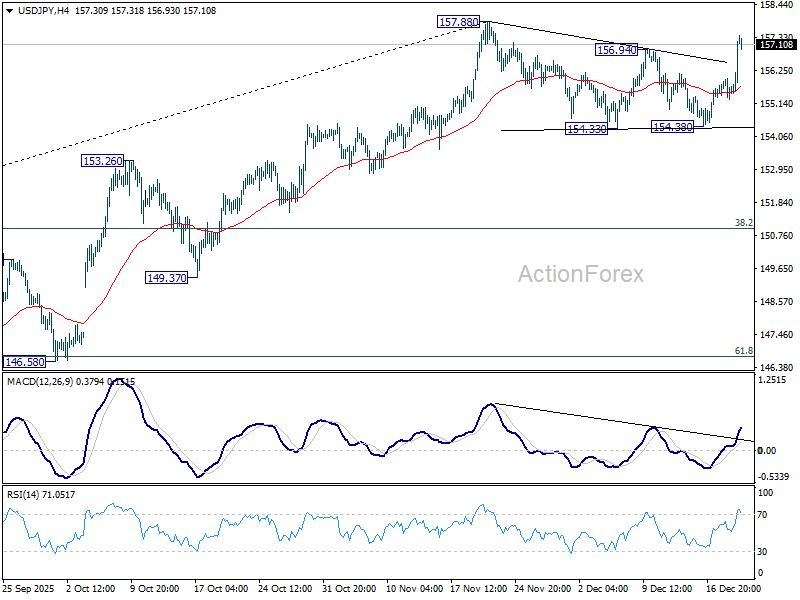

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.23; (P) 155.61; (R1) 155.93; More…

USD/JPY’s rally continues today and the break of 156.94 solidify that case that corrective pattern from 157.88 has completed with three waves to 154.38. That is, rally form 139.87 is ready to resume. Intraday bias is back to the upside for 157.88 and above. Firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 158.85 high. Risk will now stay on the upside as long as 154.38 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.