{kind=link}

Markets remain stuck in a year-end lull on the final trading day of the year, with liquidity thin and participation limited. Price action across asset classes reflects consolidation rather than conviction, as investors opt to close the year defensively rather than chase late moves.

Stronger-than-expected China PMI data failed to lift sentiment. While the readings suggested momentum was building toward year-end, markets largely looked past the improvement, treating it as insufficient to alter the broader outlook. Skepticism remains rooted in structural concerns. Analysts continue to flag China’s persistent investment slump, excess capacity, and weak domestic consumption as constraints that are likely to linger well into 2026, capping the scope for a durable rebound.

In FX markets, Dollar is trading modestly firmer after the release of December FOMC minutes. Even so, the move appears corrective in nature. Selling interest in Dollar is more likely to re-emerge once markets return from the New Year holidays. For now, gains look more like short-covering than a shift in underlying sentiment.

Minutes from the December meeting of the Fed confirmed the depth of the internal divide that led to a 25bp cut decided by a three-way vote. Policymakers broadly agreed that further easing could be appropriate if inflation continues to cool. At the same time, the minutes revealed clear hesitation about how aggressively policy should be adjusted. Several participants argued that rates may need to remain unchanged for some time after the December cut, with some describing the easing decision as “finely balanced”.

Those favoring a hold expressed concern that progress toward the 2% inflation objective may have “stalled” in 2025, emphasizing the need for greater confidence before endorsing further cuts. That caution helped keep expectations anchored. Market pricing was little changed in response. A January hold remains priced above 80%, while odds of a March cut continue to hover around 50%.

In FX performance, Yen leads the week, followed by Dollar and Loonie. Kiwi lags ahead of Swiss Franc and Aussie. Euro and Sterling sit in the middle.

Happy New Year to our readers, Action Insight will be back on Monday, January 5, 2026.

China PMIs return to expansion as year-end demand lifts activity

China’s official PMIs delivered a clear upside surprise in December, signaling a return to expansion for the first time since March. PMI Manufacturing rose from 49.2 to 50.1, beating expectations of 49.4, while PMI Non-Manufacturing climbed from 49.5 to 50.2, also above forecast. The improvement was broad enough to lift PMI Composite from 49.7 to 50.7, pointing to renewed momentum across both goods and services activity.

According to National Bureau of Statistics of China, the rebound marks a notable stabilization heading into year-end. Large enterprises were the primary driver of the pickup, as PMI jumped to 50.8, up 1.5 points from November, reflecting stronger capacity utilization and firmer order flows. In contrast, activity among smaller firms remained under pressure, with medium-sized enterprises edging up to 49.8 and small firms slipping further to 48.6.

NBS chief statistician Huo Lihui said new orders rose meaningfully in December, describing a significant expansion in both production and demand. He also pointed to improving confidence tied to pre-holiday stockpiling ahead of the Lunar New Year in February, particularly in agriculture, food processing, and beverage sectors.

Private-sector data echoed the official improvement. RatingDog PMI Manufacturing rose from 49.9 to 50.1, also beating expectations. RatingDog founder Yao Yu said new orders have now grown for seven consecutive months, supported by domestic product launches and business expansion.

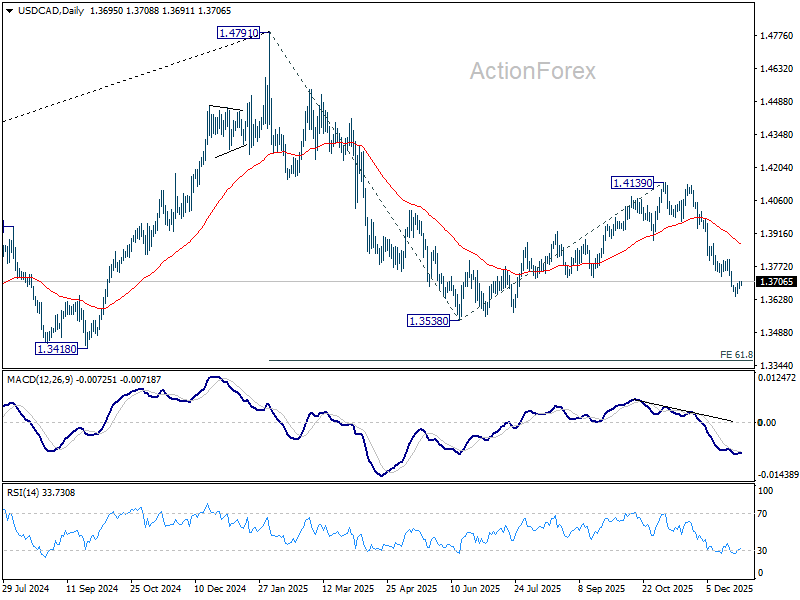

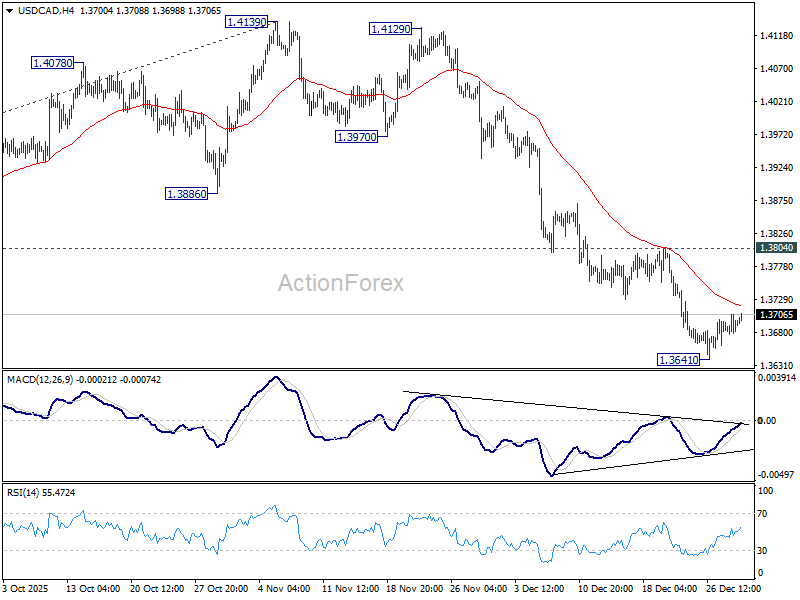

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3682; (P) 1.3695; (R1) 1.3712; More…

USD/CAD’s recovery from 1.3641 extends slightly higher today, but stays well below 1.3804 resistance. Intraday bias remains neutral and further decline is expected. On the downside, break of 1.3641 will resume the fall from 1.4139 to retest 1.3538 low. Firm break there will extend the whole decline from 1.4791 to 1.3365 projection level.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it’s just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.