{kind=link}

Dollar is trading broadly higher in Asian session today, and remains the strongest performer of the week, as markets head into the December US non-farm payrolls report. Within FX, USD/JPY stands out as a pair to watch, with the pair edging closer to levels that would confirm an upside break.

This week’s price action suggests markets may be positioning for upside risk in the jobs data, rather than bracing for disappointment. That bias is understandable. That narrative is supported by this week’s indicators, which collectively point to a jobs market that remains resilient. Hiring may be subdued, but layoffs remain contained, reinforcing the view that the US economy is slowing only gradually.

The backdrop points to resilience rather than fragility, setting the stage for a payrolls print that could surprise modestly to the upside. Such an outcome would reinforce a wait-and-see stance at the Fed. Markets may continue to debate the timing of the next rate cut, but a decisive shift toward March easing would look premature.

Still, the sustainability of Dollar’s rally hinges on more than the headline payrolls number. Market reactions across equities and Treasury yields will be critical in determining whether USD gains can extend or begin to fade after the event.

Beyond data, legal risk is also on the radar. Markets are bracing for a ruling from the US Supreme Court on the legality of President Donald Trump’s global tariffs imposed under the International Emergency Economic Powers Act. A decision could arrive as early as today. Expectations that the court may strike down the tariffs have grown since November arguments, when justices across the ideological spectrum questioned whether the law grants such sweeping authority. A ruling against the administration could trigger refund claims estimated at up to US 150B, with implications for Treasury issuance and market volatility.

Trade tensions are also resurfacing elsewhere. US–India negotiations are stalled after talks collapsed last year, prompting Trump to double tariffs on Indian goods to 50% in August. US officials have since suggested the breakdown stemmed from a lack of direct engagement from Indian leadership. According to Commerce Secretary Howard Lutnick, the deal was effectively ready but required a direct call from Prime Minister Narendra Modi to close it — a step that never materialized.

On weekly FX performance, Dollar leads, followed by Aussie and Sterling. Loonie lags, ahead of Swiss Franc and Euro. Yen and Kiwi trade in the middle.

NFP Preview: DOW 50k and yield 4.2% decide Dollar path

Dollar has taken the driving seat in FX markets this week, supported by firmer US data and a modest repricing of Fed expectations. Bets on a March rate cut have dipped to around 41%, following the upside surprise in ISM Services earlier in the week, which reinforced the view that US economic momentum remains intact. Nevertheless, hat strength now faces a critical test from Friday’s December non-farm payrolls report. How markets respond across equities, Treasuries and rate pricing will be key in determining whether the Dollar can extend its gains.

Consensus expectations point to a 66k increase in payrolls, broadly in line with November’s 64k gain. Earnings are seen rising 0.3% mom, while the unemployment rate is expected to edge lower to 4.5%. Such an outcome would reinforce the prevailing “low hiring, low firing” narrative.

However, several leading indicators suggest upside risk to the headline payroll number. The ISM Services employment index jumped back from 48.9 into expansion at 52.0, while the Manufacturing employment sub-index also improved from 44.9 to 44.0. The ADP report showed a rebound to 41k jobs from November’s negative print. Four-week moving average of initial jobless claims fell to 212k, its lowest level in months. Together, the data point to resilience rather than deterioration.

Market reaction, however, is unlikely to be straightforward. Strong payrolls could be interpreted positively, reinforcing confidence in a soft-landing scenario. Equally, they could be seen as reducing the scope for aggressive easing, triggering a risk-off response that ultimately supports Dollar. The most bullish outcome for the greenback, ideally, would involve equity markets rolling over alongside a sustained rise in Treasury yields.

Technically, DOW is facing a key inflection zone, with 50,000 marking both a psychological level and the upper boundary of a medium-term channel. A break below 47,853 support would suggest a correction is already underway, opening the door to a deeper pullback toward 45,728. Conversely, decisive push above 50,000 could accelerate gains toward 52,179, potentially within January. That, if realized, would be bearish for the greenback.

Meanwhile, 10-year yield continues to find support at its 55 D EMA (now at 4.131). Yet, upside is capped by 4.200 cluster resistance (38.2% retracement of 4.629 to 3.9047 at 4.207). On the upside, clean break above the 4.200 key level resistance cluster would argue that whole fall from 4.629 has already completed 3.947. That would set up stronger rise to 61.8% retracement at 4.368, and take Dollar higher.

China CPI surprises to upside at 0.8%, but full-year picture weak

China’s consumer inflation accelerated in December, with CPI rising from 0.7% to 0.8% yoy, above expectations of 0.6% and marking a 34-month high. The increase was driven mainly by food prices, as fresh vegetables surged 18.2% and beef prices rose 6.9%, supported by pre-New Year holiday demand.

However, price pressures remained uneven. Pork prices continued to fall sharply, down -14.6% yoy, while prices of gold jewelry jumped 68.5%, reflecting strong investment and gifting demand rather than broad-based consumption. According to National Bureau of Statistics, holiday shopping and supportive policies helped lift prices, but the improvement remains selective.

Looking beyond December, the broader deflationary challenge persists. Full-year CPI growth in 2025 was flat, the weakest in 16 years and well below policymakers’ “around 2%” target.

At the producer level, deflation moderated only slightly. PPI improved to -1.9% yoy in December from -2.2%, aided by rising non-ferrous metal prices and capacity discipline in key industries. Still, PPI fell 2.6% for the full year.

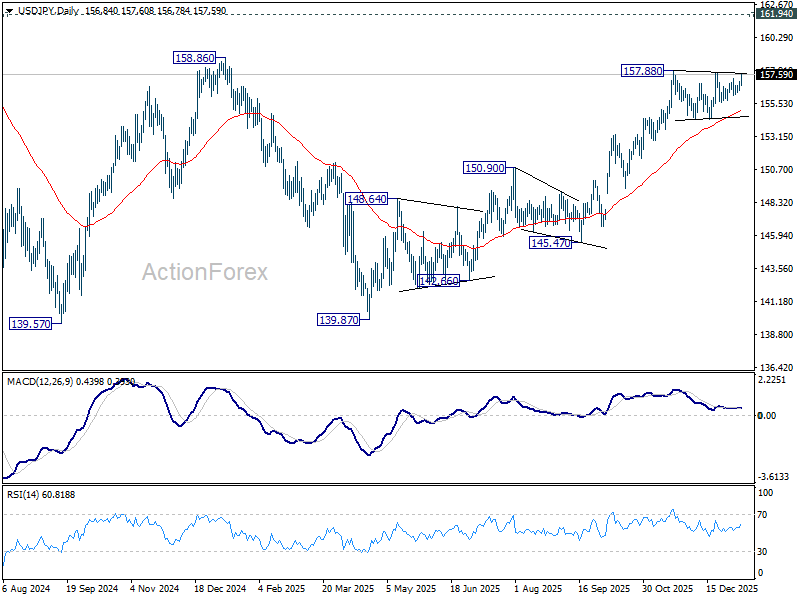

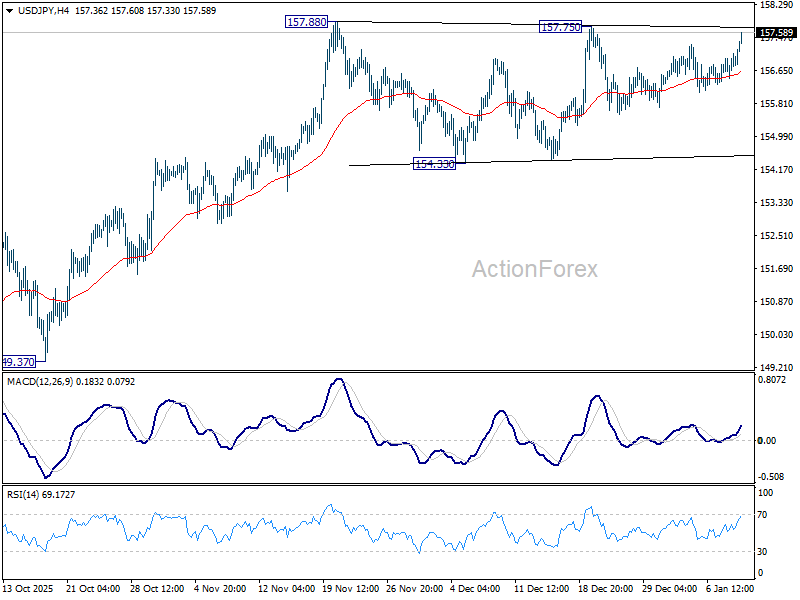

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.54; (P) 156.80; (R1) 157.15; More…

Intraday bias in USD/JPY stays neutral, but immediate focus is now on 157.88 resistance with today’s rally. Decisive break there will extend the up trend from 138.98. Further break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 161.94 high. In any case, outlook will continue to stay bullish as long as 154.33 support holds.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.33 support will dampen this bullish view and extend the corrective range pattern with another falling leg.