{kind=link}

Yen came under renewed and intense pressure during Asian session, as domestic equities surged more than 3% to new record highs following the market reopening. The catalyst behind the equity rally — and Yen’s decline — remains growing conviction that Japanese Prime Minister Sanae Takaichi is preparing to call a snap general election in February. That expectation has extended the so-called “Takaichi trade” that began last year after she became Japan’s first female Prime Minister.

The trade rests on a familiar set of assumptions. Early elections are expected to deliver a stronger mandate for fiscal expansion, driving equity gains, pushing bond prices lower, and weakening Yen. Takaichi’s strong public support has reinforced expectations that the ruling bloc would emerge with enhanced authority. Speculation has now converged on a relatively narrow window. Parliament dissolution is tentatively expected around January 23, with election dates mostly cited as February 8 or February 15, according to Japanese media and market chatter.

Regarding the selloff in Yen, Japanese authorities have responded with verbal warnings, but the market response has been dismissive. Traders appear unconvinced that rhetoric alone will halt a move driven by political conviction and global risk appetite. Finance Minister Satsuki Katayama said she raised concerns about Yen’s one-sided depreciation in talks with US Treasury Secretary Scott Bessent. Her comments were interpreted as hinting at possible US tolerance for intervention, though no concrete policy signals followed. Separately, Deputy Chief Cabinet Secretary Masanao Ozaki warned that authorities stood ready to act against excessive currency moves, including speculative ones. For now, markets continue to test those limits.

Elsewhere, US tariff headlines also crossed the wires. President Donald Trump warned that any country doing business with Iran would face an immediate 25% tariff on all trade with the US, declaring the measure “final and conclusive.” He added that the tariffs are “effectively immediately” even though details remain scarce for now.

In currency markets, Yen remains the clear underperformer for the week so far. Dollar follows as the second-weakest, weighed down not by data but by lingering concerns over Fed independence and US institutional credibility. Euro has also softened modestly, though losses remain contained. On the other side of the ledger, Kiwi is the strongest performer, supported by upbeat domestic business confidence data. Sterling and Swiss Franc are also holding firm. Aussie and Loonie sit broadly in the middle.

Attention now turns to US December CPI later today, though expectations for a market-moving surprise appear limited. Traders have already pared back bets on a March rate cut, with probabilities sitting below 30% following a run of mixed but resilient US data. There is little urgency for the Fed to act, and inflation would need to surprise decisively in either direction to alter that view.

More importantly, CPI is competing with far louder narratives. Political risk, tariff uncertainty, and questions around Fed independence are commanding investor attention. In that context, even a firm inflation print may prove secondary unless it materially shifts the broader policy outlook.

In Asia, Nikkei rose 3.10%. Hong Kong HSI is up 0.70%. China Shanghai SSE fell -0.64%. Singapore Strait Times rose 0.73%. Japan 10-year JGB yield rose 0.075 to 2.172. Overnight, DOW rose 0.17%. S&P 500 rose 0.16%. NASDAQ rose 0.26%. 10-year yield rose 0.016 to 4.187.

Australia Westpac consumer sentiment deteriorates, RBA won’t tighten precipitously

Australian consumer sentiment weakened further at the start of the year, highlighting growing anxiety over the interest-rate outlook. The Westpac Consumer Sentiment Index fell -1.7% mom to 92.9 in January, pushing sentiment deeper into pessimistic territory.

Westpac pointed to a sharp shift in rate expectations as the main drag. Nearly two-thirds of consumers who expressed a view now expect mortgage rates to rise over the next 12 months, more than double the share seen back in September.

For policy, Westpac expects the RBA to stay on hold when it meets on February 2–3, and through the remainder of 2026. While the RBA has flagged readiness to tighten if inflation proves stubborn, softer labor market conditions and limited price pressures across many goods and services should allow inflation to drift back into the 2–3% target range without the need to “tighten precipitously.”

NZIER confidence hits 10-year high, RBNZ to hold until H2 hike

New Zealand business confidence surged in Q4, reinforcing signs that an economic recovery is starting to form. The New Zealand Institute of Economic Research (NZIER) said a net 39% of firms expect better general economic conditions in the months ahead, a sharp rise from 17% in the September quarter and the strongest reading since March 2014.

NZIER noted that while a gap remains between headline confidence and firms’ own domestic trading activity, the direction of travel is clearly improving. The survey suggests the impact of earlier interest-rate cuts is now filtering through the broader economy, lifting sentiment even as activity indicators lag.

Inflation signals was reassuring. Cost and pricing indicators point to broadly contained pressures in the December quarter, with cost pressures easing and a net 37% of firms reporting higher costs.

With demand recovering but inflation subdued, NZIER expects no further OCR cuts this cycle, forecasting the RBNZ’s Official Cash Rate to trough at 2.25% before hikes begin in the second half of 2026.

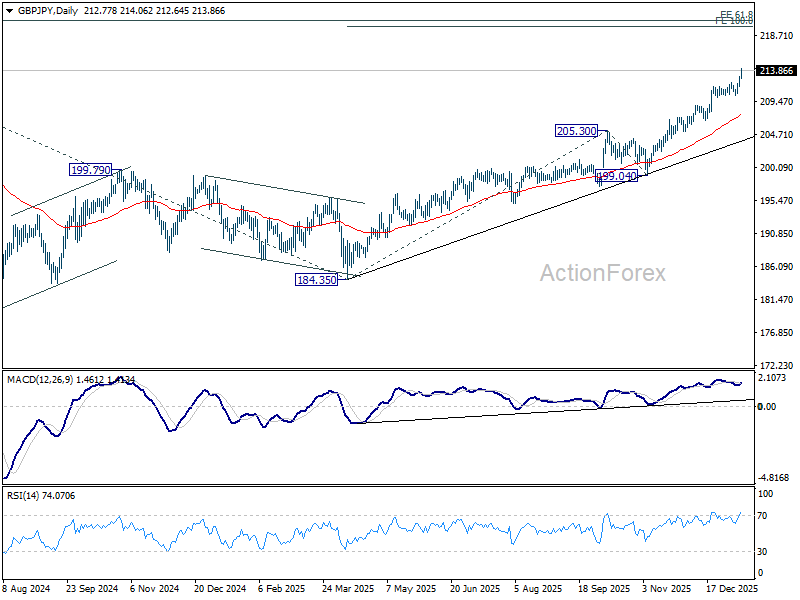

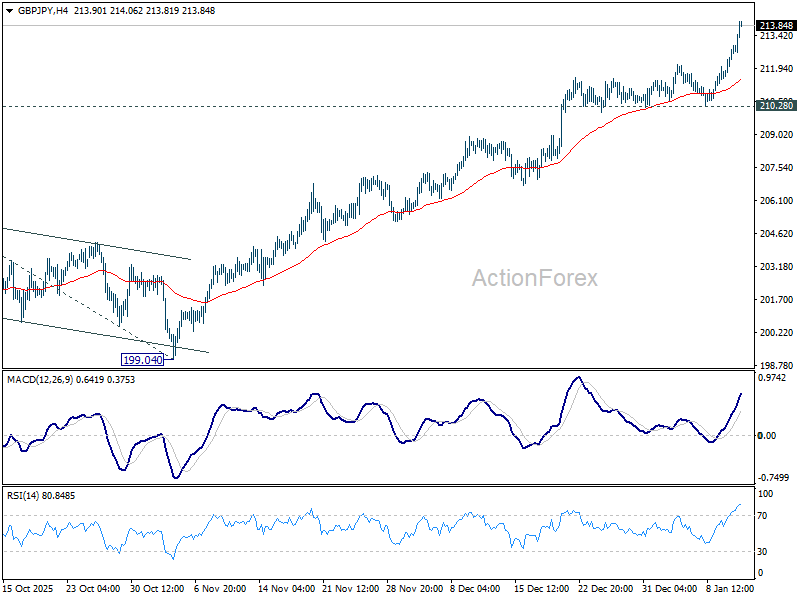

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.07; (P) 212.55; (R1) 213.47; More…

GBP/JPY’s rally accelerates higher today and intraday bias on the upside. Current up trend should now target 100% projection of 184.35 to 205.30 from 199.04 at 219.99 next. For now, outlook will stay bullish as long as 210.28 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.