Dollar edged modestly higher in early US session, but the move lacked conviction as investors digested February CPI data that broadly matched expectations. Although the annual core rate remains somewhat elevated around 2.5%, the key takeaway is that inflation is not reaccelerating. That provides the Fed with breathing room to observe how the Iran war and the resulting oil shock feed into broader price dynamics.

For policymakers, the immediate concern is not the current inflation level but the possibility of “second-round effects.” A sustained surge in energy costs could eventually push up transportation prices, services inflation, and wage demands. February’s data, however, does not yet show those pressures emerging before the war.

As a result, there is little urgency for the Fed to respond aggressively. A rate hold at the March meeting is already fully priced by markets, and today’s CPI report reinforces the central bank’s ability to remain in a wait-and-see mode while assessing how the geopolitical shock evolves.

The debate instead centers on when the Fed might resume its easing cycle. Markets now see June and September as the key windows for rate cuts this year, though the probability of a mid-year move remains uncertain given the volatile global backdrop.

Energy markets remain the dominant macro driver. Officials from the International Energy Agency and the G7 are now finalizing plans for what could become the largest coordinated emergency oil reserve release in history. The proposal reportedly involves releasing between 300 and 400 million barrels.

Such an intervention would dwarf the 182-million-barrel release implemented following Russia’s invasion of Ukraine in 2022. The scale of the plan highlights the severity of supply concerns after the Iran war effectively disrupted shipping through the Strait of Hormuz.

In currency markets, Yen and Swiss Franc are the weakest performers so far this week, along with Euro, as investors rotate out of defensive positions. Commodity and risk-sensitive currencies have benefited from the shift. Aussie leads the performance table as markets increasingly bet the RBA may bring forward another rate hike this month. Kiwi follows closely, while Sterling also gains support from improving risk sentiment. Dollar and Loonie remain in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.86%. DAX is down -1.57%. CAC is down -0.97%. UK 10-year yield is up 0.121 at 4.619. Germany 10-year yield is up 0.081 at 2.921. Earlier in Asia, Nikkei rose 1.43%. Hong Kong HSI fell -0.24%. China Shanghai SSE rose 0.25%. Singapore Strait Times rose 0.07%. Japan 10-year JGB yield fell -0.02 to 2.166.

US CPI steady at 2.4% in February, core unchanged at 2.5

US inflation rose slightly faster than expected in February, though the broader price trend remained stable. Headline CPI increased 0.3% mom, above the expected 0.2% rise, while core CPI—which excludes food and energy—rose 0.2% on the month, matching market expectations.

Housing costs continued to play the largest role in the monthly increase. The shelter index rose 0.2% mom and was the biggest contributor to the overall CPI gain. Food prices also moved higher, climbing 0.4% on the month, while the energy index increased 0.6%.

On an annual basis, inflation remained unchanged. Headline CPI held steady at 2.4% year-on-year while core CPI remained at 2.0%, both in line with expectations. Over the past year, the energy index rose 0.5% while food prices increased 3.1%.

Japan import costs surge on weak Yen, fastest since July 2024

Japan’s producer inflation moderated in February, offering some relief on the domestic cost front even as import prices surged. Producer Price Index rose 2.0% yoy, slowing from January’s 2.3% pace and coming in slightly below market expectations of 2.1%.

The softer PPI reading suggests upstream price pressures in Japan’s domestic production sector may be easing slightly. However, the picture is less benign when looking at import costs, which are heavily influenced by Yen’s weakness.

Japan’s yen-based import price index jumped 2.8% yoy, accelerating sharply from a revised 0.7% increase in January and marking the fastest rise since July 2024. The data highlights how the weak Yen continues to push up import costs, a dynamic that could keep underlying inflation pressures elevated despite the moderation in producer prices.

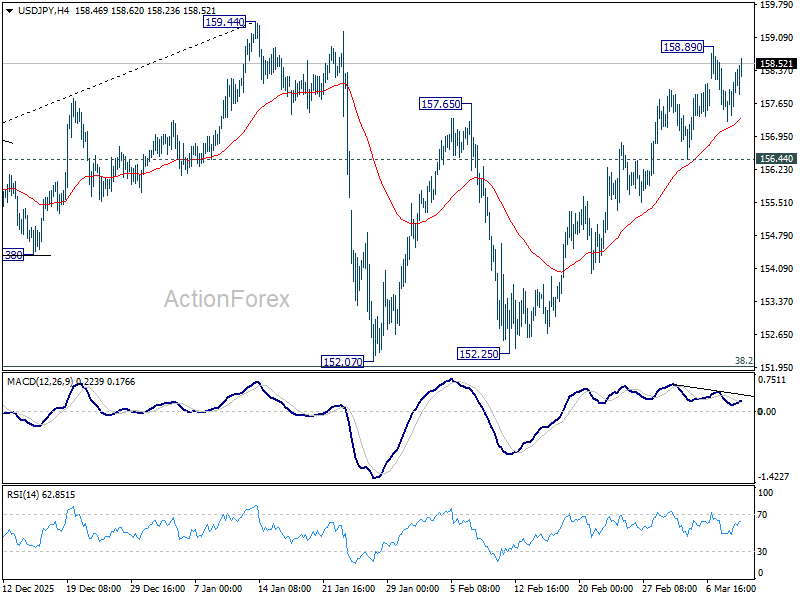

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.44; (P) 157.84; (R1) 158.44; More…

USD/JPY strengthens mildly in early US session but stays below 158.98 temporary top. Intraday bias remains neutral for the moment. On the upside, above 158.89 will extend the rise from 152.07 to 159.44 resistance. Decisive break there will target 161.94 high next. However, considering bearish divergence condition in 4H MACD, firm break of 156.44 support will argue that the rebound has completed, and turn bias back to the downside for 152.07 support. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

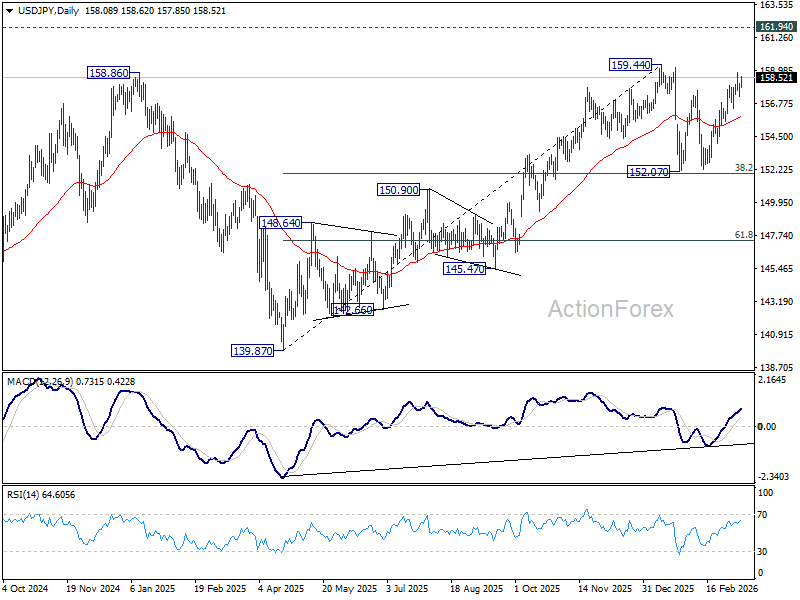

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

{kind=link}