Risk-off sentiment has returned to the fore as the US session approaches, with Dollar breaking out against Yen and Swiss Franc while Brent crude rebounds to $108. While US President Donald Trump has extended the Iran strike pause to April 6, markets are increasingly viewing this as a “thin veil” for a tactical realignment rather than true de-escalation.

A key concern is that the “pause” does not cover several major escalation channels. Traders are actively positioning for a high-risk weekend characterized by “Wildcard” threats—specifically unilateral Israeli strikes and Trump’s own “Pearl Harbor” obsession with surprise. This front-running suggests a growing belief that the diplomatic window could be scrapped well before the Monday open.

The most immediate risk comes from Israel, which is not bound by the US framework and has signaled intentions to escalate operations. Any strike that impacts high-value infrastructure or strategic assets could quickly invalidate the pause and trigger retaliation from Iran.

Beyond that, the buildup of US ground capabilities suggests a broader strategic shift. Markets are increasingly considering scenarios where the US could move to secure key chokepoints such as the Strait of Hormuz or seize strategic islands if diplomacy fails. While these actions may not occur immediately, the preparation itself raises the probability of a larger conflict.

At the same time, Iran’s response function is evolving. As pressure intensifies, the risk is shifting from controlled proxy actions to more direct and asymmetric strikes, including potential attacks on US military assets in the region. Such a move would likely trigger a rapid escalation, bypassing the current pause framework entirely.

Regional spillover risks are also rising. Interceptions of drones over Saudi Arabia and the UAE, along with warnings issued by Iranian forces, point to an increasingly fragile environment where miscalculations could draw additional players into the conflict. A single incident involving a neutral or regional actor could quickly broaden the scope of the war.

Adding to the uncertainty is the risk tied to strategic unpredictability. Trump’s recent comparisons of his strategy to “the element of surprise” at Pearl Harbor signal that he views diplomatic pauses as tools to keep an enemy off-balance. The risk is that the administration, sensing Iranian stalling, could unilaterally scrap the April 6 deadline this weekend to order a “shock and awe” strike on Iran’s power grid. While a tail-risk, it is something that the markets wouldn’t ignore.

In currency markets, Dollar is the strongest performer for the week so far, followed by Sterling and Yen. In contrast, growth-sensitive currencies such as the Australian and New Zealand Dollars remain under pressure, while Euro and Canadian Dollar sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.44%. DAX is down -1.43%. CAC is down -0.80%. UK 10-year yield is up 0.103 at 5.019. Germany 10-year yield is up 0.038 at 3.114. Earlier in Asia, Nikkei fell -0.43%. Hong Kong HSI rose 0.38%. China Shanghai SSE rose 0.63%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield rose 0.106 to 2.380.

UK Retail Sales Slip -0.4% as Discount-Driven Demand Fades

UK retail sales slipped -0.4% in February after a strong January, as earlier discount-driven demand faded. Spending appears to have been pulled forward, leaving softer activity in the latest data. While three-month growth remains positive, the figures highlight uneven consumer momentum and sensitivity to pricing. Read More

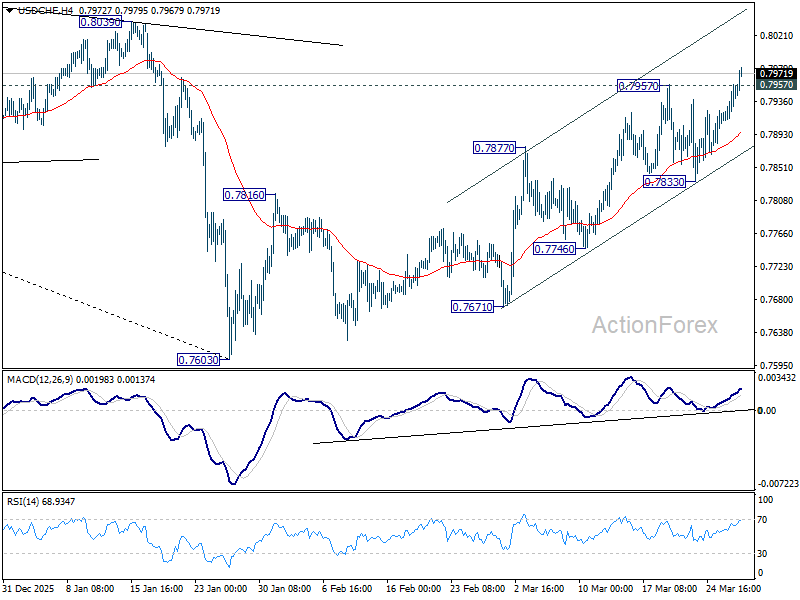

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7924; (P) 0.7942; (R1) 0.7972; More….

USD/CHF’s break of 0.7957 suggests that rebound from 0.7603 is resuming. Intraday bias is now the upside. As a correction to the whole down trend from 0.9200, next target is 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rise is expected as long as 0.7833 support holds, in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

{kind=link}