Dollar strengthened broadly as markets reacted to a sharp escalation in rhetoric from U.S. President Donald Trump, who warned that Iran’s key energy infrastructure could be “completely obliterated” if the Strait of Hormuz is not reopened and a peace deal is not reached “shortly.” In particular, Trump explicitly named Kharg Island—along with Iran’s electric generating plants, oil wells, and desalination facilities—as targets, signaling a shift from targeted strikes toward comprehensive economic disruption.

Kharg Island is central to Iran’s oil exports, handling the vast majority of its crude shipments. Targeting it would effectively remove a significant share of Iranian supply from global markets, intensifying concerns over supply disruption. This explicit threat has heightened fears of a direct hit to global energy flows, reinforcing demand for the Dollar through both safe-haven and energy-linked channels.

The tone of Trump’s comments also suggests a shift in strategy. His reference to a possible extended “stay” in Iran implies more than short-term strikes, raising the prospect of a sustained presence aimed at controlling or disabling key energy hubs. Reports that the Pentagon is preparing to deploy additional ground troops further support the view that markets must now price in a longer-duration conflict.

Meanwhile Yen strengthened as Japanese authorities intensified verbal intervention following USD/JPY’s move toward the 160 threshold. The Ministry of Finance issued what markets interpret as a “final warning,” signaling readiness to act against excessive currency moves “soon”. The rebound was further supported by expectations that BoJ policy normalization may come sooner than previously anticipated, after Governor Kazuo’s Ueda comment at the parliament.

However, Yen gains remain constrained by the broader strength of the Dollar. Rather than triggering a reversal in USD/JPY, intervention rhetoric is acting as a cap on further upside. As a result, Yen strength is being expressed more clearly in crosses.

Elsewhere, expectations for further tightening are building. Economists are increasingly calling for a more aggressive response from the Reserve Bank of Australia, with forecasts now pointing to consecutive rate hikes in May, June, and August. This reflects growing concern over second-round inflation effects, as higher energy costs are feeding through to wages and services, pushing the RBA from a monitoring stance toward a more proactive tightening phase.

In Europe, markets are also shifting toward a more hawkish outlook for the ECB. Rate hike expectations have firmed, with investors pricing three increases this year, potentially beginning as early as April or June. Policymakers are seen as moving earlier in the cycle, in part to avoid a repeat of the delayed response seen during the previous inflation surge. The overall tone remains cautious, shaped by escalating geopolitical risks and shifting policy expectations.

In currency markets, Yen is the strongest performer so far, followed by Dollar and Swiss Franc, while risk-sensitive currencies such as Aussie and Kiwi remain under pressure.

Gold Rebound From 4100 Suggests “Wyckoff Accumulation,” With Two Key Tests Ahead

Gold’s rebound from 4100 is raising the possibility of a Wyckoff accumulation phase, following a potential selling climax and liquidity flush. However, confirmation still depends on two key tests: a successful secondary test above 4100 and a breakout through the 4600–4800 resistance zone. Until then, the structure remains a developing range rather than a confirmed reversal. Read More.

Japan Issues Intervention “Final Warning” as USD/JPY Breaks 160, but Dollar Strength Prevents Reversal

Japan escalated intervention rhetoric after USD/JPY broke above 160, issuing what markets see as a “final warning.” However, strong Dollar momentum continues to limit the impact, turning intervention into a ceiling rather than a reversal trigger. Yen strength is instead showing more clearly in crosses such as AUD/JPY, where downside has extended. Read More.

BoJ Warns of “Behind the Curve” Risk as Yen Depreciation Amplifies Inflation Pressure

BoJ flagged the risk of falling “behind the curve” as yen depreciation amplifies inflation pressure and raises concerns over second-round effects. Policymakers signaled readiness to accelerate rate hikes if needed, especially if wage growth and cost pass-through persist. The shift highlights growing sensitivity to currency-driven inflation and strengthens the tightening bias. Read More.

Eurozone Sentiment Weakens Further as ESI Falls to 96.6

Economic sentiment in the EU and euro area weakened again in March, driven by sharp declines in consumer and retail confidence. Employment expectations also softened, signaling weaker demand and cautious hiring outlook. Growth momentum appears to be fading. Read More

Swiss KOF Barometer Drops Sharply to 96.1, Signals Broad-Based Economic Weakness

Switzerland’s KOF Economic Barometer dropped sharply to 96.1 in March, missing expectations and signaling a broad slowdown. Weakness across manufacturing, exports, and foreign demand highlights growing external headwinds. The data point to softer growth momentum ahead. Read More

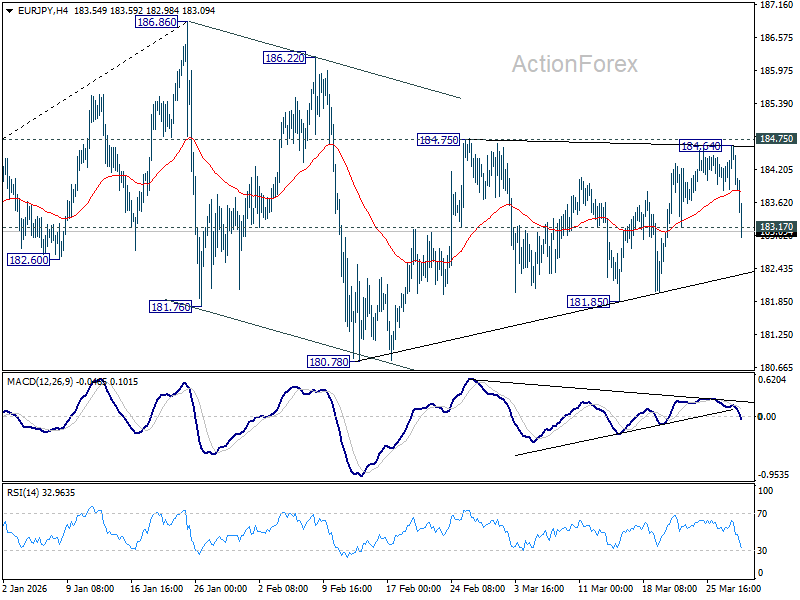

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 184.00; (P) 184.34; (R1) 184.81; More…

EUR/JPY’s accelerated decline and break of 183.17 minor support should confirm rejection by 184.75 resistance. Intraday bias is back on the downside for 181.85 support. Firm break there will argue that the correction from 186.86 is already in the third leg, and should target 180.78 and below. For now, risk will be on the downside as long as 184.64 holds, in case of recovery.

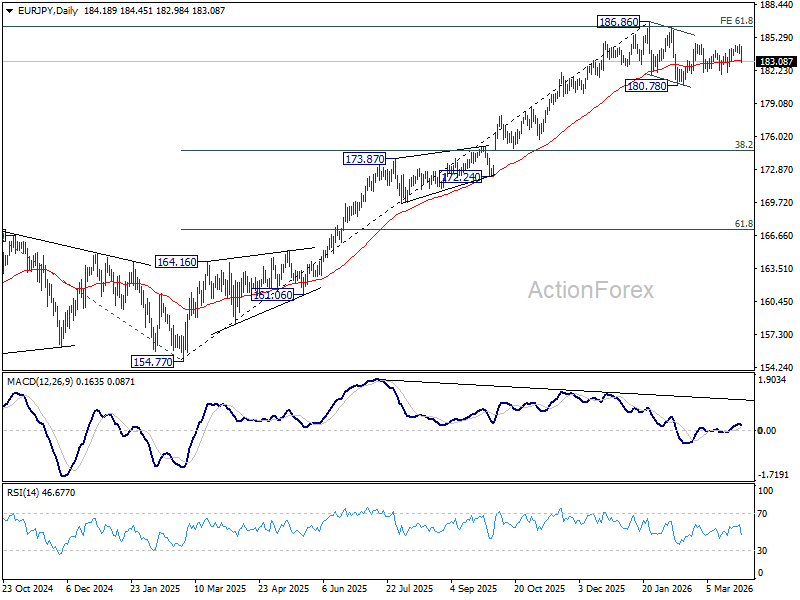

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.93) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

{kind=link}