The global energy market has effectively shrugged off a Wall Street Journal report suggesting US President Donald Trump is exploring an Iran exit strategy. Brent oil stays above $110 after a remarkably shallow dip. Asian stocks also turned red after a brief relief bounce. With the Strait of Hormuz still effectively blocked and the April 6 deadline for “complete obliteration” approaching, the current “skeptical hope” is being overwhelmed concerns over Oil supply risks.

The Wall Street Journal reported that Trump is willing to wind down the military campaign even if the Strait is not fully reopened, aiming to avoid a prolonged conflict beyond his preferred four-to-six-week timeline. The administration is said to be pivoting toward a “containment” strategy, relying on prior damage to Iran’s naval and missile capabilities while shifting the burden of reopening maritime routes to diplomatic efforts and regional allies.

However, markets are showing clear skepticism toward this narrative. Brent continues to hold above 110, with the recent rally still on track to retest the 120 psychological level. The limited downside response reflects the fact that core risks remain unchanged—military operations continue and the Strait of Hormuz is still largely closed, leaving global supply conditions tight.

More importantly, the downside scenario remains asymmetric. If no agreement is reached by the April 6 deadline to reopen the Strait, the U.S. could escalate by targeting critical infrastructure, including desalination plants, oil refineries, and the power grid. Such a move would likely force the IRGC to “go for broke,” attempting to sink remaining tankers to physically block the Strait with wreckage. Oil prices would than very likely shoot through the roof in this worst case scenario.

In currency markets, safe-haven demand remains evident. Yen is currently the strongest performers for the week so far, reflecting persistent risk aversion. Yen gains have been supported by intensified verbal intervention from Japanese authorities, reinforcing the 160 level in USD/JPY as a “Red Line”. Swiss Franc is also regaining traction as a defensive asset, benefiting from broader uncertainty. Dollar remains firm overall, supported by both safe-haven demand and elevated energy-driven inflation expectations.

On the other hand, risk-sensitive currencies are under pressure. Kiwi is the weakest performer, followed by Sterling and Aussie. In the case of the Australian Dollar, risk-off sentiment is outweighing expectations for further RBA tightening with multiple hikes in the months ahead. Euro and Loonie are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is down -1.01%. Hong Kong HSI is down -0.53%. China Shanghai SSE is down -0.25%. Singapore Strait Times is down -0.02%. Japan 10-year JGB yield is down -0.011 at 2.349. Overnight, DOW rose 0.11%. S&P 500 fell -0.39%. NASDAQ fell -0.73%. 10-year yield fell -0.098 to 4.342.

RBA Minutes Highlight Excess Demand and Oil Shock as Case for Further Tightening

RBA raised rates to 4.10% in a split 5–4 decision, with minutes showing growing concern over oil-driven inflation risks. The Board signaled more tightening may be needed, despite uncertainty around growth and the Middle East conflict. Read More.

China PMIs Return to Expansion as Output and Orders Rebound, but Cost Pressures Surge

China’s Manufacturing PMI rose to 50.4 in March, signaling a return to expansion as production and new orders improved. However, input costs surged sharply, while output prices lagged, pointing to growing margin pressure. Non-manufacturing activity also edged back into expansion. Read More.

NZ ANZ Business Confidence Tumbles to 32.5 as Cost Pressures Surge to Highest Since 2023

New Zealand business confidence tumbled in March as cost pressures surged to the highest since 2023, with more firms expecting to raise prices. Inflation expectations also climbed while activity outlook weakened, pointing to a growing stagflation risk. Read More.

Japan Tokyo CPI Core Weakens to 1.7% as Energy Subsidies Drag Inflation Lower

Tokyo CPI slowed to 1.7% in March, marking a second month below the BoJ’s 2% target as energy subsidies continued to suppress prices. However, the sharp slowdown in gasoline declines points to rising oil pressures beginning to offset policy support. The data highlight a fragile balance between near-term disinflation and emerging upside risks. Read More.

Japan Factory Output Contracts as Auto Weakness Weighs, Outlook Remains Uncertain

Japan industrial production fell -2.1% in February after a 4.3% rise in January, with weakness across most sectors led by autos. Retail sales also disappointed, pointing to soft demand, while unemployment edged lower to 2.6%. The data highlight a mixed outlook with fragile growth but stable labor conditions. Read More.

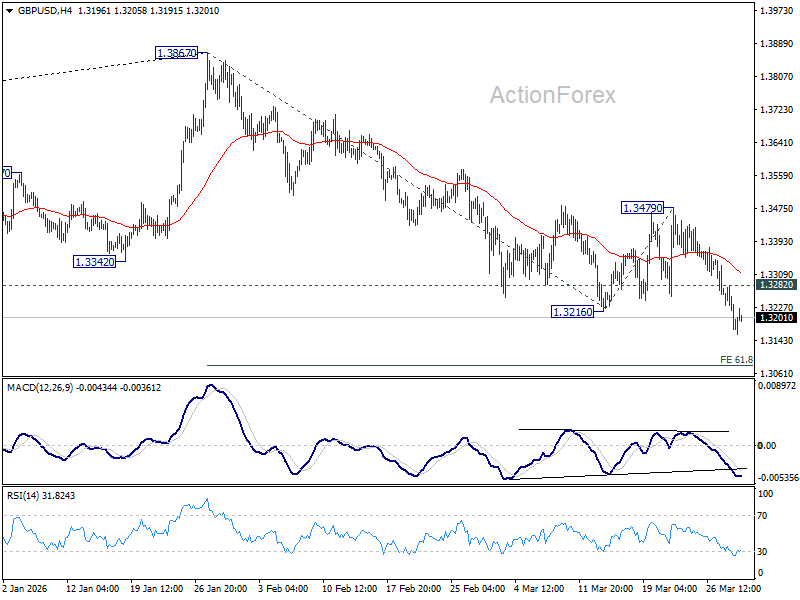

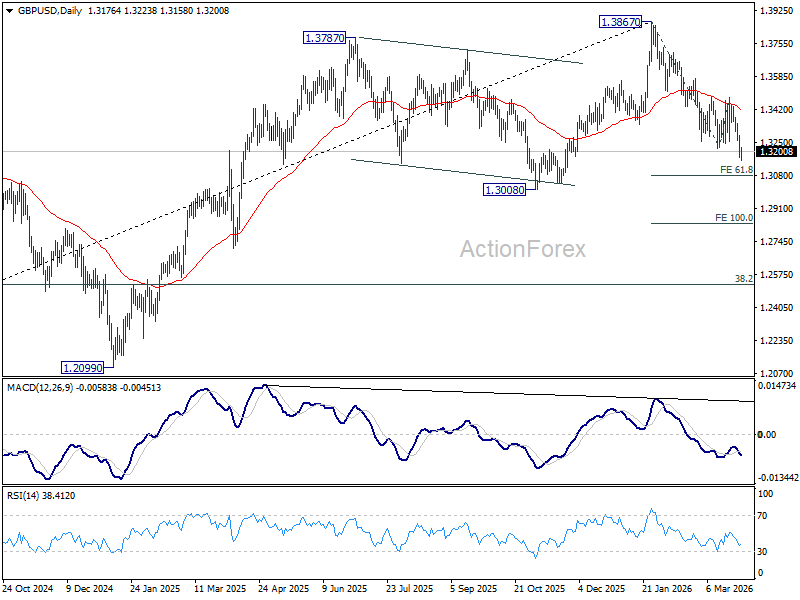

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3144; (P) 1.3213; (R1) 1.3253; More…

GBP/USD’s fall from 1.3867 resumed by breaking through 1.3216 support. Intraday bias is back on the downside for 61.8% projection of 1.3867 to 1.3216 from 1.3479 at 1.3077 first. Decisive break there could prompt downward acceleration through 1.3008 support to 100% projection at 1.2828. On the upside, above 1.3282 minor resistance will turn intraday bias neutral. But outlook will remain bearish as long as 1.3479 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

{kind=link}