Global forex markets turned notably quieter on Thursday as major currency pairs and crosses consolidated within Wednesday’s ranges. The pause came despite a sharp improvement in risk sentiment after Micron delivered blockbuster quarterly earnings, easing concerns that this week’s technology selloff had marked the beginning of a broader unwind in the AI trade. Asian equities responded enthusiastically, with Japan’s Nikkei surging 4.61% and South Korea’s KOSPI jumping 5.42%, leaving both indices back near the record highs reached only days earlier. US equity futures also pointed higher, though with considerably less conviction.

Currency markets, however, were far less impressed. The latest batch of US data, particularly May’s PCE inflation report, reinforced the Federal Reserve’s concerns over sticky price pressures and did little to weaken expectations for further policy tightening. With inflation remaining well above target and consumer spending staying resilient, September increasingly looks like the most likely timing for the next Fed rate hike.

Some major institutions are also forecasting another increase in December, while the most hawkish forecasts now call for three hikes in September, October and December. Against that backdrop, the Dollar continued to hold onto this week’s gains even as risk appetite recovered.

The strength of the Greenback has left its mark across markets. Gold has broken decisively below the key $4,000 psychological level, while Silver has fallen through $60 as investors reassess the outlook for US interest rates.

In the currency space, Dollar remains the week’s strongest performer. Yen ranks second, with USD/JPY once again pressing against the multi-decade high at 161.94, bringing the risk of Japanese intervention back into focus. Sterling is the third-best performer, with markets appearing to welcome Prime Minister Keir Starmer’s resignation.

At the other end of the rankings, New Zealand Dollar remains the weakest as falling oil prices reduce the urgency for further RBNZ tightening. Aussie is the second weakest after inflation, employment and spending data painted a mixed picture that keeps an August RBA hike possible but far from certain.Euro, Swiss Franc and Loonie are trading in the middle of the pack.

With no further top-tier economic releases due before the weekend, trading activity may remain subdued as investors turn their attention toward July and next week’s US non-farm payrolls report.

AUD/USD Stabilizes as Inflation, Jobs and Spending Keep August RBA Hike Alive

Headline inflation cooled, but that’s not the story the RBA is likely to focus on. Sticky core inflation, resilient household spending, and a labor market that continues to hold up have kept August rate hike expectations very much alive. Read More.

Silver Breaks Below $60, Can $50 Hold?

Silver’s break below $60 is only the beginning of the real story. The much more important battleground lies around $50, where powerful technical support meets strong industrial demand. The question is whether those forces can withstand a surging Dollar and increasingly hawkish Fed expectations. Read More.

US Core PCE Rises to 3.4%, Income and Spending Top Expectations

The Fed received little relief from May’s PCE report. Consumer spending remained strong, personal income accelerated, and inflation stayed well above target—a combination that keeps the case for further tightening intact. Read More.

US Durable Goods Orders Hit by Transportation, Underlying Demand Improves

The headline looked weak, but the details told a different story. Transportation orders drove May’s decline in US durable goods, while core orders posted a much stronger-than-expected gain, pointing to resilient business investment. Read More.

US Jobless Claims Fall to 215K, Labor Market Remains Resilient

The latest jobless claims report delivered good news and a note of caution. Layoffs remain low, but more Americans are taking longer to find new work. The labor market is cooling—but only gradually. Read More.

Schnabel: ECB Will Need More Rate Hikes Despite Middle East Ceasefire

Lower oil prices have not changed Isabel Schnabel’s message. The ECB Executive Board member says the ceasefire in the Middle East is “no reason” to relax policy, and she still expects further rate hikes to bring inflation back to 2%. Read More.

Germany Gfk Consumer Climate Improves Slightly as Inflation Fears Recede

Germany’s consumer mood is no longer deteriorating, but it isn’t recovering either. Lower oil prices and easing geopolitical tensions have reduced inflation fears, yet households remain reluctant to spend and continue to prioritize saving. Read More.

BoJ’s Tamura Lays Out Tightening Roadmap to 2%

Naoki Tamura didn’t just argue for more BoJ rate hikes—he outlined a roadmap. With quarter-point increases every few months toward a 2% neutral rate and the possibility of moving even faster, his remarks offer the clearest glimpse yet into how Japan’s tightening cycle could unfold. Read More.

Australia Employment Beats Forecasts, But April Revision Tempers Strength

Australia’s jobs report looked strong at first glance, with employment comfortably beating expectations. Dig a little deeper, however, and the picture becomes more balanced. A sharp downward revision to April and falling hours worked suggest the labor market is cooling gradually rather than reaccelerating. Read More.

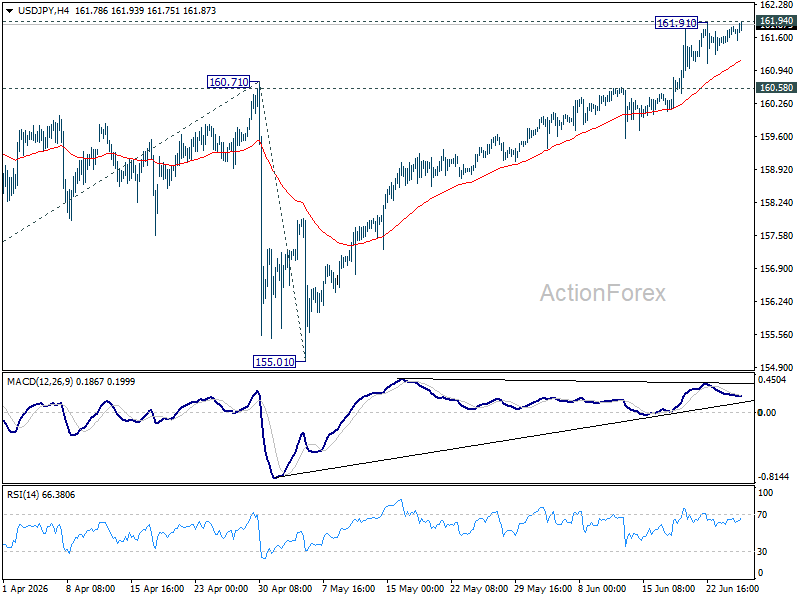

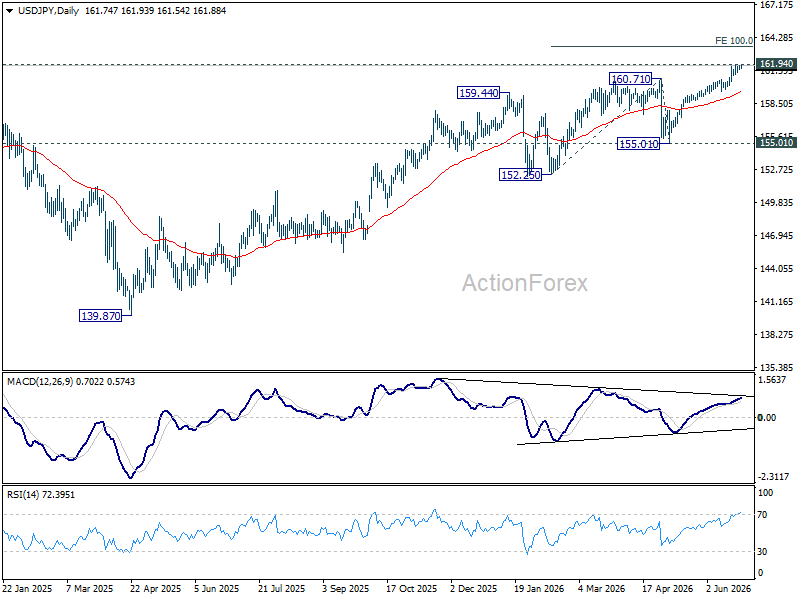

USD/JPY Daily Outlook

Intraday bias in USD/JPY remains neutral for the moment. On the downside, firm break of 160.58 support should confirm short term topping, on bearish divergence condition in 4H MACD. Deeper fall should then be seen to 55 D EMA (now at 159.46) and below. Nevertheless, decisive break of 161.94 high will resume the larger up trend to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. This will remain the favored case as long as 55 W EMA (now at 155.17) holds.

{kind=link}