US tax plan has now only one more step to take, President Donald Trump’s signature, and it will become law. Market’s reactions were relatively muted yesterday after House and Senate approvals. DOW closed slightly down by -0.11% at 24726.65. S&P 500 lost -0.08% to end at 2679.25. In the currency markets, Dollar trades mildly higher today, but remains the second weakest for the week. Yen is the worst performing one as pressured by powerful rally in treasury yields. BoJ’s standing pat provides little inspiration to the Japanese currency. Meanwhile, Euro remains the strongest one for the week, followed by Swiss Franc.

BoJ stands pat, dissented again

BoJ left monetary policies unchanged today as widely expected. Short term interest rate target was kept at -0.1%. Under the yield curve control framework, BoJ will continue to buy an annual amount of JPY 80T JGBs to keep 10 year yield at around 0%. Goushi Kataoka dissented again. In the statement, "Kataoka dissented, considering that, taking account of risk factors such as the consumption tax hike and a possible economic downturn in the United States, it was desirable to achieve the price stability target in fiscal 2018, and that it was appropriate for the Bank to purchase JGBs so that yields on JGBs with maturities of 10 years and longer would be broadly lowered."

BoJ maintained the "Japan’s economy is expanding moderately, with a virtuous cycle from income to spending operating." Assessments on consumption and and capex were upgraded. "Private consumption has been increasing moderately, albeit with fluctuations, against the background of steady improvement in the employment and income situation." "Capital expenditure continues to increase as a trend as corporate profits and business sentiment improve,"

Trump to sign tax bill into law soon

In the US, the House has finally passed the tax plan yesterday, after voting for a second time, and after Senate approved it. President Donald Trump is now expected to sign the bill into law but the exact timing is unclear yet. One of the main changes in the bill to cutting corporate tax rate from 35% to 21%, effective in 2018. Trump said that’s "probably the biggest factor in this plan" and "we’ve become competitive all over the world". Treasury Secretary Steven Mnuchin said Trump will "sign it as quickly as he can". But there are still some logistics to work on. The signing could be delayed to January 3.

Treasury yields continue powerful rally

US 10 year yield extended recent rally and took out 2.475 resistance decisively, closing at 2.497, up 0.034. There are a couple factors driving up global bond yields towards the year end. Tax cuts in the US are expected to result in increased bond selling in 2018. Meanwhile, Fed’s unwinding of the balance sheet will also increased supply. On the other hand, Germany has already indicated to sell more 30 year bunds next year. ECB will also cut down its bond purchases.

TNX’s rally firstly confirms rebound of the rebound from 2.034. And more importantly, it affirms that case that medium term correction from 2.621 has completed at 2.034. And up trend from 1.336 could be resuming. A break of 2.621 next year will pave the way to 61.8% projection of 1.336 to 2.621 from 2.034 at 2.827. Such development could be accompanied by USD/JPY breaking 2016 high at 118.65.

On the data front

New Zealand GDP grew 0.6% qoq in Q3, meeting expectation. UK Gfk consumer confidence dropped to -13 in December. Swiss trade balance and UK public sector borrowing are the main feature in European session. Canada CPI and retail sales will likely trigger some movements in Loonie later in the day. US will release Philly Fed survey, jobless claims, house price index, leading indicators and Q3 GDP final.

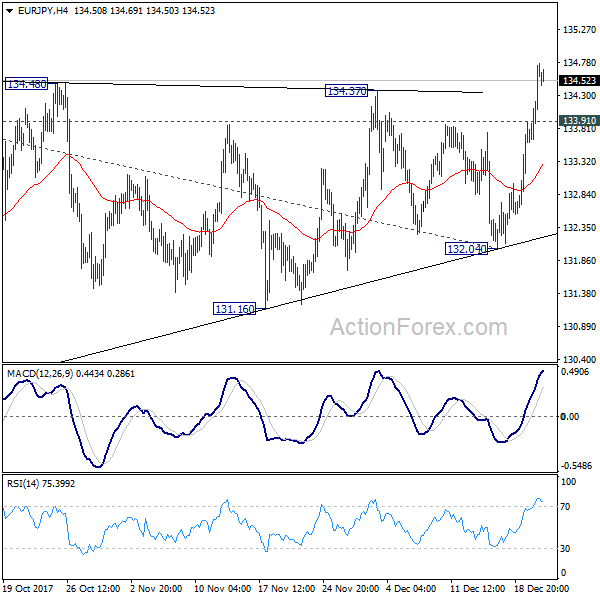

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.86; (P) 134.32; (R1) 135.04; More….

EUR/JPY surges to as high as 134.76 so far. Break of 134.39 resistance indicates resumption of medium term up trend. Intraday bias is now on the upside. Rally from 132.04 should target 61.8% projection of 114.84 to 134.39 from 132.04 at 144.12. Ideally, upside acceleration should be seen in the current move with daily MACD taking out down trend line. On the downside, below 133.91 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 132.04 key support holds.

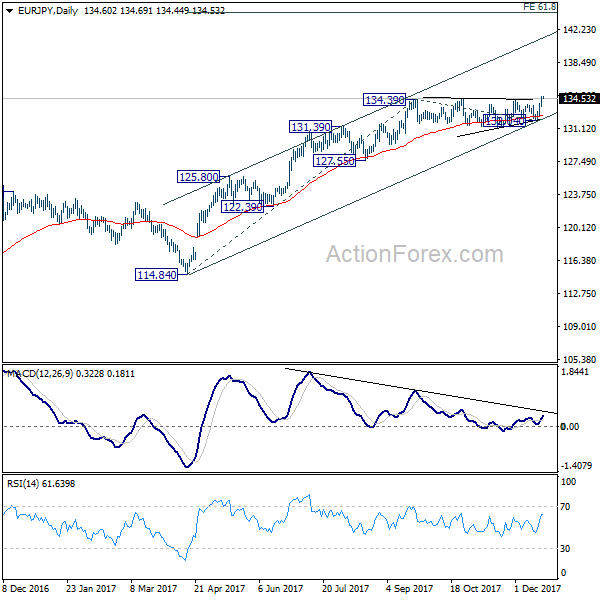

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 132.04 support will suggest medium term topping and will turn outlook bearish for deeper fall back 55 week EMA (now at 127.82).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | 0.60% | 0.60% | 0.80% | 1.00% |

| 0:01 | GBP | GfK Consumer Confidence Dec | -13 | -12 | -12 | |

| 2:00 | JPY | BOJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 7:00 | CHF | Trade Balance Nov | 2.84B | 2.33B | ||

| 9:30 | GBP | Public Sector Net Borrowing Nov | 8.6B | 7.5B | ||

| 13:30 | USD | Philly Fed Manufacturing Index Dec | 20.8 | 22.7 | ||

| 13:30 | CAD | CPI M/M Nov | 0.20% | 0.10% | ||

| 13:30 | CAD | CPI Y/Y Nov | 2.00% | 1.40% | ||

| 13:30 | CAD | CPI Core – Common Y/Y Nov | 1.60% | |||

| 13:30 | CAD | CPI Core – Trim Y/Y Nov | 1.50% | |||

| 13:30 | CAD | CPI Core – Median Y/Y Nov | 1.70% | |||

| 13:30 | CAD | Retail Sales M/M Oct | 0.30% | 0.10% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Oct | 0.40% | 0.30% | ||

| 13:30 | USD | Initial Jobless Claims (DEC 16) | 234K | 225K | ||

| 13:30 | USD | GDP Annualized Q/Q Q3 T | 3.30% | 3.30% | ||

| 13:30 | USD | GDP Price Index Q3 T | 2.10% | 2.10% | ||

| 14:00 | USD | House Price Index M/M Oct | 0.40% | 0.30% | ||

| 15:00 | USD | Leading Index Nov | 0.40% | 1.20% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec A | 0.2 | 0.1 | ||

| 15:30 | USD | Natural Gas Storage | -69B |