Dollar trades generally lower in Asian session as it has turned into correction mode. While slightly more hawkish than expected, the FOMC statement released overnight provided little inspiration to the markets. Major US equity indices ended in red, with DOW dropped -0.72%, S&P 500 down -0.72% and NASDAQ lost -0.42%. 10 year yield also closed slightly lower by -0.012 to 2.964. In the currency markets, Dollar is staying as the strongest one for the week, followed by Canadian Dollar and Japanese Yen. The markets will looks into today’s data from US, Eurozone and UK for more guidance.

Fed stands pat, more comfortable on inflation

As widely anticipated FOMC left the Fed funds rate target at 1.5-1.75% overnight. The accompanying statement also came in largely in line with our expectations – shrugging off moderation in first quarter growth and getting more confident in the inflation outlook. The central bank indicated that “both overall inflation and inflation for items other than food and energy have moved close to 2%”, while in March, they noted that those barometers “have continued to run below 2%”. Meanwhile, the members judged that “Inflation on a 12-month basis is expected to run near the Committee’s symmetric 2% objective over the medium- term”. A rate hike in June appears a done deal. The updated economic projections and the median dot plot would also be released in the June meeting. The market would be closely watching if the members have raised their rate hike expectations to four times from three. More in FOMC More Hawkish on Inflation, June Rate Hike a Done Deal

And more on FOMC:

- Fed Keeping Things Gradual with Steady Decision and Balanced Statement

- Amid Rising Inflation, The Fed Remains on Course

- Fed Stands Pat But Appears Ready to Hike More Given its Newfound Comfort with Inflation

Mnuchin arrives in Beijing as China warns to stand up to US bullying

US Treasury Secretary Steven Mnuchin arrives in Beijing today and is set to kick start trade negotiation with Chinese Vice-Premier Liu He. Mnuchin told reporter he’s “thrilled to be here” upon arriving his hotel. The delegation planned to leave Friday evening.

Ahead of the meeting, the official China Daily said in a editorial that it will “stand up to the US’ bullying as necessary”. And “as a champion of globalisation, free trade and multilateralism, it will have strong support from the international community”. It warned that “the US wants greater access to China’s market, but it should not use trade actions as a battering ram to force China to open its doors.”

Trump still claimed he always has a good relationship with Chinese President Xi in his tweet ahead of the meeting. He said that “Our great financial team is in China trying to negotiate a level playing field on trade! I look forward to being with President Xi in the not too distant future. We will always have a good (great) relationship!”

Australian Dollar lifted by large trade surplus and surge in building approvals

AUD trades broadly higher today as supported by solid economic data. Australia trade surplus came in at AUD 1.53B in March, widened from AUD 1.35B in February. That’s also much larger than expectation of AUD 0.68B. Exports jumped 1% to AUD 34.84B, with strong 8% growth in n non-monetary gold to AUD 131m. Imports rose 1% to AUD 33.31B,. Non-monetary gold imports jumped 28% to AUD 232m.

Building approvals rose 2.6% mom in Mach, much higher than expectation of 1.0% mom. Justin Lokhorst, Director of Construction Statistics at the ABS noted that “the strength in the total dwellings series is being driven by approvals for private sector houses, which have now risen for 13 consecutive months.” And, “private sector house approvals are now at their highest level since 2003, in trend terms.”

Sterling and Euro to face more data tests

While Sterling and Euro survived yesterday’s tests from economic data, they’re both facing another day of event risks. From UK, PMI services is expected to climbed back from 51.7 to 53.5 in April. The data should show how well the economy is rebounded after “bad weather” in Q1. Eurozone will release CPI which is expected to be unchanged at 1.3% yoy in April. European Commission will also release new economic forecasts. Later in the day Canada will release trade balance. US will release trade balance, jobless claims, ISM services and factory orders.

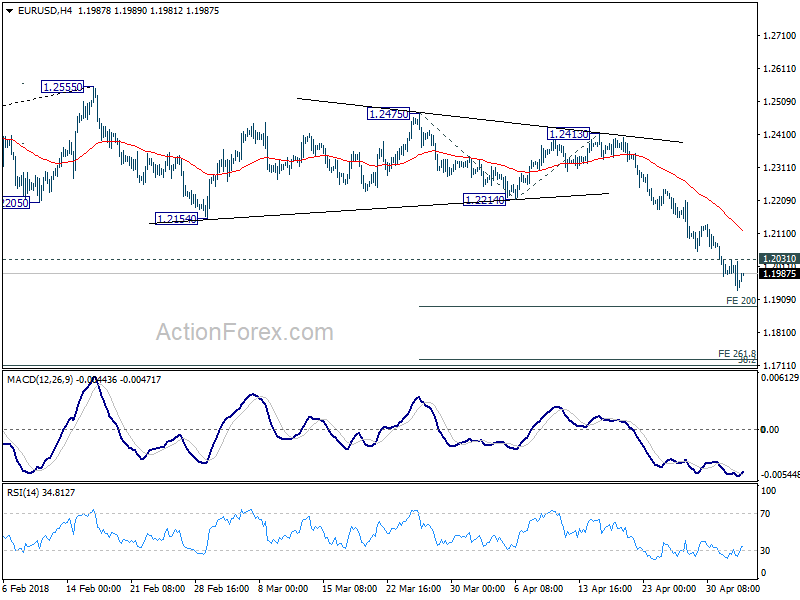

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1973 (R1) 1.2008; More….

EUR/USD dipped further to as low as 1.1937 but started to lose downside momentum on oversold condition in 4 hour RSI. For the moment, intraday bias stays on the downside with 1.2031 minor resistance intact. Next target is 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Break will target 261.8% projection at 1.1730. On the upside, though, break of 1.2031 will indicate short term bottoming and bring lengthier consolidation before staging another fall.

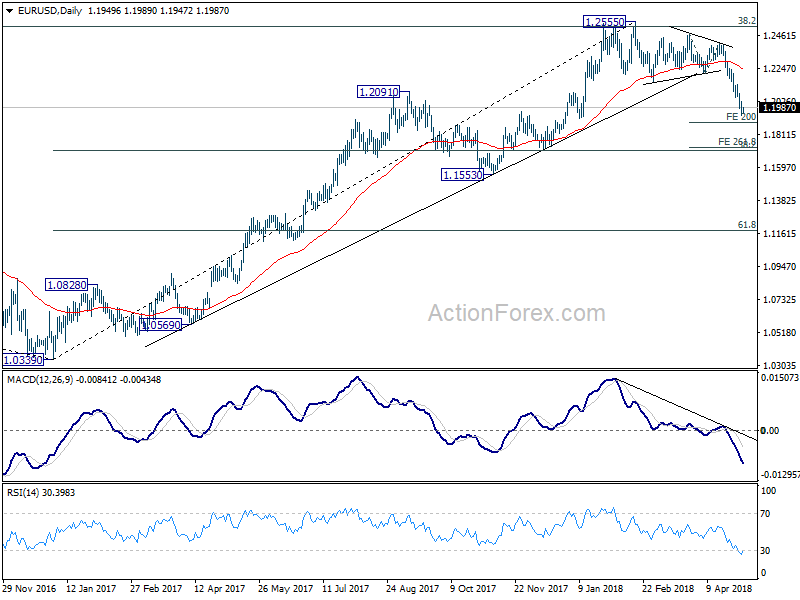

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we’ll need to look at the structure to before deciding if it’s a corrective or impulsive move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Trade Balance Mar | 1.53B | 0.68B | 0.83B | 1.35B |

| 1:30 | AUD | Building Approvals M/M Mar | 2.60% | 1.00% | -6.20% | -4.20% |

| 8:30 | GBP | Services PMI Apr | 53.5 | 51.7 | ||

| 9:00 | EUR | Eurozone PPI M/M Mar | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Mar | 2.10% | 1.60% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Apr | 1.30% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Apr A | 0.90% | 1.00% | ||

| 9:00 | EUR | European Commission Economic Forecasts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 39.40% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Mar | -2.0B | -2.7B | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | 1.00% | 0.00% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | 3.00% | 2.50% | ||

| 12:30 | USD | Initial Jobless Claims (APR 28) | 225K | 209K | ||

| 12:30 | USD | Trade Balance Mar | -55.6B | -57.6B | ||

| 13:45 | USD | US Services PMI Apr F | 54.4 | 54.4 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Apr | 58.1 | 58.8 | ||

| 14:00 | USD | Factory Orders Mar | 1.40% | 1.20% | ||

| 14:30 | USD | Natural Gas Storage | -18B |

{kind=link}