{kind=link}

Dollar continues to trade as the weakest major currency as another week starts. Over the month, the greenback is trading weakest against Kiwi and Aussie. Meanwhile, Euro is catching up as Germany is closer to reforming the grand coalition. Sterling follows on improving prospects of a favorable Brexit deal. For the moment, it’s unclear which is the main driving force behind Dollar’s selloff. The fact that other global central banks are catching up on tightening is a factor. Surge in commodity prices is another one. But these two factors are not strong enough to send the Dollar index to three year low. The concerns of China’s consideration to move away from Dollar assets could be the more important reason.

Bundesbank Weidmann: Immediate risk of hike currently low

ECB known hawk Bundesbank Jens Weidmann tried to tone down the chance of rate hike over the weekend. He expressed that "it would be particularly stressful for the banks if the long period of low interest rates were to be ended by a rapid, sharp increase in interest rates." And, "as far as central bank rates in the euro area are concerned, however, the immediate risk of change is currently low." His comments are generally in line with the view that while ECB minutes hinted on change of communications, the central bank is still far from raising interest rates. And it should be noted that various ECB officials have indicated last year that there is a sequence in stimulus exit, that is, the asset purchase program would have to stop before rate hikes.

BoC to rate hike on Wednesday despite NAFTA concerns

Bank of Canada rate decision on Wednesday will be the major focus for the week. After recent strong economic data, it’s widely expected that BoC would hike again by 25bps to 1.25%. There are still concerns over the outcome of NAFTA negotiations. There is possibility of US pulling out from the decades long agreement. But it’s clear that labor market slacks have diminished clearly. The Q4 business outlook survey also indicated solid hiring and investments. Hence, BoC will still likely look pass the NAFTA risks and hike again.

Other key focuses include UK inflation and retail sales, Fed’s Beige Book report, Australia employment and China data. Here are some highlights for the week ahead:

- Monday: Eurozone trade balance

- Tuesday: Japan PPI; German CPI final; UK CPI, PPI; US Empire state manufacturing;

- Wednesday: Japan machine orders; Australia home loans; Eurozone CPI final; US industrial production, NAHB housing index, Fed’s Beige book; BoC rate decision

- Thursday: Australia employment; China GDP, industrial production fixed asset investment, retail sales; US housing starts, jobless claims, Philly Fed survey

- Friday: New Zealand business manufacturing index; German PPI; Swiss PPI; Eurozone current account; UK retail sales; Canada manufacturing sales; US U of Michigan sentiment

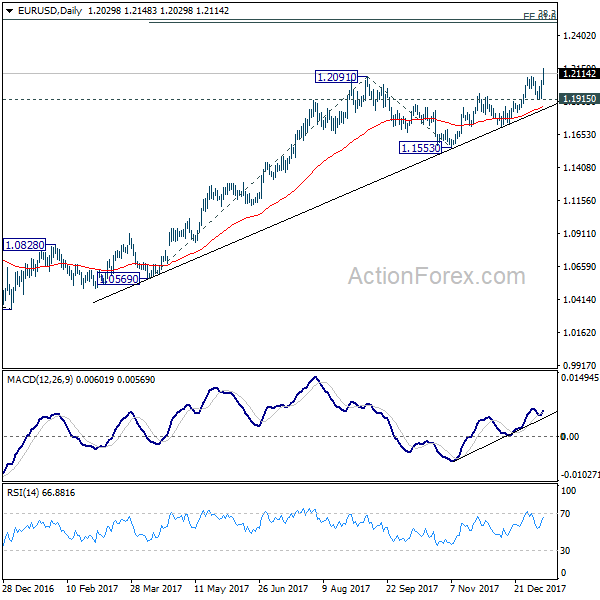

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2079; (P) 1.2149 (R1) 1.2267; More….

EUR/USD reaches as high as 1.2239 so far as recent rally extends. Intraday bias remains on the upside for 1.2494/2516 key resistance zone next. At this point, we’d continue to expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2121 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 1.1915 support holds.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we’d be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Dec | 3.60% | 4.00% | 4.00% | |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.10% | 0.20% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 22.4B | 19.0B |