Yen ended last week as the weakest one as the global markets were in full risk on mode. DOW finally made a new record high, together with S&P 500 and the strength is not limited to the US. Nikkei closed up 3.36% and is now very close to 24129.34 (2018 high). Even the China Shanghai SSE closed up 4.32%, just missing 2800 handle. It’s the same in Europe with DAX gained 2.53% and CAC added 2.64%. Treasury yields across the Atlantic also soared with US 10-year yield reclaimed 3% handle. German 10 year bund yields also breached 0.5% but failed to stand firm above.

The escalation of US-China trade war was largely ignored by the markets. Dollar ended as the second weakest one. New Zealand Dollar and Australia Dollar, two currencies most sensitive to US-China trade tensions, were the best preforming ones. Meanwhile, Sterling was the third weakest as Brexit negotiation is now at an impasse after the informal EU summit in Austria.

US-China trade war just took a mickey mouse step

Looking back, the reactions to new round of US-China tariffs showed that investors were actually relieved. USTR announced 10% tariffs on USD 200B in Chinese imports, effective September 24. Tariff ate will be raised to 25% on January 1, 2019. China swiftly announced retaliation on USD 60B imports, tariff rates at 5% and 10%.

It’s certainly not the worst case scenario, and far from. So what should be the worst? Imagine Trump kept the original rate of 25% tariffs, effective September 24 too. At the same time, he started the process on tariffs on USD 267B of Chinese goods immediately, and assume that the rate is also 25%. Then we could have 25% tariffs on nearly all Chinese imports by year end, with equivalent countermeasures by China. Comparing to this worst case scenario, the move announced last week was just a mickey mouse step.

Dollar and treasury yield at critical levels, FOMC to decide their fate

Anyway, the overall developments now put Dollar and yields at very critical levels. Both 10- and 30-year yields are now pressing key long term resistance. At the same time, Dollar is trying to draw support from key level against Euro. Technically, our base case is for Dollar to have a strong rebound and bullish reversal from the current level. Meanwhile, treasury yields would finally take out the multi decade trend defining resistances. But we can be wrong.

The eventual outcome will very much depend on FOMC meeting this week. There is no doubt that Fed will raise federal funds rate by 25bps to 2.00-2.25%. Voting could be a point of interest as some doves have voiced concerns over flattening yield curve. But more importantly, the new economic projections could be most market moving. In particular, Fed’s projections on the longer run federal funds rate. It’s estimated to be at 2.9% in June projections. And it’s the point where policymakers could see interest rate of being restrictive going beyond. This provides the anchor for assessing how far the current rate hike cycle would go. Any uplift in this figure would send Dollar and yields soaring.

US yield surged sharply, more strength at the long end

US treasury yields had a strong rally last week, in particular in the long end. 5-year yield closed the week up 0.056 at 2.954. 10-year yield rose 0.074 to 3.068. 30-year yield rose 0.073 to 3.205. Now, both 10 year yield and 30 year yield are back at important resistance levels.

30 year yield (TYX) is facing 3.255 cluster support, with 61.8% retracement of 3.976 to 2.102 at 3.260. The strong support seen from 55 week EMA (now at 2.999) is a sign of underlying bullishness Weekly MACD also stayed positive during the last consolidation pattern. Near term outlook will remain bullish as long as last week’s low at 3.120 holds. Decisive break of 3.255/60 will set up a medium term move to 3.976 resistance next.

It should also be noted if the bullish case is realized, the multi-decade channel resistance will also be taken out rather decisively. And it’s certainly a very bullish development for yields.

10 year yield is looking more bullish then TYX. The consolidation from 3.115 was contained well above 55 week EMA (now at 2.731). Weekly MACD stayed positive throughout. Near term outlook will remain bullish as long as last week’s low at 2.989 holds. Firm break of 3.115 will resume whole up trend from 1.336 (2016 low).

Also, next medium term rally will have multi-decade channel resistance taken out. Prior key resistance at 3.036 will be left behind formally. And the development could establish the next medium to long term up trend back towards 5.316. That’s a confirmation of end of the era of falling US yields.

Dollar index looking at 93.64 fibonacci level for support

The above bullish case in yield is yet to be confirmed. But if they do happen, it should be very strong support to the greenback. And talking about Dollar, the selloff in the greenback last week was not too unexpected. Dollar index’s correction from 96.68 extended to as low as 93.81 but was kept above 38.2% retracement of 88.25 to 96.98 at 93.64 so far. That was equivalent of EUR/USD breaching 1.1779 fibonacci resistance. Also the structure of the decline from 96.98 is so far corrective looking, which doesn’t violate our view.

For now, we’d continue to expect this 93.64 fibonacci level to hold, as it’s also in proximity to 55 week EMA (now at 93.86). There would be high chance of lifting DXY through 95.73 resistance should TNX and TYX could take out the above mentioned key resistance levels. However, strong rejections by the resistance in TNX and TYX would likely drag dollar index through 93.64 to set up deeper medium term correction.

Position trading strategy

Our sell EUR/GBP strategy was cancelled last week as the cross dipped through 0.8875 support first, before staging a strong rebound towards weekly close. But admittedly, the strategy was wrong. We anticipated some negative news in the early part of the week but eventually, something would be agreed at the EU summit regarding Brexit deal. Unfortunately, the only thing that EU and UK agreed was that they disagreed. EU saw UK Prime Minister Theresa May’s Chequer’s plan us unworkable. May blamed that EU provided no counterproposals after rejection. The deadlock will continue at least until the next EU summit in October.

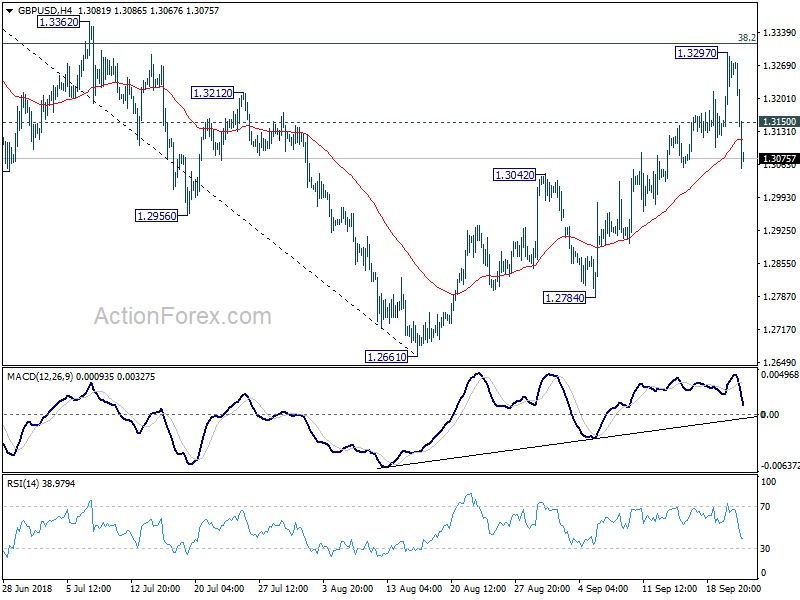

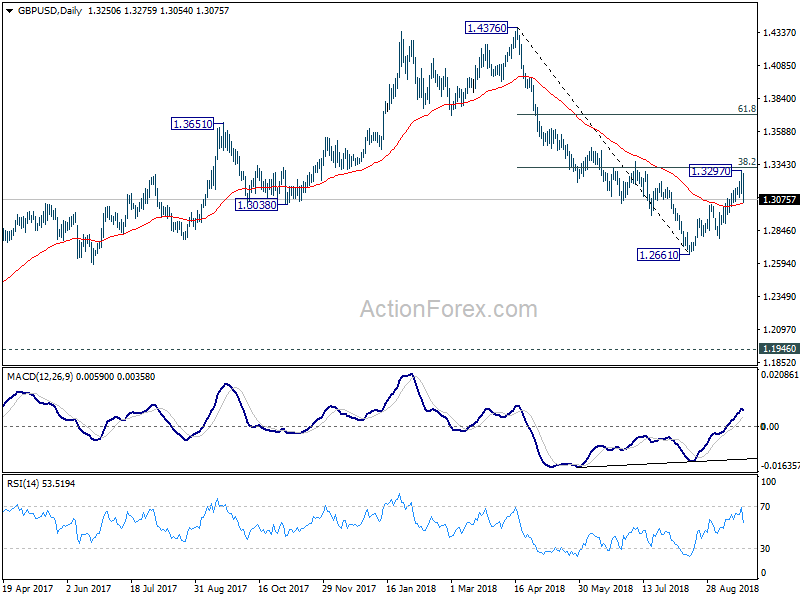

On this week’s strategy, we’d like to take on a higher risk one in buying Dollar. As noted above, technically, it’s the point where Dollar should have a rebound. Based on recent strong data, we don’t expect a dovish twist in FOMC announcement. The most dovish scenario is that it doesn’t hawkish-up and disappoints the markets. Yen is naturally a good choice considering strong stock and yield rally. But we’d tend to avoid it as it’s too close to 113.17 resistance. EUR/AUD’s rejection from 1.6172 suggests that Aussie is having an upper hand over Euro. EUR/GBP’s strong rebound from 0.8847 indicates Sterling is even weaker. Hence, it brings us back to the miserable pound.

Considering GBP/USD is close to 55 day EMA (now at 1.3051), we’ll sell GBP/USD on recovery to 1.3150. Stop will be placed at 1.3300, slightly above 1.3297 top. 1.2661 low will be the target. Risk/reward ratio at 1: 3.26, which is acceptable. Depending on the downside momentum, if things turn out right, we might hold the position through 1.2661.

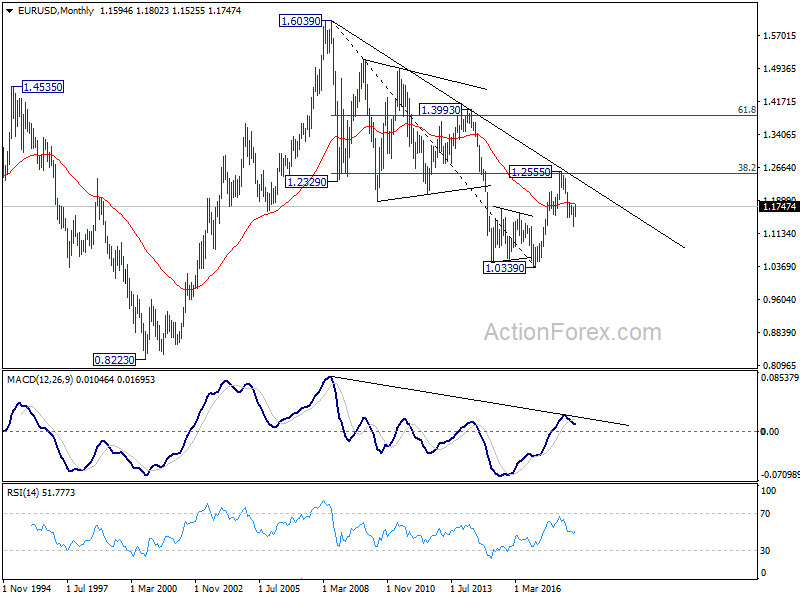

EUR/USD Weekly Outlook

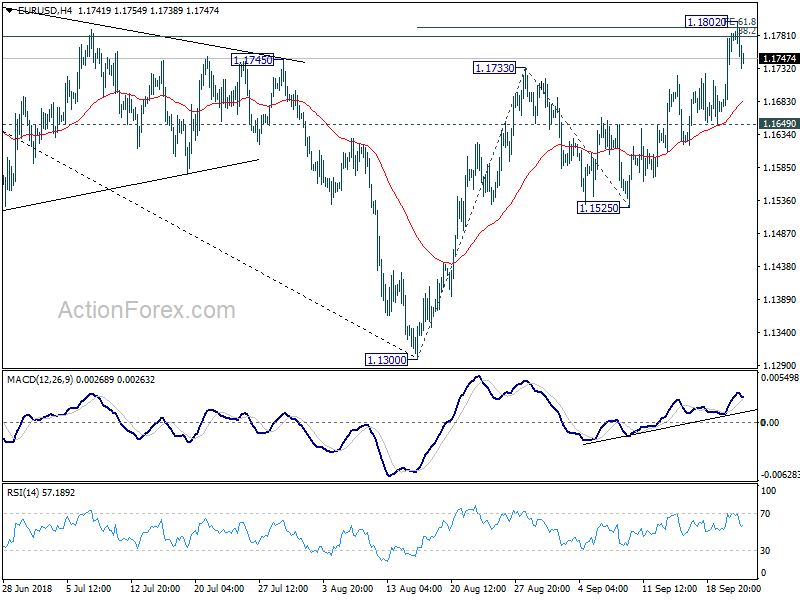

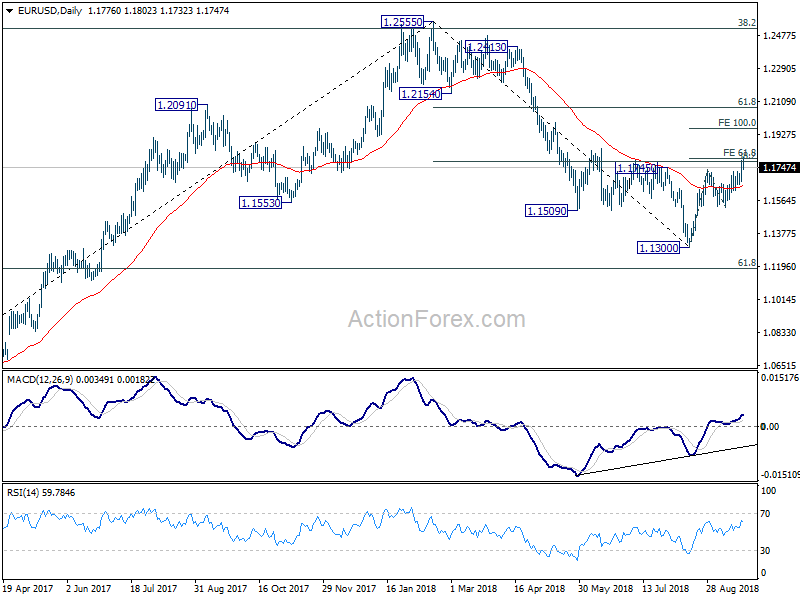

EUR/USD surged to as high as 1.1802 last week but failed to sustain above 38.2% retracement of 1.2555 to 1.1300 at 1.1779 and retreated. Initial bias is neutral this week first. At this point, we maintain our view that 1.1779 should limit upside, at least on first attempt, to bring near term reversal. On the downside, break of 1.1649 minor support will be the first signal that corrective rise from 1.1300 has completed. Intraday bias will be turned to the downside for 1.1525 support first. Break will confirm and bring retest of 1.1300 low. However, sustained break of 1.1779 will extend the corrective rise from 1.1300 to 100% projection of 1.1300 to 1.1733 from 1.1525 at 1.1958 before completion.

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

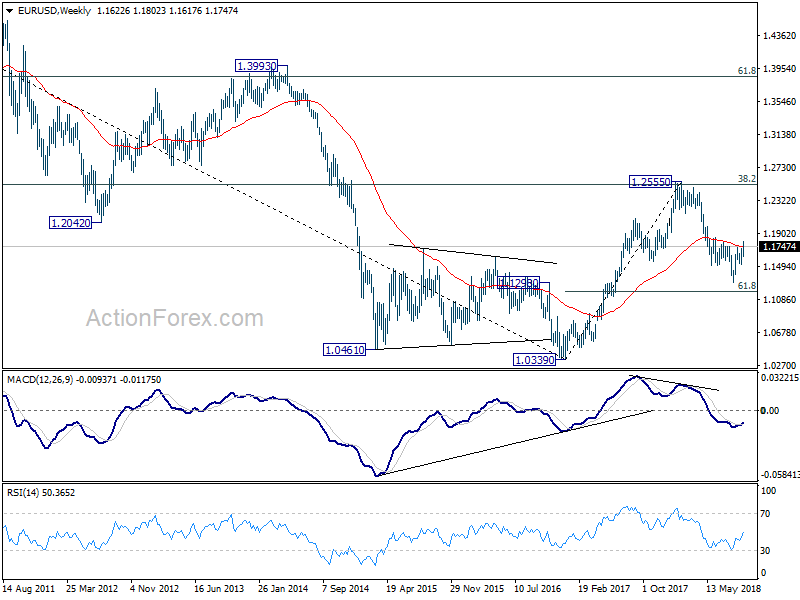

In the long term picture, the rejection from 38.2% retracement of 1.6039 to 1.0339 at 1.2516 argues that long term down trend from 1.6039 (2008 high) might not be over yet. EUR/USD is also held below decade long trend line resistance. Firm break of 61.8% retracement of 1.0339 to 1.2555 at 1.1186 should at least bring a retest on 1.0339 low.

{kind=link}