Dollar ended last week as the weakest one after deep selloff before weekly close. A whole lot of events are scheduled ahead to keep the greenback busy. Those include FOMC rate decision, US-China trade talk, non-farm payrolls. Also, the partial government shutdown has finally ended temporarily and we’ll have more economic data for gauging the economy of the US. Australian Dollar ended as the second weakest but it has already pared back much losses after Friday’s rebound. Yen followed as the third weakest.

Sterling ended as the strongest one and maintained strengthen towards the end. It’s boosted by receding chance of no-deal Brexit. The debate and vote on amendments in the Commons on Tuesday will likely provide a more concrete path forward regarding Brexit. New Zealand Dollar was the second strongest after solid CPI lowered chance of an RBNZ cut. Euro was surprisingly resilient and survived a batch of weak data as well as dovish ECB. The common currency will face tests from GDP and CPI this week.

FOMC, trade war, NFP and reopened government to keep Dollar busy

Dollar performed not too badly for most part of the week, until it suffered heavy selloff on Friday. The WSJ reported Fed is considering to stop shrinking it’s massive balance sheet earlier. That is, the eventual size of the portfolio of treasury securities could be larger than originally expected. This is seen as move in response to the adverse stock market condition back in December. Some policy makers might want to take the balance sheet reduction off autopilot. This is definitely a topic Fed Chair Jerome Powell would be scrutinized in the post FOMC meeting press conference on Wednesday.

Besides FOMC meeting, there are full of events in the US this week. Trump finally gave up the demand for the border wall temporarily on Friday. He agreed to a deal, without funding for the wall, that ended the 35-day historic government shutdown. The deal was then quickly passed by Senate and House without opposition. Now, the Congress will have up till February 15 to debate on border security. A whole lot of economic data, which missed schedule release day, will likely come up gradually this week. And, more than that, January non-farm payrolls and ISM manufacturing will be featured.

The highly anticipated meeting between US Trade Representative Robert Lighthizer and Chinese Vice Premier Liu He will take place on January 30-31 in Washington. Ahead of that, there will be vice ministerial meetings on Monday and Tuesday. Comments from the US side has been rather conflicting. On the one hand, Commerce Secretary Wilbur Ross said the two countries are “miles and miles” away on a trade deal. But White House economic adviser Larry Kudlow said Trump is optimistic. But one thing for sure, there is so far no news regarding how Chines is going to handle the biggest concerns of the US, including intellectual property threat, forced technology transfer, and opening up market access. Let’s see if there will be any real progress in the negations.

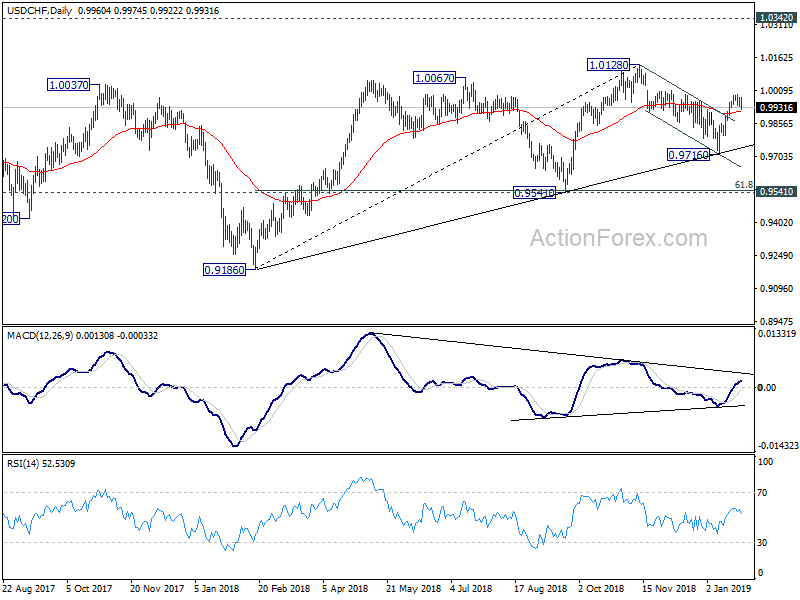

Dollar index to extend correction from 97.71 through 95.02

Dollar index’s sharp decline on Friday is rather near term bearish. It suggests failure to sustain above 55 day EMA. And, the rebound from 95.02 has completed at 96.67 already. Corrective decline from 97.71 might now be ready to resume for 95.02 and below. But after all, downside should be contained by 93.81/94.09 support zone (38.2% retracement of 88.25 to 97.71 at 94.09) to bring rebound. Meanwhile, even in case of recovery, risk will now stay on the downside as long as 96.67 holds.

DOW’s not that strong close was rather disappointing

While DOW jumped to as high as 24860.15 but closed way off this high at 24737.20. The close is indeed rather disappointing considering the Fed balance sheet rumor as well as news on ending government shut down. For now, further rise is still in favor as long as 24244.31 support holds. However, it looks like even in case of rally, DOW will start to feel heave in 24932.09/25820.34 resistance zone (61.8% and 78.6% retracement of 26951.81 to 21664.59).

Euro and DAX survived dovish ECB and weak economic data

Euro survived some very weak economic data, as well as dovish ECB last week. It ended higher against all major currencies except Sterling and New Zealand Dollar. Adding to that, German DAX and French CAC ended the week higher, extending recent rebound. It seems that investors are seeing the worst in Eurozone is behind.

ECB President Mario Draghi noted in the post meeting press conference that “the risks surrounding the Euro area growth outlook have moved to the downside”. This is the first time since April 2017 that the central bank admitted that risks are to the downside. Over the past 21 months, ECB had been describing risks as “broadly balanced”, while suggesting the balance is “moving to the downside”. The uncertainties ECB has identified are “geopolitical factors and the threat of protectionism, vulnerabilities in emerging markets and financial market volatility”.

Meanwhile, Eurozone PMI composite dropped to 50.7, a 66-month low. Both manufacturing and services were close to stagnation at 50.5 and 50.8. They were at 50-month and 65-month low respectively. German ZEW economic sentiment improved to -15 but stayed well below long term average of 22.4. ZEW Current Situation dropped sharply to 27.5, down from 45.3. German Ifo business climate dropped to 99.1, lowest since February 2016.

Looking ahead, Q4 GDP in Eurozone will be released and is expected to slow to 0.2% qoq. Eurozone CPI will also be featured and is expected to slow -0.2% to 1.4% yoy in January. We’ll see if Euro could maintain its resilience.

Along side the strength of Euro, German DAX was also strong last week. In particular, Rebound from 10279.20 resumed on Friday by gapping higher. 55 day EMA is considered firmly taken out, which is bullish. Adding to that, there was bullish convergence condition in daily MACD. It’s still early to confirm reversal of the down trend from 13596.89. But for now, there is prospect of further near term rebound to 11726.62 support turned resistance, which is also close to medium term channel resistance.

Sterling strong as campaign for no-deal Brexit gathers momentum

Sterling ended as overwhelmingly the strongest as the campaign to rule out no-deal Brexit gathered momentum. The House of Commons will hold another day of Brexit debate on Tuesday, January 29. Given that Prime Minister Theresa May’s Plan B is so very much like the original Plan A, it’s not really the focal points of the debate. Instead, attentions and debates will be on the next steps as put forward as amendments to the Brexit deal.

One of the most high profile amendments was put forward by Labour MP Yvette Copper, which has cross party support. In short, if May couldn’t get a deal approved by the parliament by February 26, the parliament will be give a vote on postponement of Article 50 by nine months, to avoid a no-deal Brexit. The chance of getting this amendment through jumped after Labour finance chief said the party will highly likely support it. Also,

Other amendments including putting an expiry date to the Irish backstop, holding a second referendum, ruling out no-deal Brexit with other means. We’ll have a much better idea on what’s next after Tuesday. And, if a no-deal Brexit is pretty much ruled out, Sterling could be give another boost.

Position trading

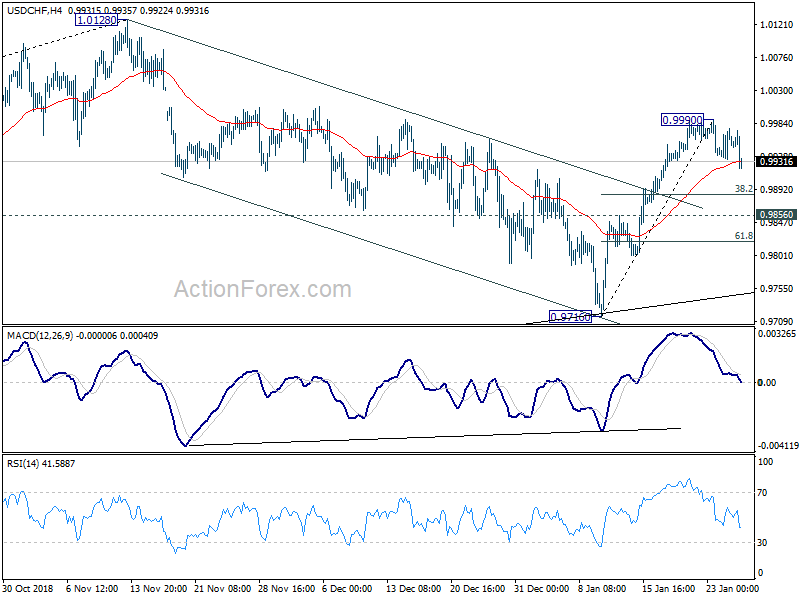

Our buy USD/CHF at 0.9920 order was not filled last week as it rose to 0.9990 and then dropped to 0.9922 before closing at 0.9931. The entry was just missed.

Dollar will likely be under some mild pressure this week, at least initially, as also reflected in Dollar index outlook mentioned above. But Swiss Franc is unlikely to benefit much from it. Firstly, rebound in European stocks, as seen with DAX above, is set to extend. Secondly, strength, or at least resilience in emerging market currencies, for example in USD/ZAR and USD/TRY, will limit Franc rally too.

And, technically, we maintain the view that corrective fall from 1.0128 has completed at 0.9716 after drawing support from medium term trend line, on bullish convergence condition in 4 hour MACD. Hence rise from 0.9716 should resume after completing the retreat from 0.9990. And such rise is likely resuming whole up trend from 0.9186.

Hence, we’ll continue to try to buy USD/CHF, but at a lower entry. We’ll buy USD/CHF at 0.9880, around 38.2% retracement of 0.9716 to 0.9990 at 0.9885. Stop will be placed at 0.9810, below 61.8% retracement at 0.9821. Target is placed at 1.0300, as we expect the upside to extend to take on 1.0342 resistance (2017 high).

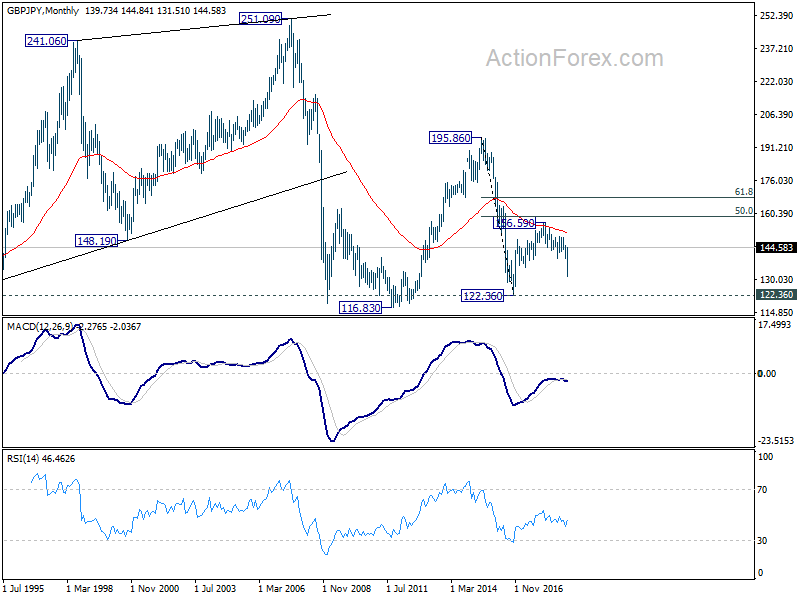

GBP/JPY Weekly Outlook

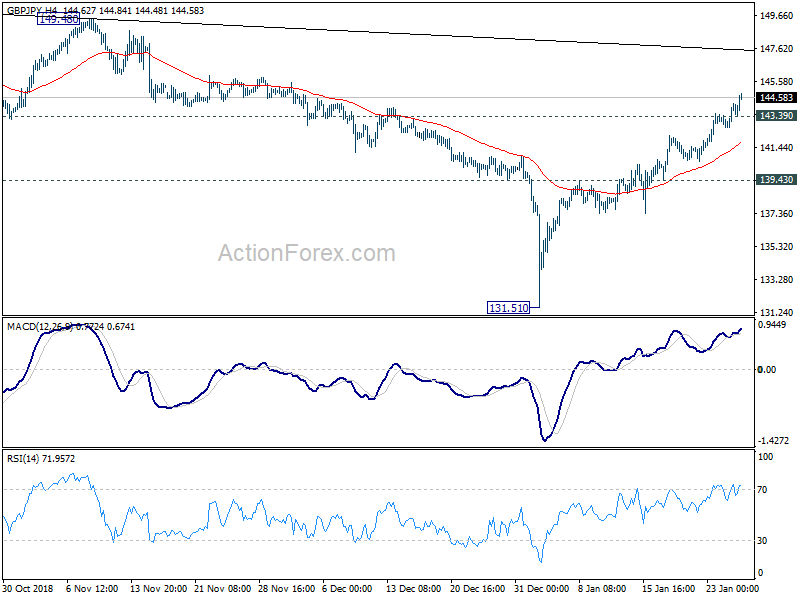

GBP/JPY’s rebound from 131.51 extended to as high as 144.84 last week and there is no sign of topping yet. Initial bias remains on the upside this week for trendline resistance at around 147.35. We’d expect strong resistance from there to limit upside at first attempt. On the downside, below 143.39 minor support will turn intraday bias neutral first and bring consolidations. But further rise will remain in favor as long as 139.43 resistance turned support holds.

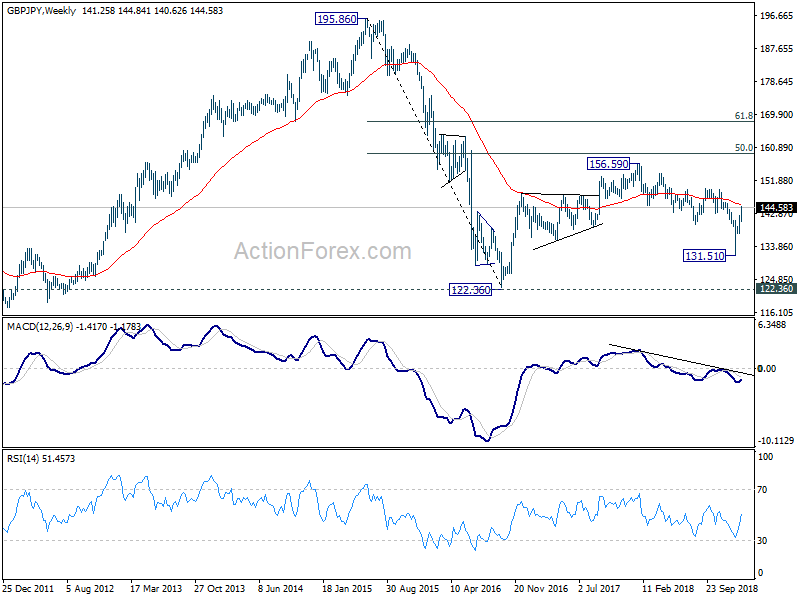

In the bigger picture, the strong rebound from 131.51 suggests that medium term fall from 156.59 (2018 high) has completed already. The corrective structure of such decline is turn argues that it’s the second leg of the corrective pattern from 122.36 (2016 low). And this pattern is starting the third leg. On the upside, decisive break of 149.38 will pave the way to 156.59 resistance and above.

In the longer term picture, the rise from 122.36 (2016 low) to 156.59 (2018 high) doesn’t display a clear impulsive structure. Thus, we’re treating price actions from 122.36 as a corrective pattern. In case of an extension, strong resistance is likely to be seen at 50% retracement of 195.86 (2015 high) to 122.36 at 159.11 to limit upside. On the downside, break of 131.51 support will bring 122.26 low back into focus.

{kind=link}