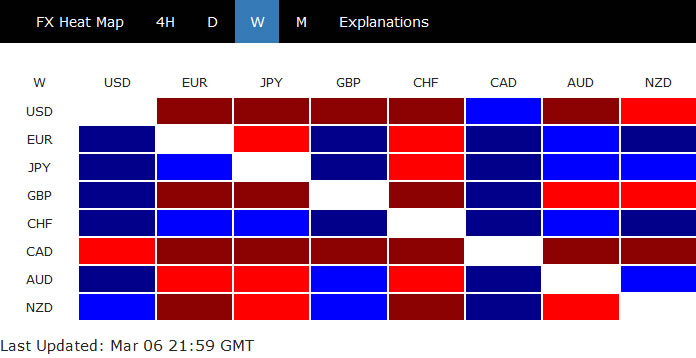

Global Wuhan coronavirus pandemic overshadowed all developments last week. Total confirmed cases broke 100k level (103,813 at the time of writing), with 3,522 deaths. Situation in China eased with daily new cases continued to drop. But there is no sign of slowing in South Korea (7,041 cases, 48 deaths) and Iran (5,823 cases, 145 deaths). Europe is very worrying with 4,636 cases and 197 deaths in Italy. Germany (717 cases), France (653, Spain (454) and Swiss (268 are catching up, while UK, Sweden, Norway, the Netherlands have all reported more than 100 cases.

Global stocks had a volatile week of consolidations. But eventually, Nikkei, FTSE, DAX and CAC broke to new lows. US indices were saved by the late rebound, partly also thanks to Fed’s -50bps panic rate cut. Dollar ended as the second weakest as 10-year and 30-year yield tumbled to new record lows on expectation of more Fed easing this month. But Canadian Dollar was even worse as WTI crude oil broke through key support at 42. Swiss Franc and Yen were the strongest on risk aversion and falling yields. Euro and Sterling were mixed with focus turns to this week’s ECB meeting, while BoE might follow Fed to deliver an inter-meeting cut.

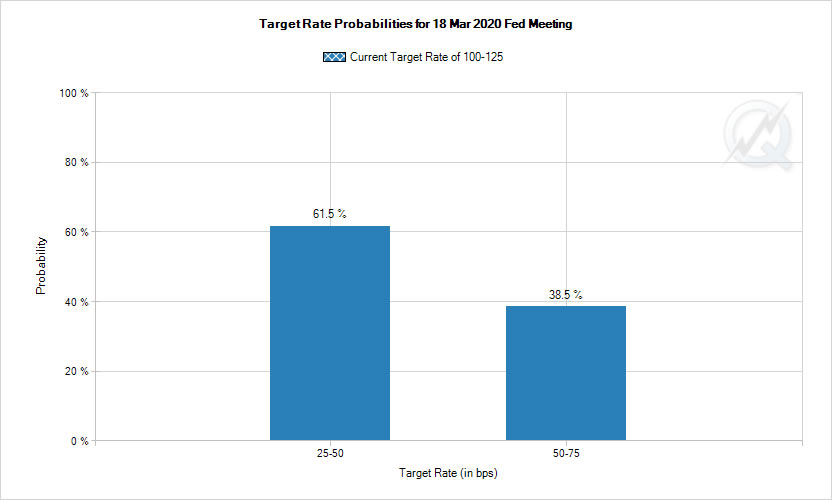

Markets seeing another -75bps cut by Fed, after the panic move

G7 finance ministers and central banks promised coordinate actions to counter the economic impact of coronavirus pandemic. RBA cut interest rate by 0.25% to 0.50% last week. BoC also lowered the benchmark rate by -50bps to 1.25%. Both were central banks delivered after regular scheduled meetings. The biggest surprise came from Fed, which announced an emergency rate cut of -50bps to 1.00-1.25%. The move as they came just two weeks ahead of the scheduled meeting on March 18. February economic data, in particular non-farm payrolls, were indeed rather solid. Stock markets were give little to no boost. Overall, Fed’s panic move seemed to have draw some criticism.

Further, there are questions on whether monetary policy easing is the right way to address the pandemic. It’s argued that fiscal measures are more effective in cushioning the supply shock from the outbreak. And more importantly health care measures should be given the highest priority to keep people safe first. To us, Taiwan has been doing exceptionally well in their coronavirus policies. It’s in the first batch of countries outside China which reported inflections. And even with its close tie with China, up till now, there are only 45 cases. There is no choke in the domestic economy neither. But then, for some reasons, Taiwan will never get the well deserved acknowledgement from WHO Director General Tedros Adhanom Ghebreyesus. Nor would Taiwan’s model be promoted to other countries by the WHO.

Anyway, investors are still hungry for more Fed rate cut despite last week’s move. Fed funds futures are pricing 100% chance of at least another -50bps rate cut on March 18, with 61.5% chance of -75bps cut. Such expectation was a key driving in pushing 10- and 30- year yield to record low, and a sharp selloff in Dollar against Euro and Yen. Nevertheless, the situation is still fluid and could change, in the next 10 days or so.

Dollar index confirmed major topping at 99.91 after steep selloff

Dollar index dived through 96.35 last week as selloff accelerated. The development now confirms major topping at 99.91. The decline could either be corrective the rise from 8.25 to 99.91, or as the third leg of the pattern from 103.82. In either case, based on current momentum, break of 38.2% retracement of 88.25 to 99.91 at 95.45 is likely. If happens, next target will be 61.8% retracement at 92.70.

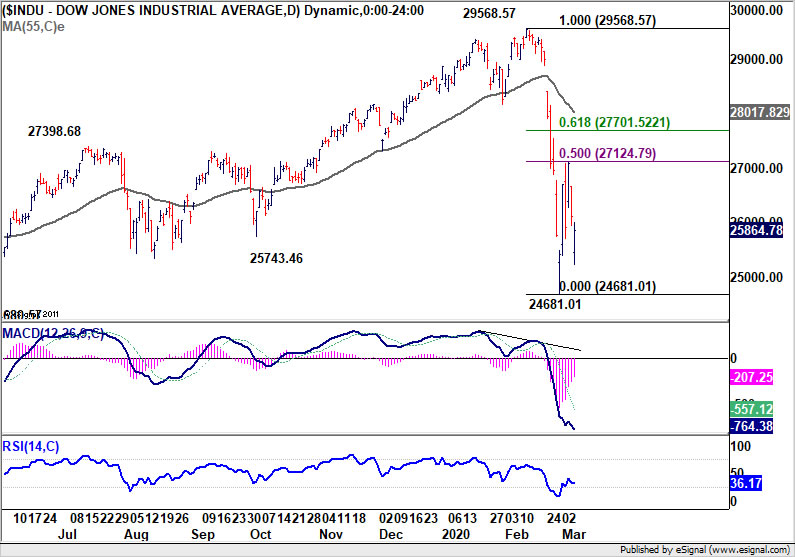

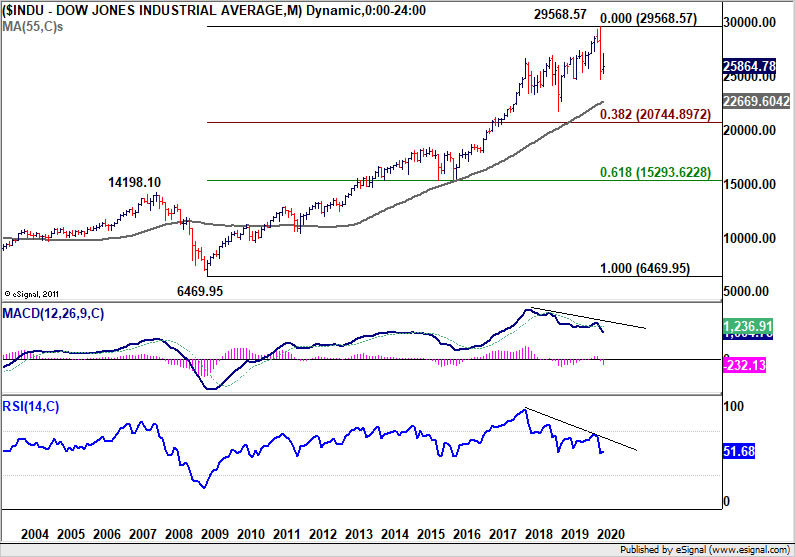

DOW to stay in range for very near term, but deeper decline expected later

DOW engaged in volatile sideway consolidation above 24681.01 last week, as rebound attempt was limited by 50% retracement of 29568.57 to 24681.01 at 27124.79. For the very near term, we’d expect more consolidative trading first. As long as 61.8% retracement at 27701.52 holds, we’d favor that case, that current fall is part of a long term correction. That is, it’s corrective whole rise from 6469.95 to 29568.57. Break of 2468.01 will target 55 month MACD at 22669.60 and possibly below.

Gold hit 7-year high, but hesitates to resume uptrend

Gold surged to new 7-year high of 1692.18 last week but failed to sustain above 1689.31 high so far. 1689.31 remains a key focus for the near term. Decisive break there will resume larger rally from 1160.17. Next target will be 100% projection of 1266.26 to 1557.04 from 1445.59 at 1736.37. However, break of 1631.83 minor support will turn bias to the downside to extend the consolidation from 1689.31 with another falling leg.

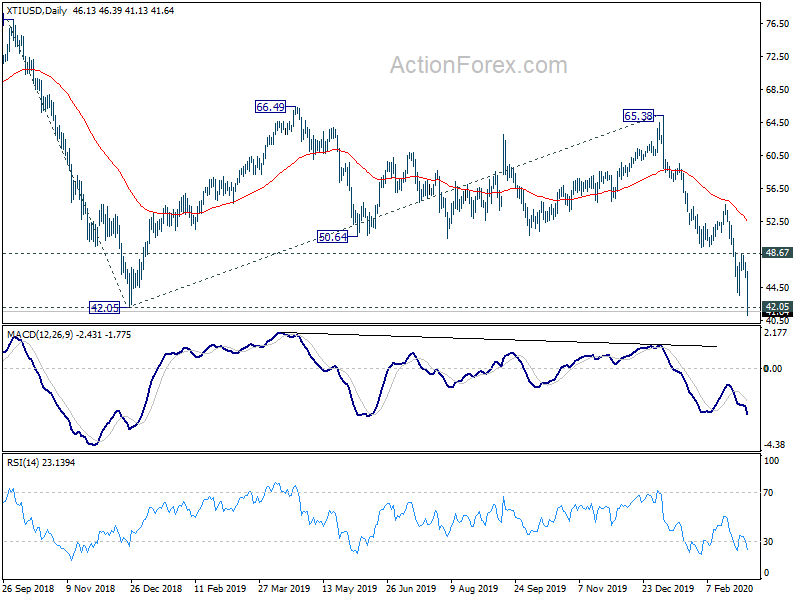

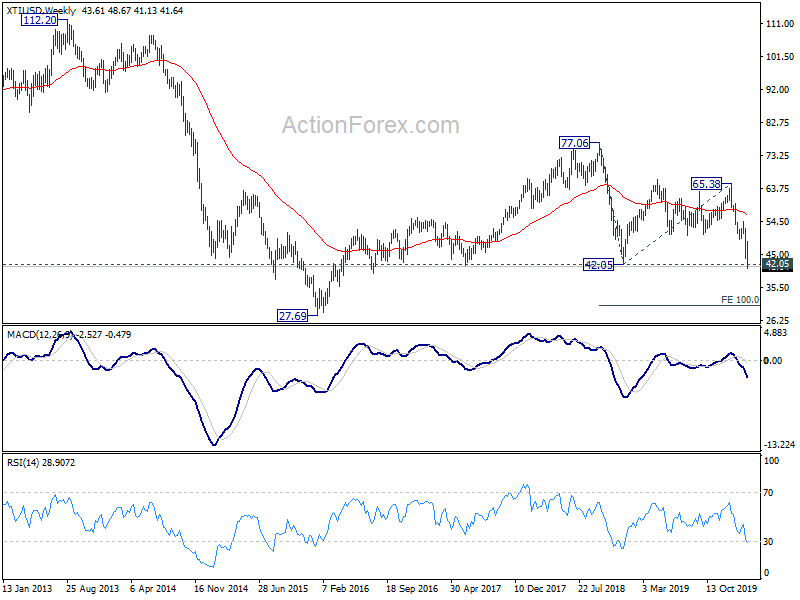

WTI crude oil broke 42.05 key support, resuming long term down trend

WTI crude oil dropped to as low as 41.13 last week and the break of 42.05 key support is unexpected to us. But in any case, near term outlook will stays bearish as long as 48.67 resistance holds. Sustained trading below 42.05 will confirm resumption of the down trend from 77.06 (2018 high). Next target will be 100% projection of 77.06 to 42.05 from 65.38 at 30.37.

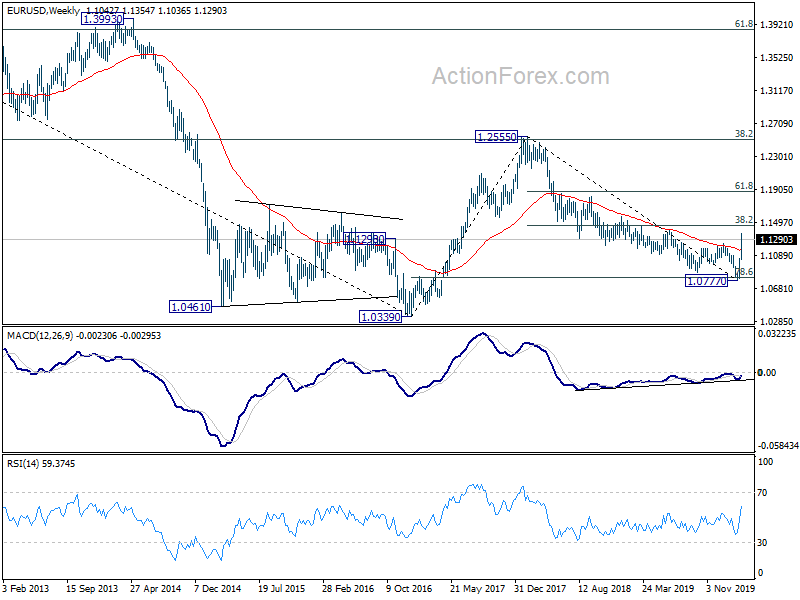

EUR/USD Weekly Outlook

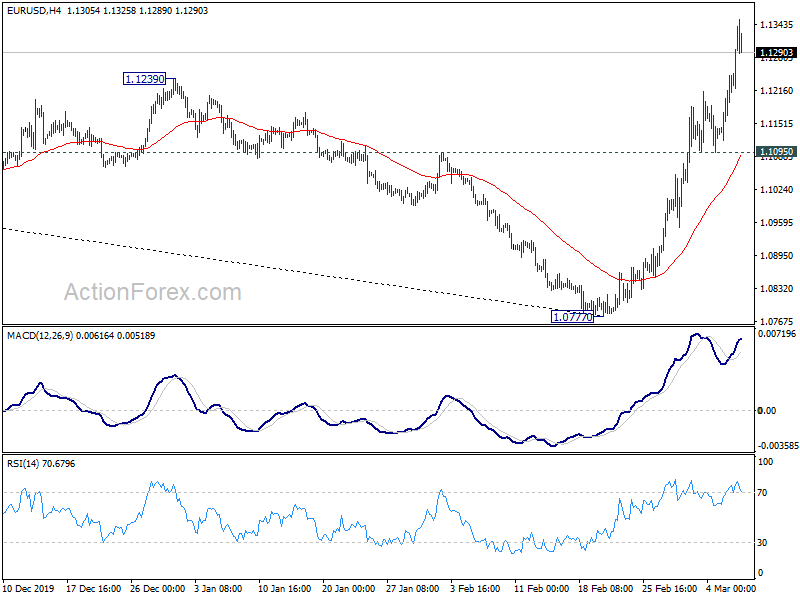

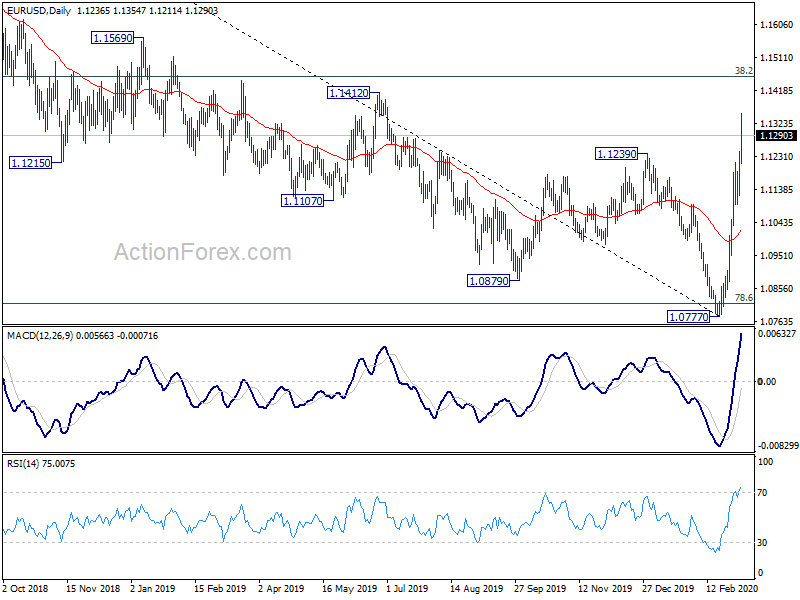

EUR/USD’s strong break of 1.1239 resistance last week confirmed medium term bottoming at 1.0777. Initial bias remains on the upside this week for 1.1456 fibonacci level. Reactions from there would reveal if its undergoing medium term bullish reversal. On the downside, break of 1.1095 minor support is needed to indicate short term topping. Otherwise, near term outlook will remain bullish in case of recovery.

In the bigger picture, a medium term bottom should have formed at 1.0777 after drawing support from 78.6% retracement of 1.0339 (2017 low) to 1.2555 at 1.0813. Sustained break of 38.2% retracement of 1.2555 to 1.0777 at 1.1456 will raise the chance of medium term bullish reversal and target 61.8% retracement at 1.1876. Rejection by 1.1456 will suggests that price actions from 1.0777 are merely a correction. Another fall below 1.0777 low would be seen at a later stage in this case.

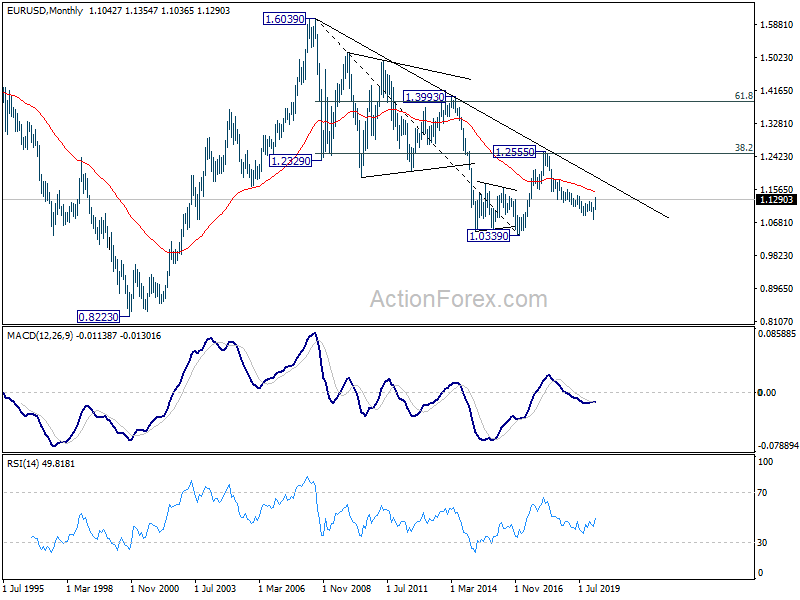

In the long term picture, outlook remains bearish for now. EUR/USD is held below decade long trend line that started from 1.6039 (2008 high). It was also rejected by 38.2% retracement of 1.6039 to 1.0339 at 1.2516 before. A break of 1.0039 low will remain in favor as long as 55 month EMA (now at 1.1512) holds.

{kind=link}