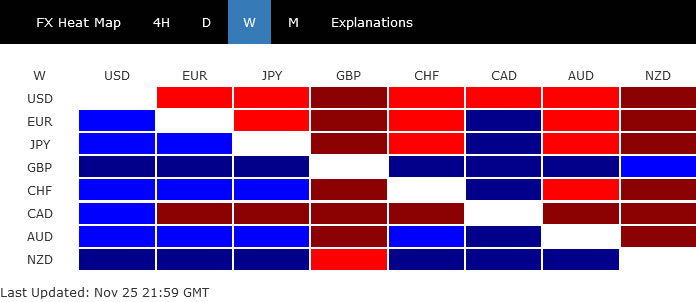

The expectations of a smaller Fed hike in December was affirmed by FOMC minutes last week. Dollar ended as the worst performer, following mild risk-on sentiment. Canadian Dollar was the second worst as dragged down by falling oil prices. Meanwhile, Euro was the third weakest suffering some selloff against Sterling.

Talking about the Pound, it’s the best performer last week. Kiwi was second, supported by RBNZ’s jumbo 75bps rate hike, followed by Aussie. The latter twos’ rally was somewhat capped by uncertainties over social unrest in China.

Fed expected to slow down in Dec, DOW extended rally

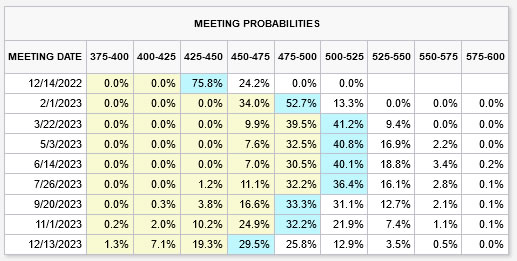

Market sentiment in the US was generally positive last week. Minutes of November FOMC meeting noted that “a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate”. The message reinforced the expectations that the next move on December 15 is a 50bps hike, with market now pricing in over 75% chance (around 25% chance for another 75bps hike).

As many global central bankers advised, the focus should be shifting to where the end point of the current tightening cycle is. According to fed fund futures, Fed might have the last rate hike in March with federal funds rate ending up at 5.00-5.25%. But that could be reshaped by the upcoming non-farm payroll data.

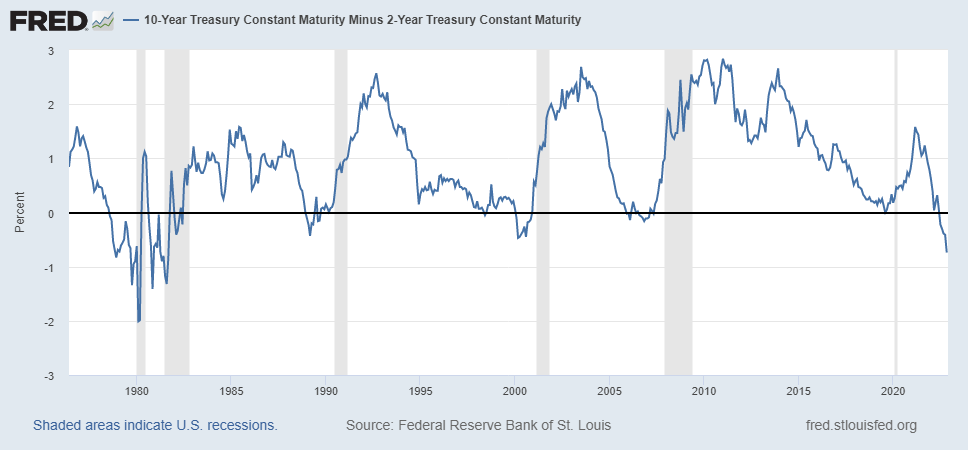

There are expectations that Fed would start to cut interest rate by the end of 2023, even if still too early to make a judgement on that. Inflation development is certainly a factor. The shape of the upcoming recession is for sure another one. It should be noted that the time and depth of yield curve inversion (2yr-10yr) is the worst since early 80s.

The persistence of DOW’s rally and the close above 34281.36 were a surprise. Considering overbought condition, there is still possibility of rejection by this resistance and break of 33239.75 support will bring pull back towards 55 day EMA (now at 32202.48). But sustained trading above 34281.36 will set the stage for retesting 36965.83 high in the early part of next year.

DXY had no rebound yet, but near term downside potential limited

Dollar index’s was knocked down towards the end of the week, but overall outlook is unchanged. A cluster of support level lies ahead, including 104.63, 38.2% retracement of 89.20 to 114.77 at 105.00, and 55 week EMA at 103.98. So near term downside potential should be limited, and a rebound could happen any time. Break of 107.99 resistance would bring further rise back towards 55 day EMA (now at 109.20).

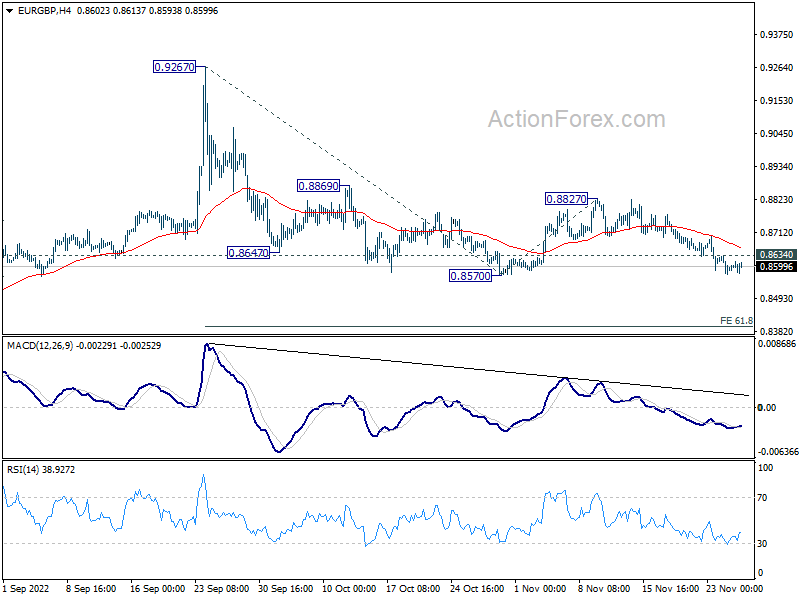

Underlying strength in Sterling not too convincing yet

Sterling ended as the strongest one for a couple of reasons. Firstly, political situation in the UK has pretty much stabilized after the new budget was well received by the markets earlier in the month. Secondly, the Supreme Court ruled out a unilateral Scottish independence referendum, removing a political uncertainty for the near term. Thirdly, the decline in oil price is seen as benefiting the UK more than other parts of Europe, for its deflationary effect. And Fourthly, while the Pound responds positively with risk-on sentiment together with Aussie and Kiwi, rallies in the latters were slightly capped by unrest and uncertainties in China.

Yet, the Pound still has a lot to prove. EUR/GBP will need to take out 0.8570 support in a decisive manner to confirm resumption of the fall from 0.9267. In that case, next target is 61.8% projection of 0.9267 to 0.8570 from 0.8827 at 0.8369. Or, break of 0.8634 minor resistance will delay the bearish case and bring recovery first.

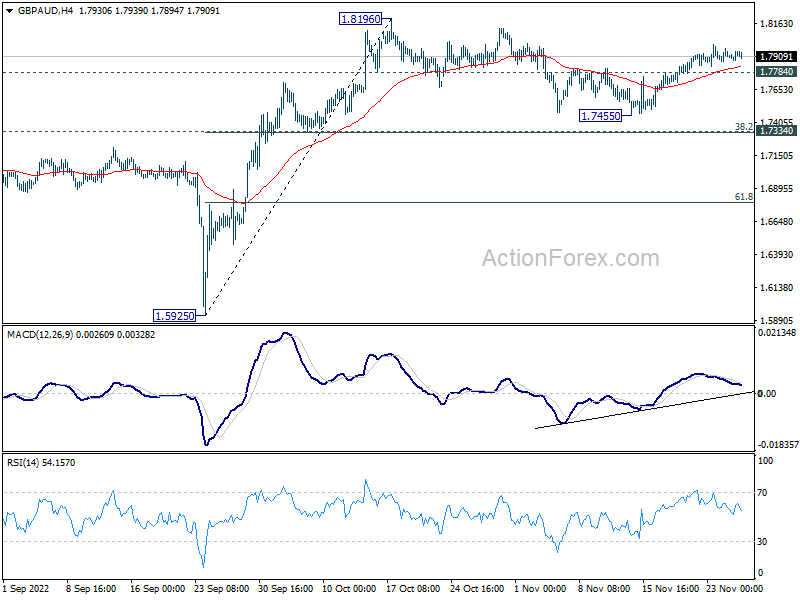

GBP/AUD’s corrective fall from 1.8196 should have completed at 1.7455. Yet, momentum of the rebound from there doesn’t warrant up trend resumption. Break of 1.7784 minor support will extend the corrective pattern with another decline back towards 1.7334 cluster support (38.2% rretracement of 1.5925 to 1.8196 at 1.7328). But of course, firm break of 1.8196 will confirm resumption of whole rally from 1.5925.

USD/JPY Weekly Outlook

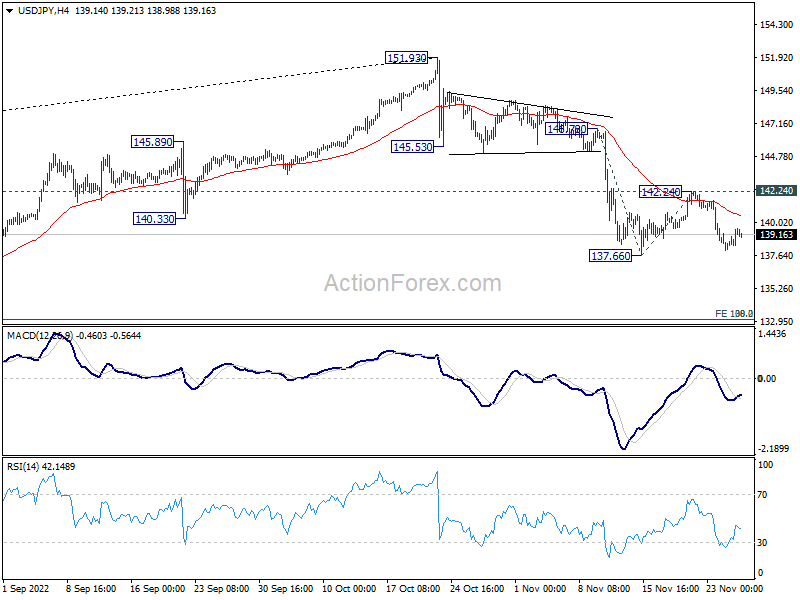

USD/JPY’s recovery ended at 142.24 after failing to sustain above 4 hour 55 EMA. But downside was contained above 137.66 support. Initial bias remains neutral this week first. Outlook stays bearish as long as 142.24 resistance holds. Break of 137.66 will resume the fall from 151.93 to 100% projection of 146.78 to 137.66 from 142.24 at 133.12, which is close to 133.07 medium term fibonacci level.

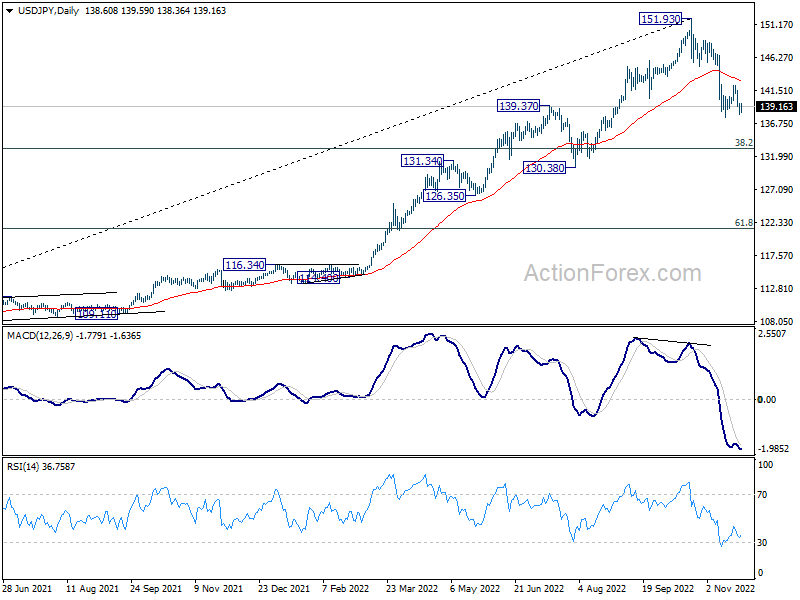

In the bigger picture, a medium term top should be formed at 151.93. Fall from there is correcting larger up trend from 102.58. It’s too early to call for bearish trend reversal. But even as a corrective move, such decline should target 38.2% retracement of 102.58 to 151.93 at 133.07, or further to 55 week EMA (now at 131.22).

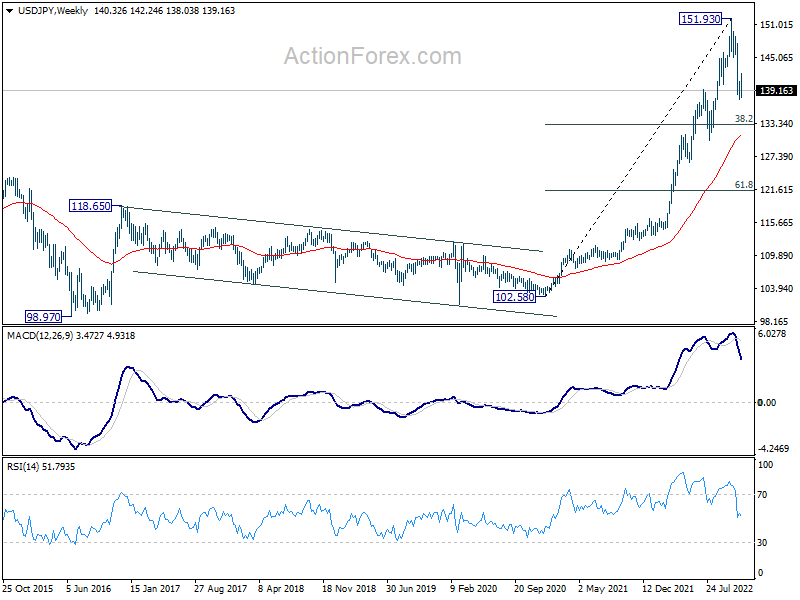

In the long term picture, rise from 102.58, as part of the up trend from 75.56 (2011 low) was put to a halt at 151.93, just ahead of 100% projection of 75.56 to 125.85 from 102.58 at 152.87. There is no clear sign of long term reversal yet. Such up trend is expected to resume at a later stage, as long as 125.85 resistance turned support holds.

{kind=link}