After some last minute dramas, UK Prime Minister Theresa May finally secured the backing from her Cabinet, on the Brexit draft agreement. As a more positive sign, there is no resignation of ministers so far. May said after a five-hour marathon meeting that “the collective decision of cabinet was that the government should agree the draft withdrawal agreement and the outline political declaration.” She added, “when you strip away the detail, the choice before us was clear: this deal, which delivers on the vote of the referendum, which brings back control of our money laws and borders, ends free movement, protects jobs security and our Union; or leave with no deal; or no Brexit at all.”

EU chief Brexit negotiator Michel Barnier hailed the UK for making a “decisive, crucial step” towards orderly Brexit. Referring to the draft, he said “this is a precise, detailed document… which provides legal certainty for everyone and on all the issues where we have to deal with the consequences of Brexit.” While it ” may be hard to guarantee an orderly withdrawal”, he pledged that UK will remain “our friend, our partner, and our ally.” Barnier had also passed his recommendation to EU27 leaders that “decisive progress” had been made for an extra EU summit, probably on November 25, to sign off.

EU’s statement here, with link to the withdrawal agreement.

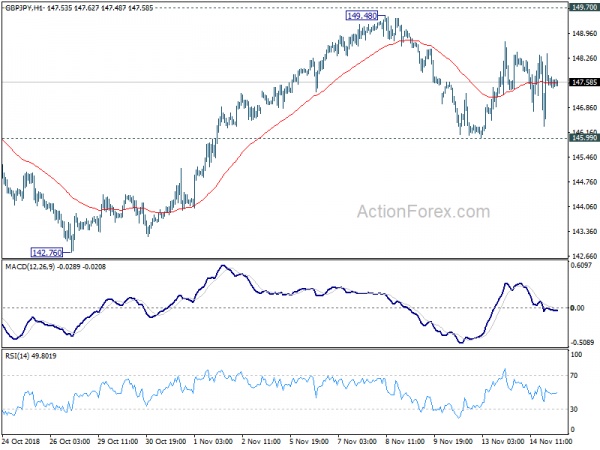

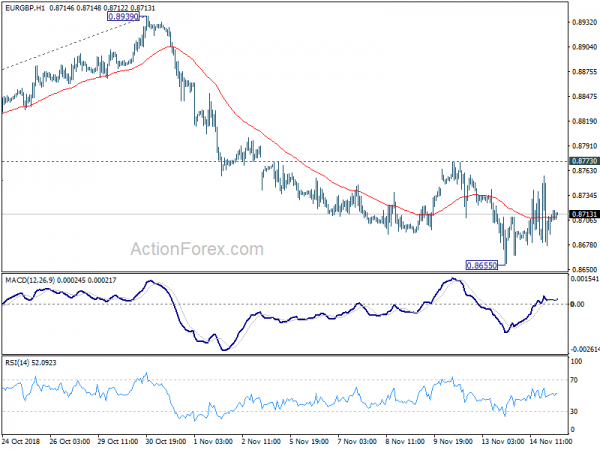

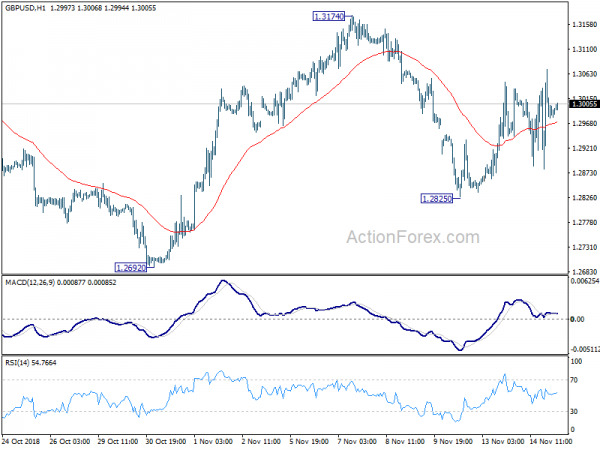

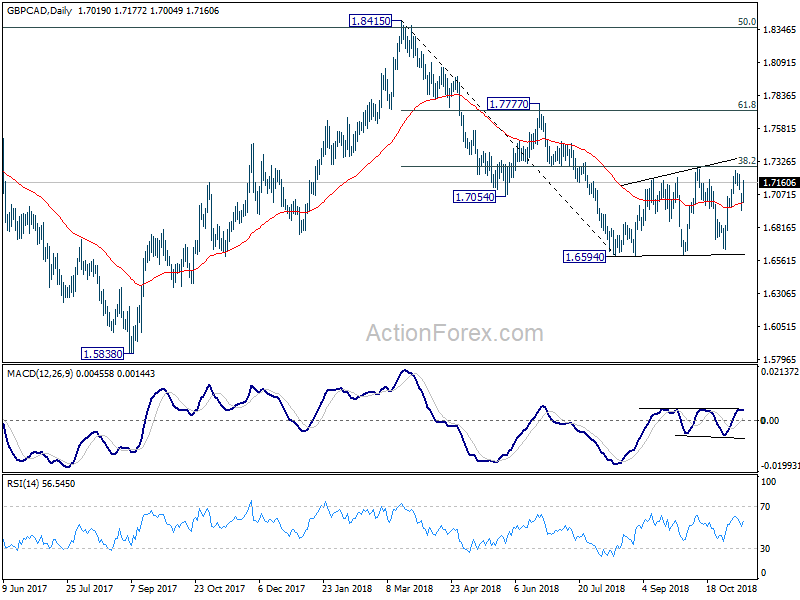

Sterling’s reactions to the development were volatile, yet muted. There were ups and downs in GBP/USD, GBP/JPY and EUR/GBP. But they’re after all, kept in familiar range.

May secured cabinet support for Brexit deal, Sterling reactions volatile yet muted

After some last minute dramas, UK Prime Minister Theresa May finally secured the backing from her Cabinet, on the Brexit draft agreement. As a more positive sign, there is no resignation of ministers so far. May said after a five-hour marathon meeting that “the collective decision of cabinet was that the government should agree the draft withdrawal agreement and the outline political declaration.” She added, “when you strip away the detail, the choice before us was clear: this deal, which delivers on the vote of the referendum, which brings back control of our money laws and borders, ends free movement, protects jobs security and our Union; or leave with no deal; or no Brexit at all.”

EU chief Brexit negotiator Michel Barnier hailed the UK for making a “decisive, crucial step” towards orderly Brexit. Referring to the draft, he said “this is a precise, detailed document… which provides legal certainty for everyone and on all the issues where we have to deal with the consequences of Brexit.” While it ” may be hard to guarantee an orderly withdrawal”, he pledged that UK will remain “our friend, our partner, and our ally.” Barnier had also passed his recommendation to EU27 leaders that “decisive progress” had been made for an extra EU summit, probably on November 25, to sign off.

EU’s statement here, with link to the withdrawal agreement.

Sterling’s reactions to the development were volatile, yet muted. There were ups and downs in GBP/USD, GBP/JPY and EUR/GBP. But they’re after all, kept in familiar range.