Live Comments

Japan Core CPI Picks Up to 1.6% in June, but Underlying Inflation Remains Contained

Japan's core consumer inflation accelerated in June, with the CPI excluding fresh food rising from 1.4% yoy to 1.6% yoy, matched expectations. Headline inflation also picked up from 1.5% yoy to 1.7% yoy. The figures point to firmer price pressures ahead of next week's Bank of Japan policy meeting, though both measures remained below the central bank's 2% target. Meanwhile, the core-core CPI, which strips out both fresh food and energy, eased from 1.8% yoy to 1.7% yoy, suggesting underlying inflation remained relatively contained despite the rebound in headline prices.

Food continued to be the main source of inflation. Prices excluding fresh food rose 3.1% from a year earlier, driven by higher raw material costs that lifted prices of processed foods such as bento meals and chocolates. By contrast, government subsidies aimed at cushioning households from higher fuel costs continued to suppress energy prices. Energy costs fell -0.1% yoy after declining -2.5% in May, with lower gasoline and electricity prices offsetting part of the upward pressure from global crude oil markets. Healthcare and household durable goods also contributed to the rise in consumer prices.

The June data are unlikely to alter expectations that the BoJ will keep its policy rate unchanged at next week's meeting after raising it to 1.00% in June. Instead, attention will center on the Bank's updated economic and inflation projections, particularly its assessment of the risks posed by rising oil prices and a weak Yen. With Brent crude at $100 and Japan heavily dependent on imported energy, today's inflation figures suggest the recent pickup in price growth has yet to fully reflect the potential impact of higher energy costs should government subsidies be scaled back or global oil prices continue climbing.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Headline CPI (Jun, y/y) | +1.7% | — | +1.5% |

| Core CPI ex-Fresh Food (Jun, y/y) | +1.6% | +1.6% | +1.4% |

| Core-Core CPI ex-Fresh Food & Energy (Jun, y/y) | +1.7% | — | +1.8% |

| Food ex-Fresh Food (Jun, y/y) | +3.1% | — | +3.5% |

| Energy Prices (Jun, y/y) | -0.1% | — | -2.5% |

| Gasoline Prices (Jun, y/y) | -0.7% | — | — |

| Electricity Prices (Jun, y/y) | -1.7% | — | — |

Key Takeaways

- Core inflation accelerated: CPI excluding fresh food rose from 1.4% to 1.6%, but stayed below BoJ's 2% target for a fifth consecutive month.

- Headline inflation also picked up: Headline CPI increased from 1.5% to 1.7%, reflecting firmer food and other consumer prices.

- Underlying inflation softened slightly: Core-core CPI eased from 1.8% to 1.7%, suggesting broader domestic price pressures have not reaccelerated.

- Food remained main driver: Food excluding fresh items rose 3.1%, though inflation slowed from 3.5%, as higher raw material costs continued to lift processed-food prices.

- Energy subsidies limited upside: Energy prices fell only 0.1%, narrowing sharply from May's 2.5% decline, but government support still restrained gasoline and electricity costs.

- Oil and Yen create upside risks: Brent near $100 and weak Yen could raise imported inflation later, particularly if government subsidies are reduced.

- BoJ likely to pause: Data should not alter expectations for rates to stay at 1.00% next week after June's hike.

- Outlook Report matters more: Markets will focus on how BoJ incorporates Middle East supply disruptions, higher oil and Yen weakness into new inflation forecasts.

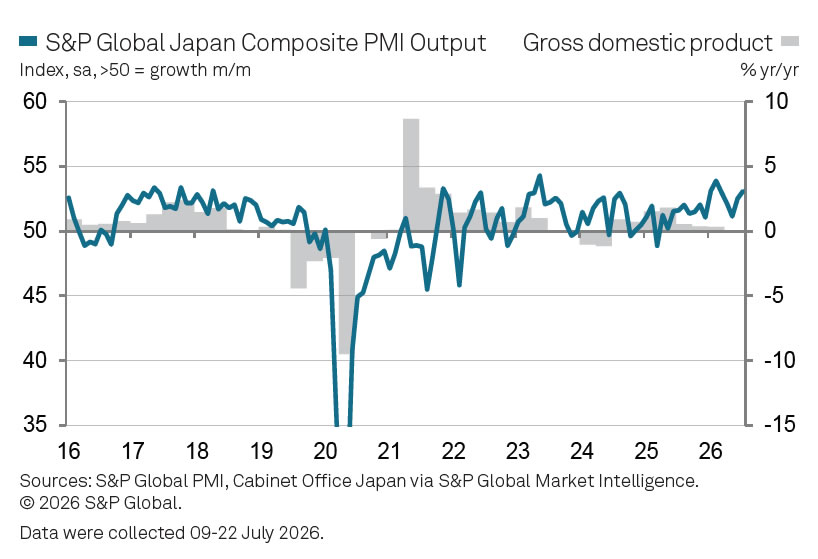

Japan PMI Composite rises to 53.1 as AI Demand Boosts Manufacturing

Japan's private sector expanded at its fastest pace since February in July, with the S&P Global Flash Composite PMI Output Index edging up from 52.8 to 53.1. The survey marked a sixteenth consecutive month of expansion, reflecting resilient business activity at the start of the second half of the year. While the Manufacturing PMI eased marginally from 54.8 to 54.7, manufacturing output accelerated sharply, with the Output Index rising from 54.3 to 56.1. Meanwhile, services activity cooled modestly as the Services PMI Business Activity Index slipped from 52.2 to 51.9.

The latest survey pointed to an increasingly uneven recovery. Manufacturing continued to outperform, supported by robust demand from the semiconductor and artificial intelligence industries, while services lost some momentum. At the same time, geopolitical tensions in the Middle East continued to shape business conditions. Manufacturers reported building inventories of finished goods and raw materials to guard against supply chain disruptions and higher input costs linked to the conflict, even as overall cost inflation eased slightly from June.

Despite the stronger pace of activity, the outlook became more cautious. Firms remained able to pass higher costs on to customers, with services companies in particular reporting faster increases in selling prices as they sought to protect margins. However, business confidence weakened, especially in the services sector, reflecting uncertainty over the economic outlook and geopolitical risks.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Flash Composite PMI Output Index (Jul) | 53.1 | 52.8 |

| Flash Services PMI Business Activity Index (Jul) | 51.9 | 52.2 |

| Flash Manufacturing PMI (Jul) | 54.7 | 54.8 |

| Flash Manufacturing PMI Output Index (Jul) | 56.1 | 54.3 |

Key Takeaways

- Private sector expansion strengthened: Japan's Flash Composite PMI Output Index edged up from 52.8 to 53.1, marking the strongest pace of growth since February and extending the expansion streak to 16 consecutive months.

- Manufacturing led the improvement: Although the headline Manufacturing PMI eased slightly from 54.8 to 54.7, the Manufacturing Output Index jumped from 54.3 to 56.1, signaling a sharp acceleration in factory production.

- Services lost some momentum: The Services PMI Business Activity Index slipped from 52.2 to 51.9, indicating that growth remained positive but moderated during July.

- Technology demand remained supportive: Manufacturers continued to benefit from robust demand linked to the semiconductor and AI industries, helping offset external headwinds.

- Middle East tensions continued to affect businesses: Firms reported building inventories of goods and raw materials amid supply chain disruptions and higher costs stemming from the regional conflict.

- Inflation pressures remained elevated: While input cost inflation eased slightly, selling prices continued to rise strongly, particularly in the services sector as firms sought to protect profit margins.

- Business confidence softened: Optimism about future output declined, especially among services firms, highlighting growing uncertainty despite solid current activity.

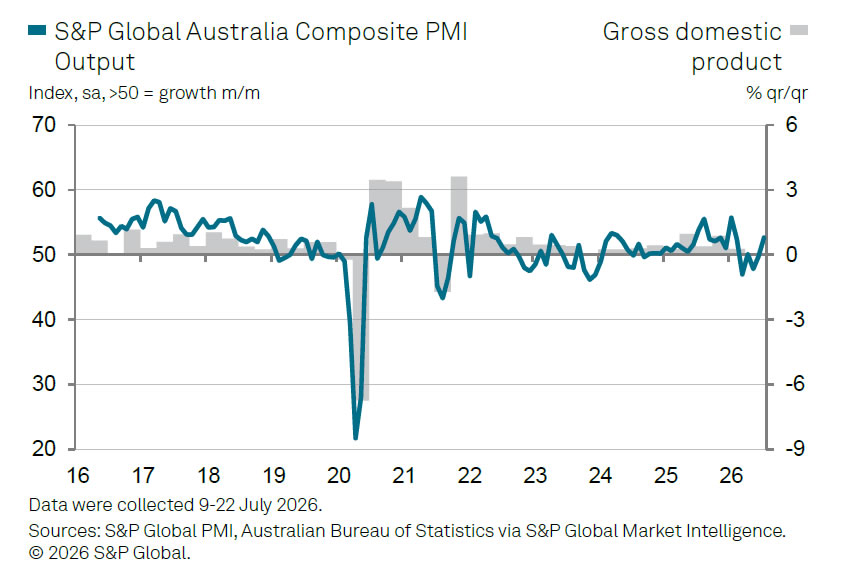

Australia PMI Composite Hits 2026 High at 52.6 as Domestic Demand Rebounds

Australia's private sector gained momentum in July, with the S&P Global Flash Composite PMI rising from 50.4 to 52.6, its highest reading since the start of the year. The improvement was driven primarily by the services sector, where the Services PMI Business Activity Index climbed from 50.5 to 53.0, while Manufacturing PMI edged up from 51.5 to 51.7. The data point to a firmer pace of economic expansion at the start of the third quarter, with overall business activity growing at a rate above the survey's long-run average.

A notable feature of the report was the improvement in demand. New orders increased for the first time in five months, indicating that domestic demand is beginning to recover despite continued weakness in overseas markets. While services remained the main engine of growth, manufacturing also showed signs of stabilizing. Factory output remained slightly below the expansion threshold at 49.9, but improved from June's 49.5, suggesting the sector's downturn is gradually easing rather than deepening.

The survey also offered encouraging news on inflation. Input cost pressures continued to moderate, providing further evidence that disinflation remains on track even as demand strengthens. At the same time, firms became more willing to protect profit margins as business conditions improved. Looking ahead, however, businesses remained cautious about the outlook, reflecting uncertainty surrounding the global economy and trade environment.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Flash Composite PMI Output Index (Jul) | 52.6 | 50.4 |

| Flash Services PMI Business Activity Index (Jul) | 53.0 | 50.5 |

| Flash Manufacturing PMI (Jul) | 51.7 | 51.5 |

| Flash Manufacturing PMI Output Index (Jul) | 49.9 | 49.5 |

Key Takeaways

- Private sector growth accelerated: Australia's Flash Composite PMI rose from 50.4 to 52.6, the strongest reading of 2026 and above the survey's long-run average, signaling a firmer pace of economic expansion.

- Services remained the growth engine: The Services PMI Business Activity Index climbed from 50.5 to 53.0, accounting for most of the improvement in overall business activity.

- Manufacturing continued to stabilize: The headline Manufacturing PMI edged up from 51.5 to 51.7, while the Manufacturing Output Index improved from 49.5 to 49.9, suggesting factory activity is nearing stabilization despite remaining slightly below the expansion threshold.

- Domestic demand improved: New orders increased for the first time in five months, indicating a recovery in domestic demand even as export sales weakened further.

- Disinflation trend continued: Businesses reported easing input cost pressures, providing further evidence that inflationary pressures are moderating despite stronger activity.

- Margin protection improved: More stable demand enabled firms to pass through costs more effectively and better protect profitability.

- Outlook remained cautious: Despite stronger current conditions, businesses continued to express uncertainty about the year ahead, reflecting concerns over the global economic and trade environment.