Dollar surges broadly as markets are entering into US session. AUD is trading as the weakest. US treasury yield will be a focus today, on whether 10 year yield could stay above 3% level and challenge 3.035 high.

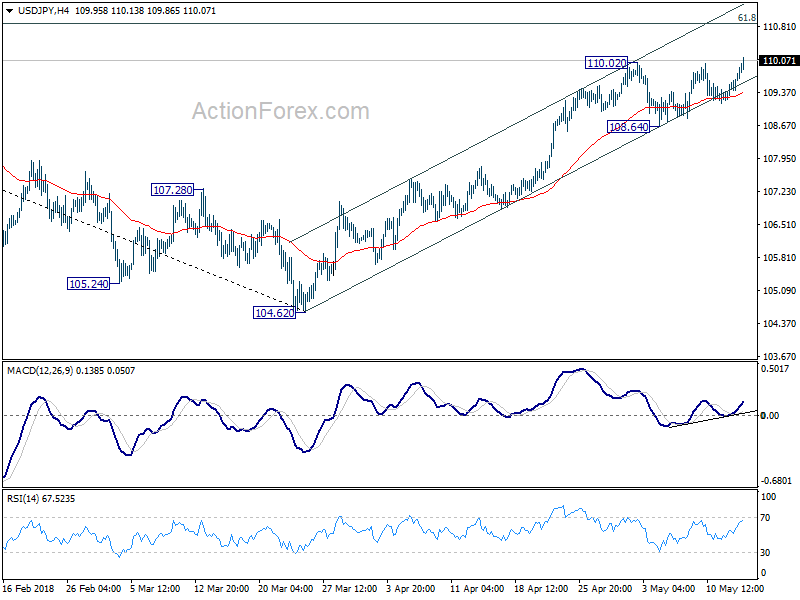

In particular, USD/JPY breaks through 110.02 resistance to resume recent rally from March low at 104.62. More importantly, it’s holding well within near term rising channel. Next target is 61.8% retracement of 114.73 to 104.62 at 110.86.

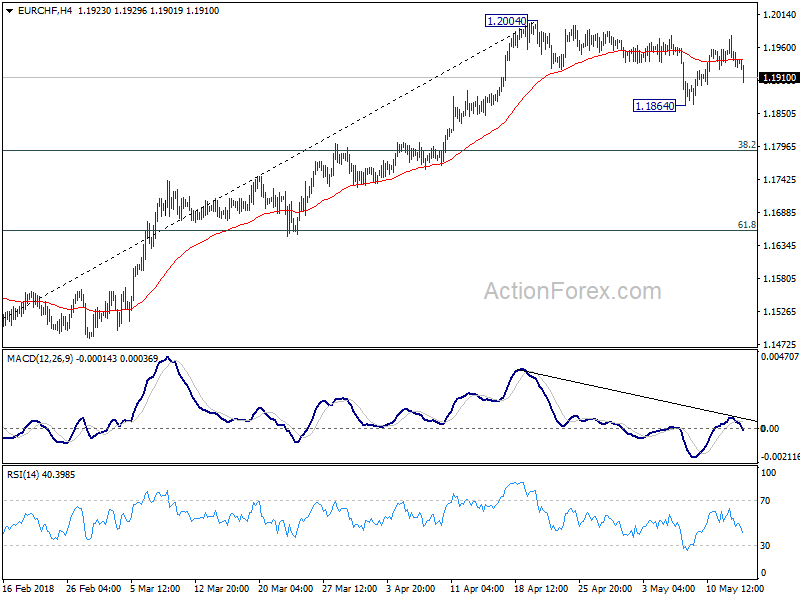

On development to watch is the sharp fall in EUR/CHF. The consolidation pattern from 1.2004 is set to extend with another falling leg, likely through 1.1864. That could give EUR extra pressure against USD, JPY and GBP.

USD ignores retail sales, surges as 10 year yield hit highest since 2011

US retail sales rose 0.3% mom in April, in line with expectation. Ex-auto sales rose 0.3% mom, below expectation of 0.5% mom.

Empire state manufacturing index rose to 20.1, up from 15.8 and beat expectation of 15.0.

Dollar pays little attention to the data release. Instead, it’s following treasury yields higher. 10 year yield reaches as high as 3.045 so far. It has now breached key resistance of 2013 high at 3.036, hitting highest since 2011.