The SNB is tightening its monetary policy further and is raising the SNB policy rate by 0.75 percentage points to 0.5%. In doing so, it is countering the renewed rise in inflationary pressure and the spread of inflation to goods and services that have so far been less affected. It cannot be ruled out that further increases in the SNB policy rate will be necessary to ensure price stability over the medium term. To provide appropriate monetary conditions, the SNB is also willing to be active in the foreign exchange market as necessary.

The SNB policy rate change applies from tomorrow, 23 September 2022. Moreover, the SNB is adjusting the implementation of its monetary policy to the positive interest rate environment. This ensures that the secured short-term Swiss franc money market rates remain close to the SNB policy rate. Banks’ sight deposits held at the SNB are remunerated at the SNB policy rate up to a certain threshold. Sight deposits above this threshold are remunerated at an interest rate of zero percent. The SNB will also use liquidity-absorbing measures.

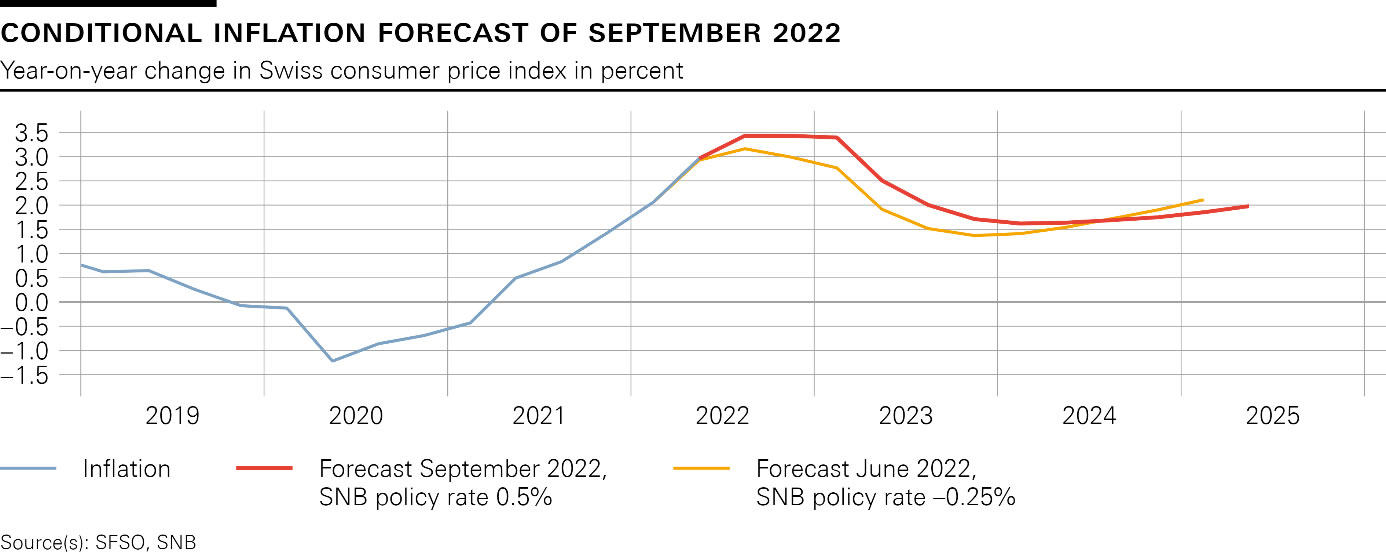

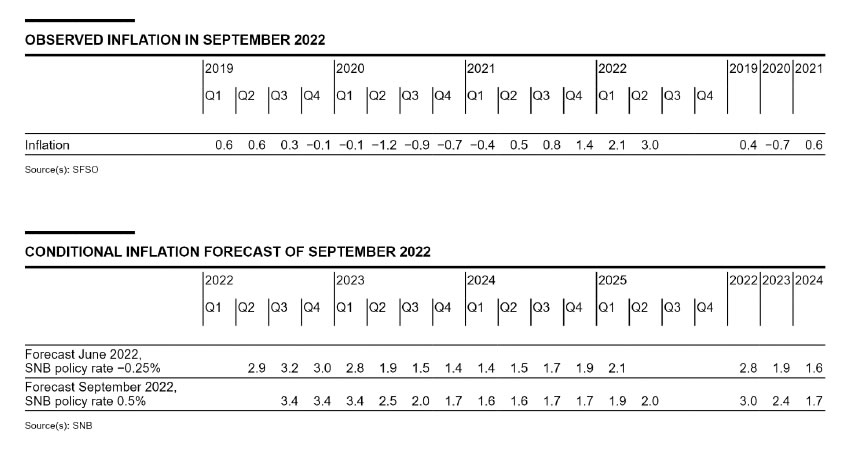

Inflation rose to 3.5% in August and is likely to remain at an elevated level for the time being. The latest rise in inflation is principally due to higher prices for goods, especially energy and food. The SNB’s new conditional inflation forecast is based on the assumption that the SNB policy rate is 0.5% over the entire forecast horizon (cf. chart 1). Up to mid-2024, the forecast is above that of June. After that, it is lower due to the now tighter monetary policy. At the end of the forecast horizon, inflation stands at 2%. The new forecast puts average annual inflation at 3% for 2022, 2.4% for 2023 and 1.7% for 2024 (cf. table 1). Without today’s SNB policy rate increase, the inflation forecast would be significantly higher.

Global economic growth has slowed considerably in recent months. At the same time, inflation in many countries is markedly above central banks’ targets. In response, numerous central banks have further tightened their monetary policy.

In its baseline scenario for the global economy, the SNB expects only weak economic growth. In particular, the energy situation in Europe, the loss of purchasing power due to inflation, and tighter financing conditions are having a dampening effect. Inflation will remain elevated for the time being. However, the importance of temporary factors such as supply bottlenecks is likely to diminish over the medium term. The increasingly tighter monetary policy in many countries should also help inflation gradually return to more moderate levels.

This scenario for the global economy is subject to significant risks. For example, the energy situation could worsen again. At the same time, high inflation could become embedded and require stronger monetary policy responses abroad. Finally, the course of the coronavirus pandemic remains an important source of risk.

In Switzerland, GDP growth in the second quarter was lower than expected, at 1.1%. This was mainly due to weaker performance in manufacturing. The short-term outlook has deteriorated. By contrast, the situation on the labour market has remained positive.

The further development of the economy is likely to be shaped by the economic slowdown abroad and the availability of energy in Switzerland. To date, the prices of natural gas and electricity in particular have risen sharply.

For this year, the SNB anticipates GDP growth of around 2%. This is roughly half a percentage point lower than at the last monetary policy assessment. The level of uncertainty associated with the forecast remains high. The biggest risks are a global economic downturn, a worsening of the gas shortage in Europe and a power shortage in Switzerland. Furthermore, a resurgence of the coronavirus pandemic cannot be ruled out.

Both mortgage lending and prices for single-family houses and privately owned apartments have continued to rise in recent quarters, while the latest data show signs of a slowdown in the residential investment property segment. The SNB will continue to monitor developments on the mortgage and real estate markets closely.

{kind=link}