Here are the latest developments in global markets:

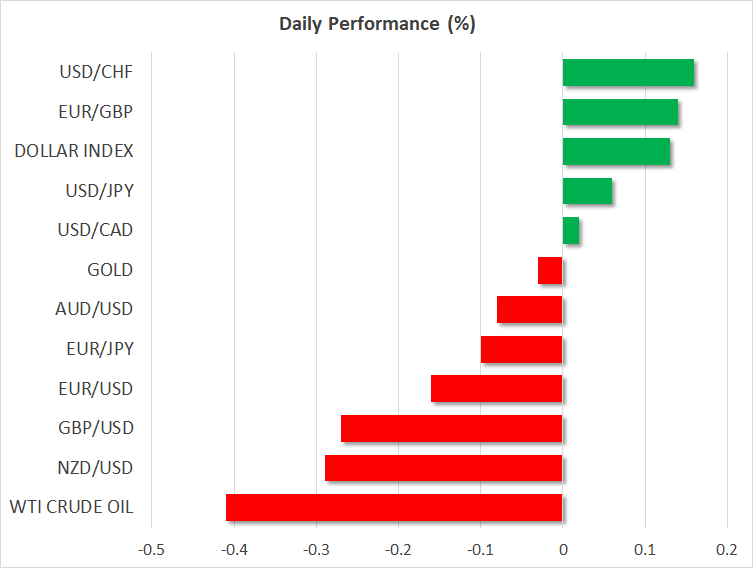

FOREX: The US dollar index is roughly 0.1% higher on Thursday, extending its gains from the previous session and trading just below an eleven-month high. Meanwhile, both the euro and sterling are on the defensive. The kiwi came under renewed selling interest after the RBNZ kept the option of a rate cut on the table.

STOCKS: US markets closed lower on Wednesday, giving back earlier gains. The drop came after White House economic advisor Kudlow said the Trump administration’s latest announcement on China was not an indication the US will soften its stance on trade, keeping investors on edge. The Nasdaq Composite was hit the hardest (-1.54%), while the S&P 500 (-0.86%) and the Dow Jones (-0.68%) also took a beating. Futures tracking the Dow, S&P, and Nasdaq 100 are currently flashing green though, pointing to a slightly higher open today. The negative sentiment rolled over into Asia as well, with Japan’s Nikkei 225 and Topix falling by 0.01% and 0.26% respectively. In Hong Kong, the Hang Seng dropped by 0.51%. Europe looks set to follow suit, as futures tracking all the major indices suggest a notably lower open today.

COMMODITIES: Oil prices are a little lower on Thursday, giving back some of the significant gains they posted in the previous session, when WTI touched a fresh three-and-a-half year high. Most of the gains came after the weekly EIA inventory data showed a much larger crude drawdown than expected. Prices surged even despite a stronger dollar, which typically weighs on the dollar-denominated liquid. In precious metals, gold is marginally lower today, extending its losses from Wednesday. The yellow metal is now trading at a fresh low for the year, at $1249/troy ounce. Given the insensitivity it has displayed towards trade frictions lately, its continued plunge appears to be primarily a function of a strengthening dollar more than anything else.

Major movers: Kudlow frightens equities, but dollar rises; kiwi drops after RBNZ

US stock markets went for a rollercoaster ride on Wednesday. They raced higher initially, after the Trump administration confirmed it will take what many have deemed as a less-confrontational route towards curbing Chinese investments in high-tech US companies. Officials said they will use a review process to assess whether foreign investments in “critical technology” pose national security risks, with Treasury Secretary Mnuchin saying the changes will not target China specifically.

However, the narrative that the US was seeking de-escalation soon got turned on its head, after White House economic advisor Larry Kudlow said the announced plan was not an indication of a softening stance towards China. Stocks quickly gave back all their gains to trade much lower in the aftermath.

The dollar, meanwhile, surged throughout the day, remaining largely unfazed by the trade narrative. The dollar index is slightly higher on Thursday as well, trading just below an eleven-month high reached earlier in June. Not even a sizeable drop in longer-term US Treasury yields was enough to halt the greenback’s advance, which may have been at least partly fueled by quarter-end demand.

The other factor potentially driving flows into the dollar was broad weakness in the euro and sterling. With little in the way of news flow, it seems the looming EU summit today is casting a shadow on the euro. German Chancellor Merkel’s coalition government could face collapse should she return home without a deal on immigration, potentially sending Europe’s largest economy to early elections.

Similarly, considering the summit will also touch on Brexit – where negotiations are still stuck on the Irish border issue – investors may have taken a defensive stance towards the pound. Some comments from BoE Governor Mark Carney yesterday that global risks are rising probably didn’t do the currency any favors either. Cable is down almost 0.3% today too, touching a fresh seven-month low.

Elsewhere, kiwi/dollar is down 0.3% today – trading at new two-year lows – after the RBNZ kept its policy unchanged overnight, but adopted an even more dovish tone. Officials said they are well positioned to manage a change in the cash rate either up or down, keeping the prospect of another rate cut on the table amid disappointing GDP growth and global trade tensions.

Day ahead: Eurozone business surveys, German inflation and US GDP due; EU summit gets underway; trade headlines still of interest

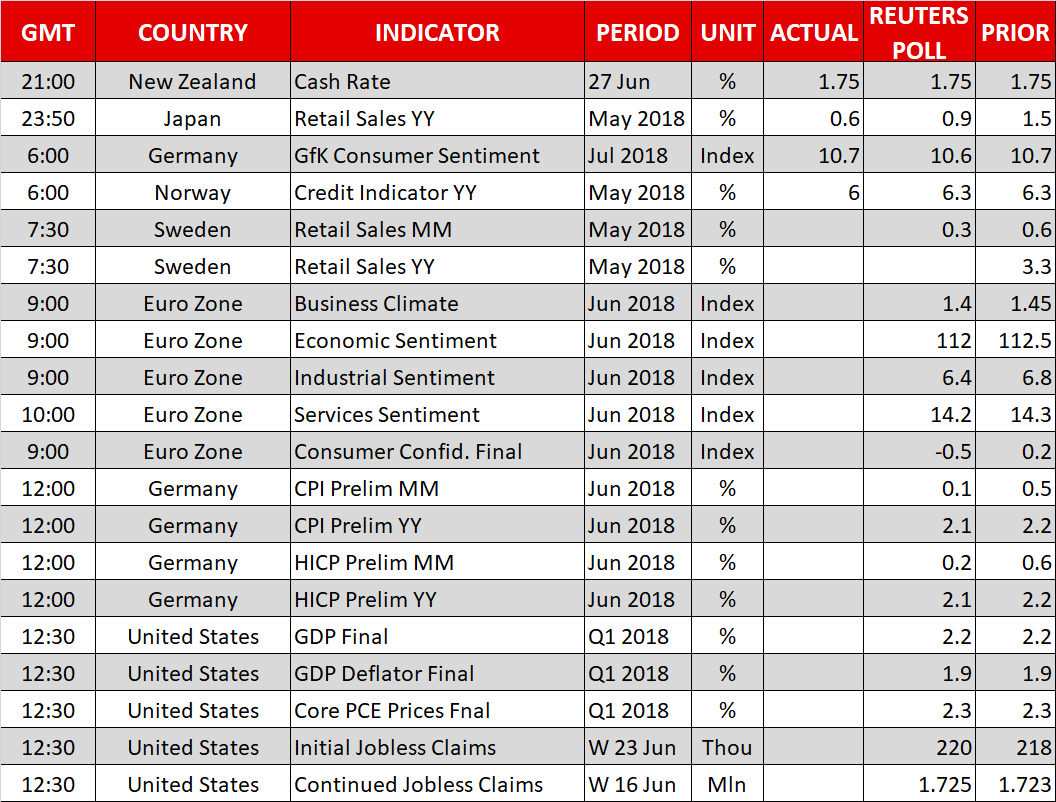

Thursday’s calendar features numerous business surveys out of the eurozone, inflation figures out of Germany, as well as updated GDP estimates for Q1 out of the US. Meanwhile, a European Council Summit commencing later on the day will also be of interest, as it could prove crucial for German Chancellor Angela Merkel’s coalition government. Any headlines on the state of global trade are also likely to prove market moving.

Krona pairs will be in focus at 0730 GMT, as Sweden will be seeing the release of retail sales figures for May.

At 0900 GMT, the European Commission’s Directorate General for Economic and Financial Affairs will be releasing numerous surveys gauging business morale, all of which are expected to reflect a worsening of sentiment during June relative to May. June’s final consumer confidence reading, again released by the same authority, will also be made public at the same time, with the relevant index anticipated at -0.5, its lowest since October 2017.

Germany, the eurozone’s and Europe’s largest economy, will be seeing the release of June flash inflation figures at 1200 GMT. CPI growth is projected to slow down to 0.1% m/m (from 0.5% in May) and 2.1% y/y (from 2.2% in May). The Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, will also be of interest. These numbers come one day before the eurozone sees its own preliminary inflation figures hitting the markets, and are also important in the sense that they may give an indication regarding tomorrow’s release.

Final estimates for Q1 GDP growth in the US are expected to confirm growth standing at 2.2% on an annualized basis during the quarter. The numbers are due alongside the final releases on Q1’s GDP deflator and core PCE price data at 1230 GMT. Weekly jobless claims numbers are also due at the same time.

EU leaders will be gathering in Brussels for a summit to touch on issues including migration, security & defense, and economic and financial affairs. Brexit will also be discussed, though that’s likely to come to the fore during tomorrow’s talks.

There are rising concerns over the sustainability of German Chancellor Merkel’s coalition government, with political instability in the country likely to act as a drag on the euro. Specifically, the Christian Social Union (CSU) party, Merkel’s Bavarian ally, has threatened to clash with her unless the party’s demands on reducing the country’s immigration burden are satisfied. Merkel will likely attempt today to get concessions from her European counterparts that would allow her coalition to continue ruling Europe’s largest economy. EU Summit Chairman Donald Tusk and European Commission President Jean-Claude Juncker will be holding a press conference after the first working session of the meeting at 1700 GMT.

Andy Haldane, the BoE policymaker who surprised markets last week by voting in favor of rate hike, will be talking at 1330 GMT. Regional Fed Presidents James Bullard (1445 GMT – non-voting FOMC member in 2018) and Raphael Bostic (1600 GMT – voter) are also scheduled to make appearances today.

Lastly, trade developments remain in the background. On Wednesday, the US adopted a softer stance of some sorts against China, providing some relief to markets. Still, mixed signals are projected by the Trump administration and a re-escalation of tensions is not to be ruled out.

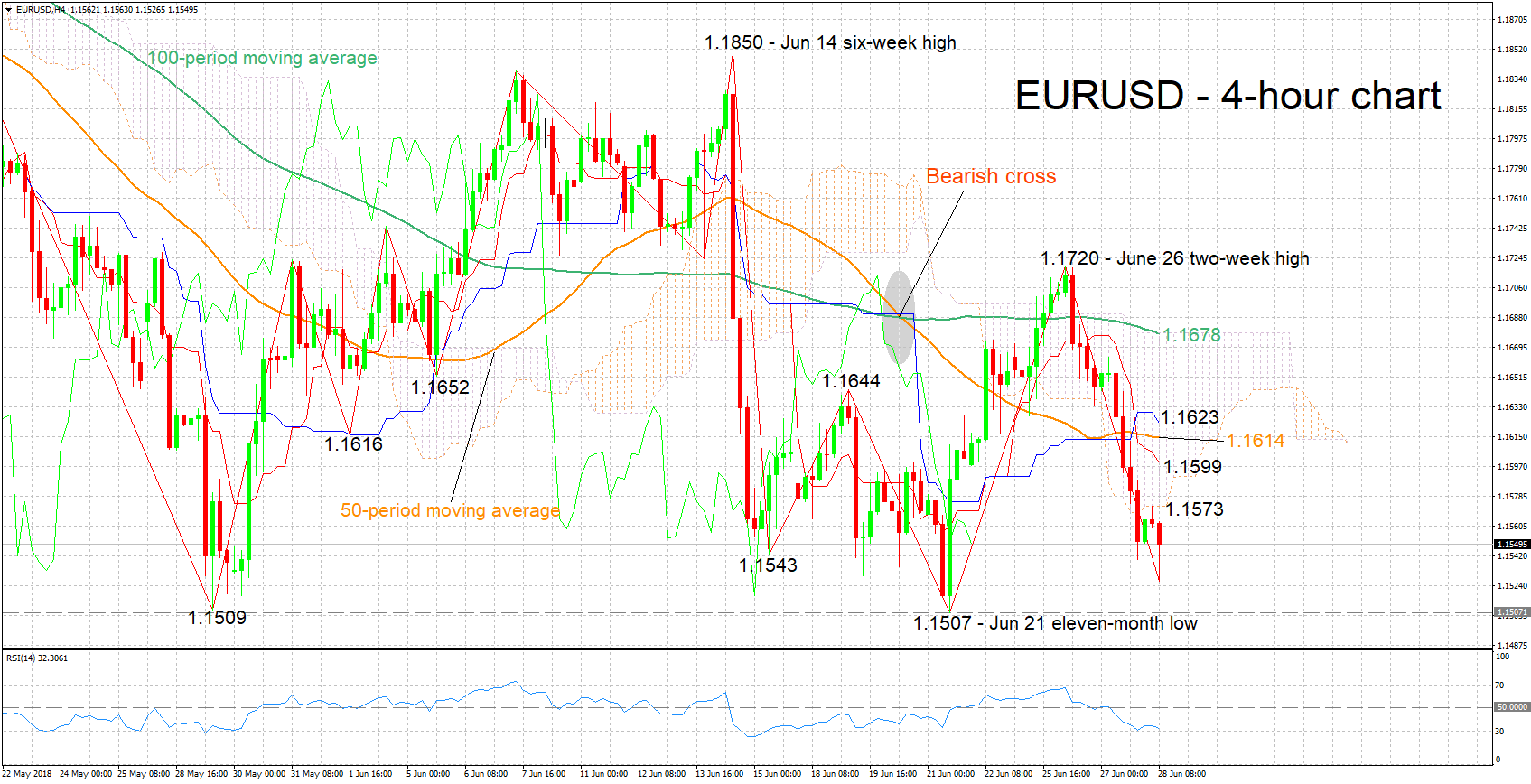

Technical Analysis: EURUSD bearish in the short-term

EURUSD has declined by more than 150 pips after reaching a two-week high of 1.1720 on Tuesday. Earlier on Thursday, it recorded a one-week low of 1.1527. The negatively aligned Tenkan- and Kijun-sen lines are projecting a bearish picture. The RSI is also pointing towards negative momentum. Notice though as well that the indicator is close to the 30 oversold level.

An EU Summit outcome that is seen as undermining Merkel’s government will likely exert downward pressure on the pair. Support to declines could come around last week’s 11-month low of 1.1507, including the 1.15 round figure, with steeper losses increasingly bringing into scope the 1.14 handle.

Anything seen as strengthening Merkel’s position on the other hand might allow EURUSD to advance. Resistance to advances may be met around the Ichimoku cloud bottom at 1.1573, and further above from the area around the current level of the Tenkan-sen at 1.1599; the region around the latter includes the 1.16 handle, the current level of the 50-period MA (1.1614) and the Kijun-sen (1.1623).

Eurozone and US releases due later today can also spur some positioning in EURUSD.