Here are the latest developments in global markets:

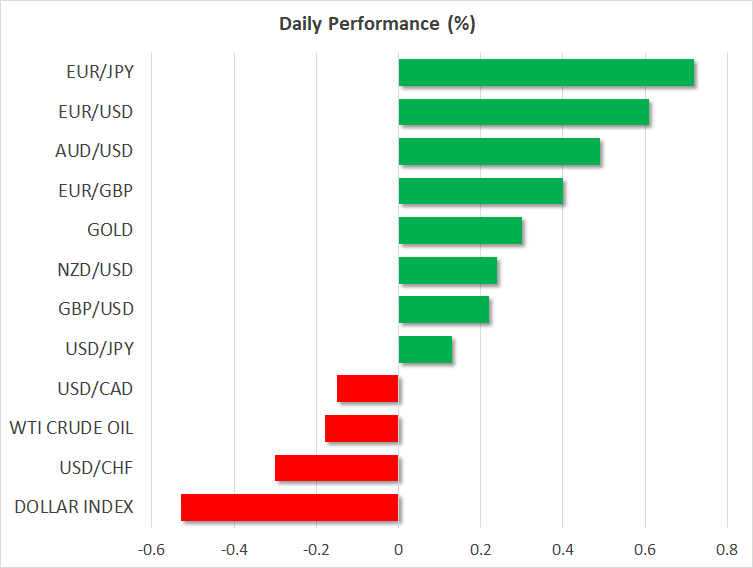

FOREX: The US dollar index is down by 0.5% on Friday, as the currency with the biggest weight in that index – the euro – is advancing after EU leaders reached a deal on immigration overnight, dispelling some political uncertainty. The safe-haven Japanese yen is on the retreat, as the positive tones from the EU summit and the lack of any concerning trade news boosted risk appetite.

STOCKS: US markets closed in the green on Thursday in the absence of a fresh escalation in trade tensions, with technology and financial shares leading the way higher. The tech-heavy Nasdaq Composite advanced 0.79%, while the S&P 500 and the Dow Jones climbed by 0.62% and 0.41% respectively. The rebound looks set to continue, as futures tracking the Dow, S&P, and Nasdaq 100 are pointing to a significantly higher open today, something likely owed to the positive outcome of the EU summit. The bullish sentiment rolled over into Asia too, with Japan’s Nikkei 225 and Topix gaining 0.15% and 0.23% correspondingly. In Hong Kong, the Hang Seng surged by 1.58%. Europe was even more encouraging. Futures suggest all the major European indices are set to open more than 1.0% higher today.

COMMODITIES: Oil prices corrected lower on Friday, after posting notable gains in the previous session. WTI is down by 0.2%, after it touched a fresh three-and-a-half year high yesterday of $74.03, while Brent is 0.1% lower, trading just below a one-month high. Without any fresh news on the supply front, the gains appear to be owed mostly to the correction lower in the dollar, as well as the broader risk-on sentiment in markets. In precious metals, gold is up by 0.3% on Friday. It is currently trading near the $1250/troy ounce level, attempting to post its first day of advances this week amid a dip in the US dollar, which makes the dollar-denominated metal more attractive for investors using foreign currencies.

Major movers: Euro recovers, yen retreats as EU reaches migration deal; loonie rebounds too

After marathonlike talks that dragged on until the early hours of Friday, EU leaders finally reached an agreement on migration. They agreed to take more steps towards restricting the movement of asylum seekers between member states, and also to set up new centers that process migrants to determine whether they are genuine refugees or not. The accord strengthens the position of German Chancellor Merkel, who was under pressure to return home with a deal or face the potential collapse of her fragile coalition government.

The euro spiked higher on the news, recovering ground against all its major counterparts as the likelihood for early elections in Germany diminished and political uncertainty faded. Euro/dollar is up by 0.6% on Thursday, while euro/sterling is 0.4% higher, touching a fresh three-month high. Sterling will probably remain watchful of Brexit developments – remember the EU summit continues today and the leaders could highlight the lack of meaningful progress in those talks lately.

Euro/yen was the biggest winner, gaining 0.7% as the EU deal boosted risk appetite in general, diverting funds out of safe-haven assets like the yen and into high-yielding currencies like the Australian dollar. Besides the migrant deal, the yen seems to be on the defensive amid a lack of fresh escalation in the trade saga. In fact, China said overnight it will allow more foreign investment in its economy after July 28, in sectors such as banking and automotive, helping to ease concerns of further tensions. Dollar/yen is up by 0.1%, and looks set to post a green candle for the fourth consecutive session.

Elsewhere, rising oil prices breathed some life back into the Canadian dollar yesterday. The loonie surged as WTI crude prices touched fresh three-and-a-half year highs; recall Canada is a major oil-exporting economy. Besides oil, monetary policy will likely be a major driver for the currency in the coming days. The BoC meets again on July 11 and a rate hike is priced in with a 64% probability, according to Canada’s OIS. Should today’s GDP data and next week’s jobs figures confirm the economy continues to operate on all cylinders, markets could push that probability closer to 100% and the loonie may stay in demand – absent any worrisome NAFTA headlines, of course.

Day ahead: US core PCE index, personal income & consumption under the spotlight; EU CPI in focus as well

Friday’s economic calendar will keep investors busy in terms of key data releases, while trade developments may continue to dictate changes in risk sentiment.

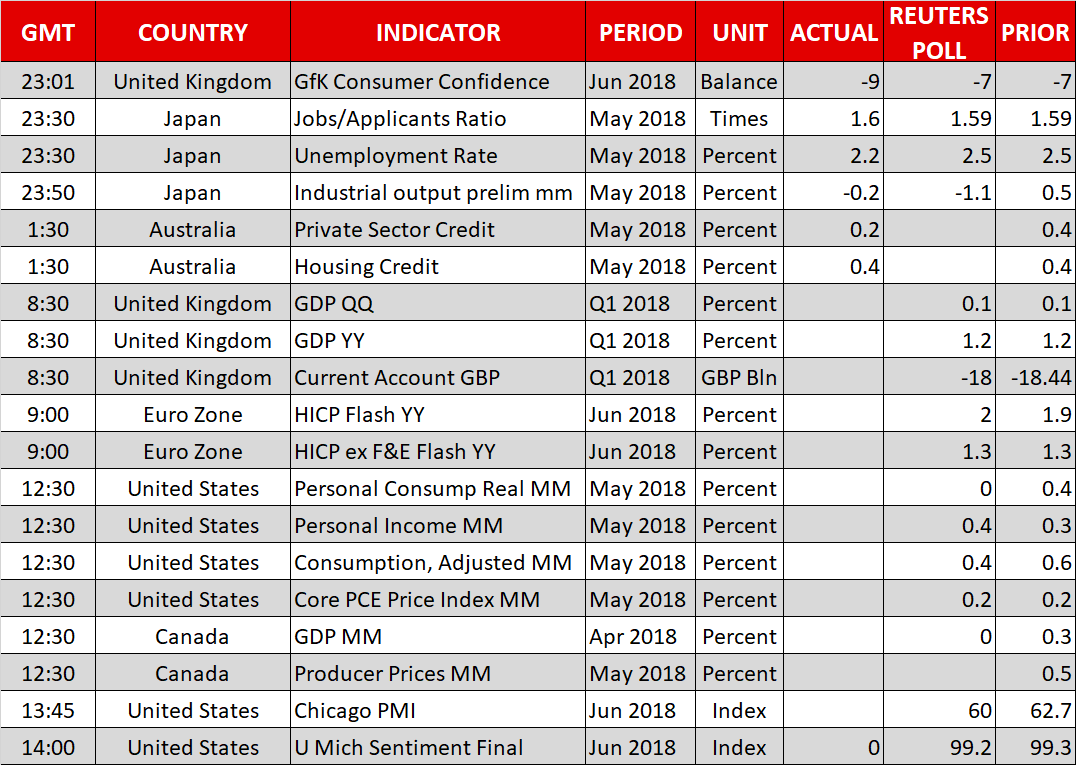

Out of the Eurozone, the German unemployment rate will come into view at 0800 GMT to show that the jobless rate remained unchanged at the record low of 5.2% in June according to analysts, with the number of unemployed people decreasing by 8k, less than the 11k reduction in May. Eurozone flash inflation readings for the aforementioned month, however, will be of greater interest as these could affect the ECB’s view on monetary policy and therefore bring greater volatility to the euro if the data deviate from expectations. Forecasters are now supporting that the headline CPI has inched up to 2.0% y/y in June compared to 1.9% in May, while the core equivalent which excludes food and energy is seen unchanged at 1.3% y/y. Should inflation data register a higher increase than expected, the euro could extend today’s rally on speculation ECB policymakers could feel more confident to raise interest rates after the termination of the asset purchasing program at the end of this year. Still, investors will likely continue to monitor the political situation in Germany despite EU leaders finding a solution to the migration puzzle at the EU summit today. Particularly, it would be interesting to see whether Merkel’s coalition partners, who oppose the Chancellor’s refugee policy, will raise their thumbs up, saving the coalition government and Merkel’s political career.

Meanwhile, in the UK, the Office for National Statistics will be publishing its final GDP growth estimates for the first quarter at 0830 GMT, with expectations being for an expansion of 1.2% y/y and 0.1% m/m as first and second estimates indicated. At 1230, Canada will also see its monthly GDP growth stats but no growth is expected to have been recorded in April. In March, Canadian GDP increased by 0.3% m/m.

In the US, all eyes will turn to the calendar at 1230 GMT when the Bureau of Economic analysis is scheduled to update the Fed’s favorite inflation measure, the core Personal Consumption Expenditure Index, as well as its personal income and personal consumption gauges. The report is projected to show that inflation has risen by 0.2% m/m in May, the same as in April, pushing the yearly gauge from 1.8% to 1.9%, just below the Fed’s inflation target of 2.0%. Investors, though, will look at the consumption and income figures to clarify whether higher interest rates and inflation are pressuring consumers. While consumption could have eased to 0.4% m/m from 0.6% seen previously, personal income is projected to edge up by 0.1 percentage points to 0.4% m/m. In case the numbers – especially the consumption gauge – beat expectations, amplifying the case for a more hawkish rate path by the Fed, then the dollar could attract additional buying interest.

A little bit later, Chicago PMI and University of Michigan Consumer Sentiment will come under review as well at 1345 and at 1400 GMT respectively.

In oil markets, Baker Hughes will report the number of active US oil drills at 1700 GMT.

As for today’s public appearances, the French President Emmanuel Macron, the Chairman of the EU summit Donald Tusk, and the head of the European Commission Jean-Claude Juncker will be giving a news conference after a two-day European leaders’ summit at 1130 GMT. Comments on Brexit and eurozone economic integration will be in focus.

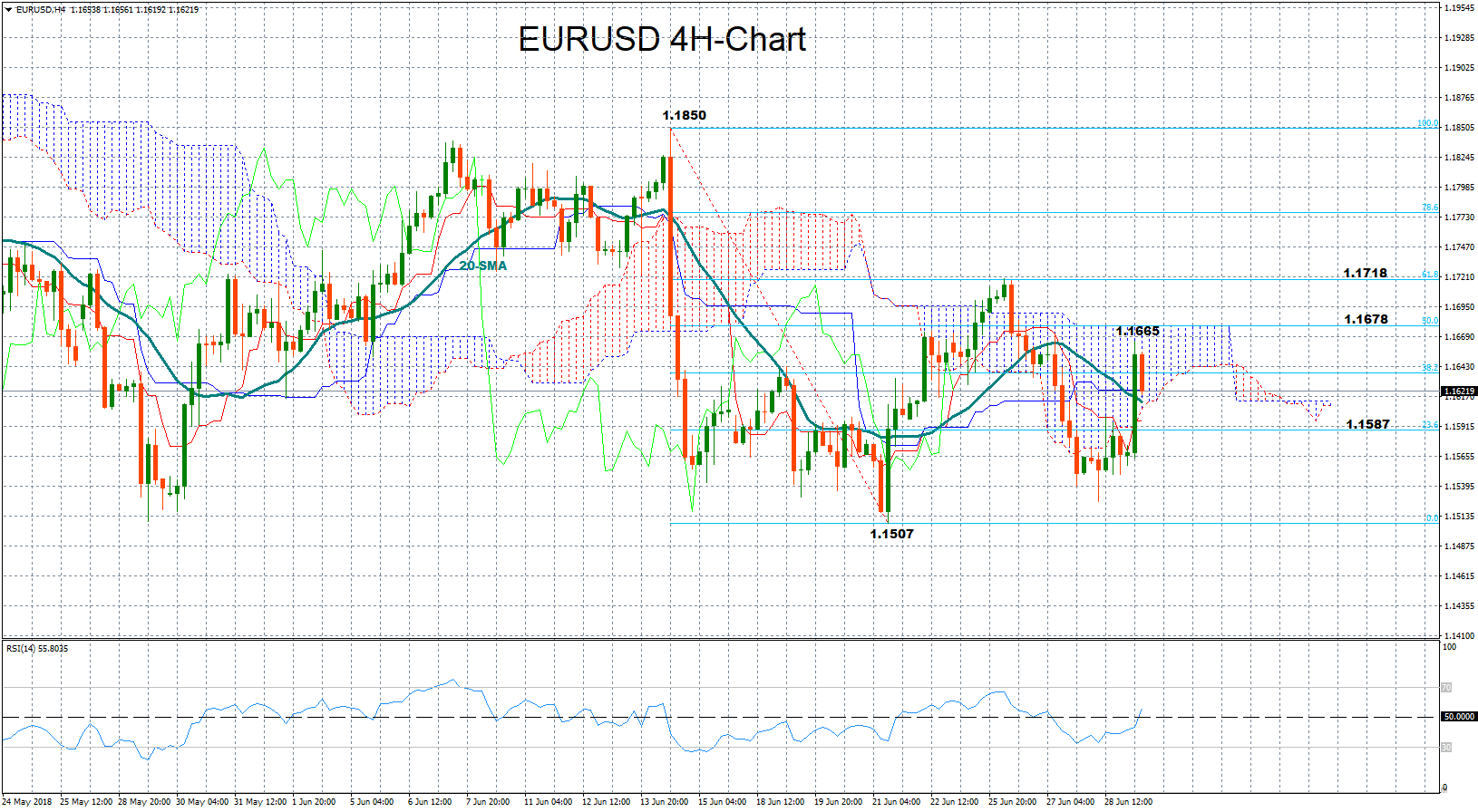

Technical Analysis: EURUSD breaks 1.1600 but momentum indicators are still neutral

The announcement of a migration deal in the Eurozone, woke up euro bulls early today, driving EURUSD above the 1.1600 level and back into the Ichimoku cloud in the four-hour chart. The Ichimoku indicators, however, continue to support that the pair is likely to trade neutral, maintaining the downtrend from 1.1719 as the red Tenkan-sen line has flattened below the blue Kijun-sen line. The RSI has improved further but is currently moving around its neutral threshold of 50, sending additional neutral signals at the moment.

Still, the pair could gain more ground today if Eurozone inflation figures surpass forecasts, with traders looking for resistance probably at today’s high of 1.1665 before eyes turn to 1.1678, the 50% Fibonacci retracement of the downleg from 1.1850 to 1.1507. A break of this point could then shift focus to the 61.8% Fibonacci retracement of 1.1718, where the market stopped upside corrections on Tuesday.

On the other hand, disappointing prints could immediately lead the market down to the 20-period moving average which currently stands at 1.1613 before steeper declines eye the 23.6% Fibonacci of 1.1587. The area around 1.1550, though, could be a stronger support since it has provided some floor to the market over the past two weeks.

{kind=link}