Here are the latest developments in global markets:

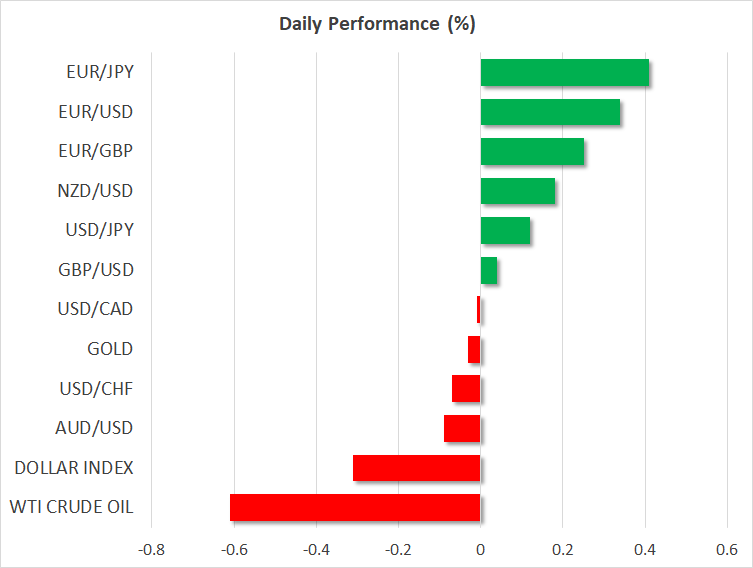

FOREX: The US dollar index is down by 0.3% on Thursday, ahead of the release of the minutes from the June FOMC meeting later today. Meanwhile, the euro is recovering ground following media reports that ECB officials think the market is underestimating the Bank’s rate-hike path.

STOCKS: US equity markets remained closed in celebration of the Independence Day public holiday yesterday. Futures suggest the S&P 500, Dow Jones, and Nasdaq 100, are set to open higher today, albeit not significantly so. In Asia, all indices were lower on Thursday, as the threat of the US-China trade standoff heating up further tomorrow cast a large shadow. In Japan, the Nikkei 225 and the Topix fell by 0.78% and 1.01% respectively, while in Hong Kong, the Hang Seng retreated by 1.04%. In Europe, futures tracking the major benchmarks were mixed, some pointing to a higher and some to a lower open today, though all were near neutral territory.

COMMODITIES: Oil prices corrected lower on Thursday, following a tweet from US President Trump demanding that OPEC lower oil prices. He said the cartel is driving prices higher even though the US defends many of its members without much payment, and that they must reduce prices immediately. WTI is down by 0.6% today, while Brent fell by approximately 0.8%. In precious metals, gold continued its tentative recovery yesterday, aided by a correction lower in the dollar, which makes the dollar-denominated metal more attractive for investors using foreign currencies. The safe-haven is practically flat on Thursday, currently hovering near the $1,255/troy ounce mark.

Major movers: Euro and sterling recover; trade narrative still front and center

The euro and the British pound enjoyed some demand on Wednesday, in an otherwise quiet trading session, with US markets closed for a public holiday.

The common European currency received a helping hand from media reports suggesting “some” ECB members believe markets are underestimating the Bank’s rate trajectory. Investors were previously fully pricing in a 10bps rate increase in December 2019, which these policymakers perceived as too dovish, instead indicating that a lift-off in rates may occur as early as September or October 2019. Following these hawkish signals, markets repriced that prospect, and now a 10bps hike is fully factored in for October next year.

Remarks from key ECB speakers today, including Executive Board members Praet and Mersch, could cast a fresh light on such expectations. Should they confirm that September-October is the most likely period for a hike, then a further bullish repricing of a September hike may be in order, potentially extending the euro’s recovery.

In the UK, the pound got a lift from a stronger-than-anticipated services PMI for June, with pound/dollar touching a 10-day high of 1.3245 before retreating slightly. Coming on top of similar upside surprises in the respective manufacturing and construction indices, the solid services print likely played into the narrative that the BoE remains on track to raise rates in August, something currently priced with a 57% probability (UK OIS). BoE Governor Mark Carney’s comments today will be closely watched. After Carney, and with no other tier-one data points on the UK calendar for a while, focus will likely turn back to Brexit, where PM May is soon expected to unveil a White Paper that could determine whether the negotiations will move forward, or not.

On the trade front, a German newspaper reported yesterday the US ambassador to Germany told car industry leaders that the US is willing to find a compromise with the EU to avoid tariffs on European car imports. While stocks of car manufacturers like Daimler (+3.21%) jumped, this had little effect on broader market sentiment. In general, all eyes remain on the US-China tariffs that are expected to be enacted tomorrow. Markets are jittery a US implementation of the announced tariffs will lead to retaliation from China, which could provoke even further measures from the US, thus dragging the two into a more serious standoff.

Day ahead: Fed minutes eyed; ADP employment report and ISM services PMI due; tariff “deadline” looms

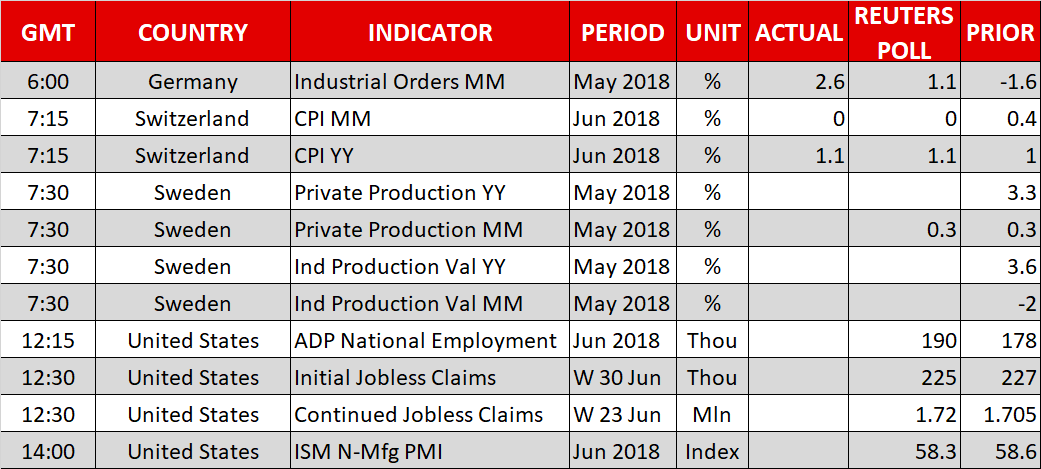

Notable releases out of Thursday’s calendar are the ADP jobs report and the ISM’s services PMI out of the US. The Fed minutes pertaining to the central bank’s latest meeting are also due and may end up attracting most attention in terms of releases.

Data on private sector production and industrial production will be made public out of Sweden at 0730 GMT, bringing krona pairs to the fore.

The ADP’s national employment report on the number of positions added to the US economy by the private sector is due at 1215 GMT. The addition of 190k positions is projected during June, up from 178k in May. This report is considered by some as a preamble to the nonfarm payrolls report (due on Friday) which covers both the private and public sectors, though it should be stressed that the correlation between the two releases has fallen recently.

Out of the US at 1230 GMT are weekly jobless claims data, while the ISM’s non-manufacturing (services) PMI for June is slated for release at 1400 GMT. The index is anticipated to slightly ease relative to May, though to still remain comfortably in expansion territory above 50.

The Fed minutes relating to the US central bank’s June meeting are due at 1800 GMT. FOMC policymakers increased interest rates for a second time this year at that gathering, while they also revised upwards their rate-path projections to signal a total of four hikes in 2018, from three before. The projection for four rate increases in total during the year was a close call though, and the minutes may offer additional insights on how confident FOMC members are for such a prospect. Any comments on global trade and how frictions may affect the US economy will also be generating interest.

Policymakers making appearances include ECB chief economist Peter Praet (0830 GMT), BoE Governor Mark Carney (0945 GMT) and ECB executive board member Yves Mersch (1115 GMT).

A meeting between German Chancellor Angela Merkel and Hungarian Prime Minister Viktor Orban at 1100 GMT might be of interest, given their differences over immigration policy. Merkel will also be holding talks with UK PM Theresa May in Berlin – at 1200 GMT – which are expected to address the relatively slow progress in Brexit negotiations so far. Meanwhile, US Secretary of State Mike Pompeo is in North Korea for meetings with Kim Jong-un.

In energy markets, EIA data on crude oil inventories due at 1500 GMT will be attracting oil traders’ interest. Crude stocks are forecast to have declined by around 3.5 million barrels during the week ending June 29, after falling by around 9.9m in the previously tracked week.

Lastly, trade deliberations will also be in focus one day before US tariffs on $34 billion of Chinese imported goods take effect.

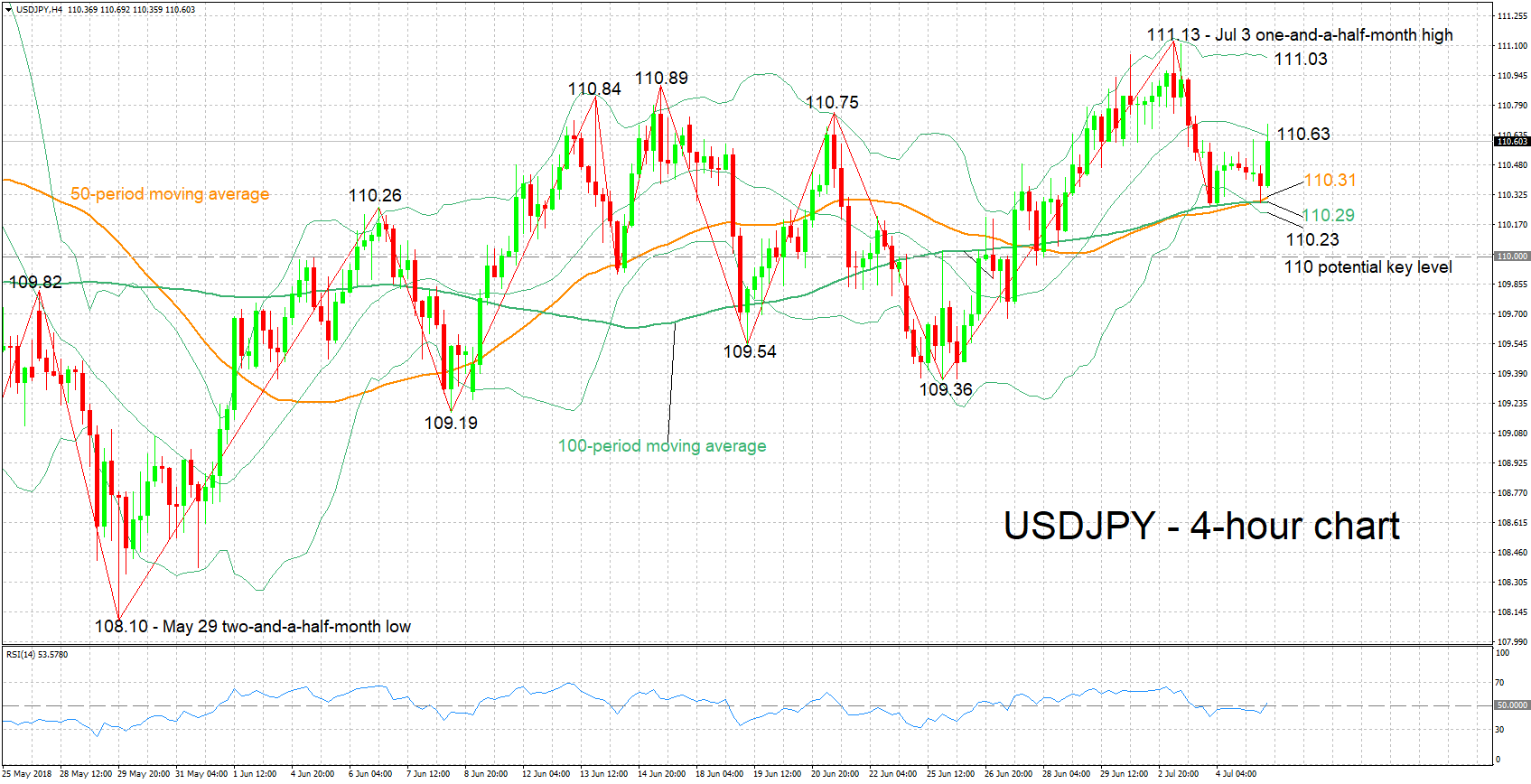

Technical Analysis: USDJPY looking mostly neutral in the short-term

USDJPY managed to gain some ground after touching a one-week low of 110.27 during Wednesday’s trading. The RSI has been largely moving sideways in support of a mostly neutral short-term picture, though it is currently attempting a move higher; a shift towards a positive momentum may be in the making, though it is too early to conclude towards that direction at the moment.

Should today’s minutes project a more hawkish Fed than already priced in after June’s meeting, then USDJPY is expected to move higher. The area around the middle Bollinger line (a 20-day moving average line) at 110.63 seems to be providing immediate resistance. Further above, the upper Bollinger band at 111.03 would be eyed, with the area around it encapsulating the 111 round figure, as well as the one-and-a-half-month high of 111.13 from July 3.

On the downside and in case of a more cautious Fed than initially perceived, the pair may meet support around the current level of the 50-day MA at 110.31; the 100-day MA at 110.29 and lower Bollinger band at 110.23 are also part of the region around this point. The 110 handle lies not far below and could provide additional support in case of steeper losses.

US releases earlier in the day can also move the pair.

{kind=link}