Here are the latest developments in global markets:

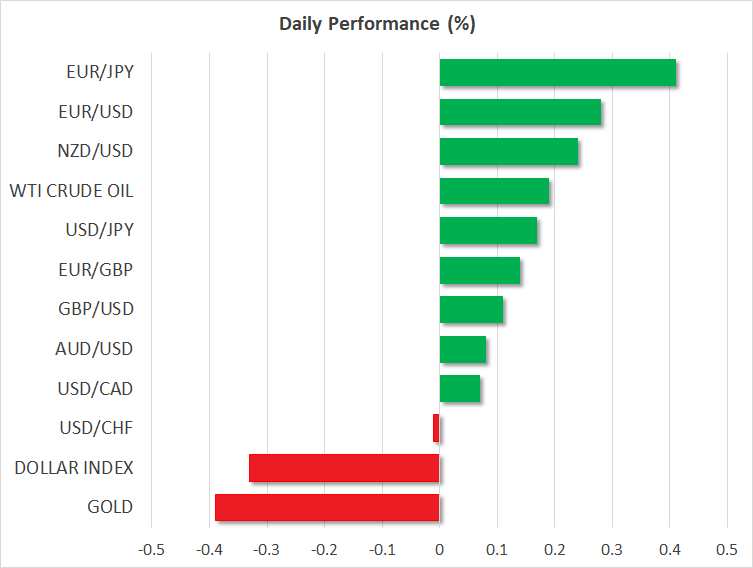

FOREX: The dollar was erasing yesterday’s losses made against the Japanese yen, last seen at 110.62 (+0.16%) as investors were optimistic that the FOMC meeting minutes due later today would deliver an overall hawkish message after June’s gathering signaled four rate hikes in total this year instead of three previously. The dollar index though was on the backfoot at 94.30 (-0.37%), pressured by a stronger euro and pound. Euro/dollar rallied significantly to touch a more-than-a -one-week high of 1.1720 before it fell to 1.1700 (+0.40%) after German factory orders in May printed the highest growth in six months. Comments by the ECB chief economist Peter Praet early on Thursday, stating that uncertainties about eurozone inflation have declined substantially also provided some support to the common currency. Yet, he added that patience on monetary policy is still needed. Moreover, sources revealing today that the EU is looking at options to reduce its tariffs on US automobiles, calming tensions with the US a day before US import tariffs on $34 billion Chinese products take effect, boosted confidence in the market as well. Euro/yen surged above 129.00 to peak at 129.51(+0.53%). Pound/dollar changed hands higher at 1.3254 (+0.17%) as latest PMI readings out of the UK showed signs that the UK economy is in recovery in the second quarter after finishing Q1 weaker. However, investors were not up to take a strong position on the currency as Brexit risks were still hanging in the background, with all eyes turning to Theresa May’s meeting with her cabinet on Friday where May will present the UK’s preferred position on the UK’s post-Brexit relationship with the EU. Meanwhile, speaking at a press conference, BoE chief Mark Carney said that the central bank and the government are working closely to prepare the economy for the very “unlikely event of a hard Brexit”. Still, Carney reiterated the case for limited and gradual rate hikes, further lifting cable. Euro/pound was marginally up at 0.8819. In antipodean currencies, aussie/dollar and kiwi/dollar were in bullish mode, increasing by 0.24% and by 0.36% respectively. Dollar/loonie was steady at 1.3135.

STOCKS: Hopes the EU could calm trade tensions with the US and upbeat factory data out of Germany helped European stocks to rise for the third day, with the benchmark European STOXX 600 and the blue-chip Euro STOXX 50 increasing both by 0.83% at 1130 GMT. The German DAX 30 went up by 1.55%, with all sectors but telecommunications and consumer non-cyclicals being in the green. The French CAC 40 rose by 1.24%, the Spanish IBEX 35 climbed by 1.35%, while the Italian FTSE MIB surged by 1.51%. The British FTSE 100 was up by 0.59%, while futures tracking major US stock indices were pointing to a positive open.

COMMODITIES: Oil prices managed to reverse higher early in the European session despite Trump’s demands for lower OPEC crude prices. Moreover on Thursday, threats from the Iranian president, Hassan Rouhani, to cut some level of cooperation with the International Atomic Energy Agency (IAEA) as well as warning that Iran would stop oil shipments from neighboring countries if the US persuades third parties to halt oil imports from Iran caped helped prices to gain ground. WTI crude and the London-based Brent were last seen up at $74.53/barrel (+0.53%) and at $78.26 (+0.03%) respectively. In precious metals, gold had almost reversed yesterday’s gains, extending down to $1,252.50/ounce (-0.38%). Copper dropped to an 11-month low of 2.84 (-1.60%) as investors sold the metal before the US import tariffs on Chinese products take effect this Friday.

Day Ahead: Eyes on FOMC minutes; US ISM non-manufacturing PMI and ADP employment report pending

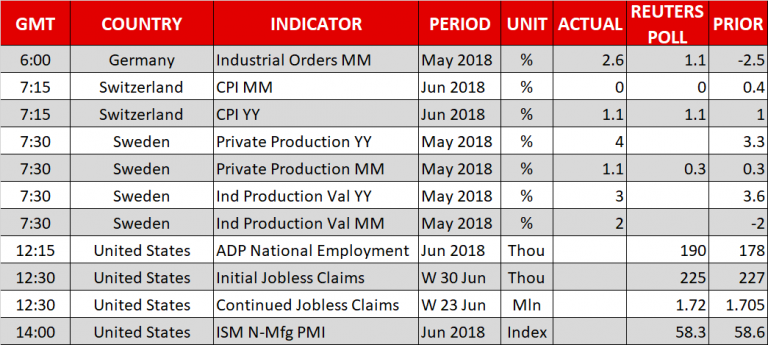

On Thursday, the release of the June’s Federal Open Market Committee meeting minutes at 1800 GMT is expected to be the main headline of the day. On June 12-13, FOMC members decided to increase the Federal funds by 25bps. Moreover, the new ‘dot plot’ was revised upwards to signal two more rate hikes by the end of the year, instead of just one more indicated in the previous one, marking a total number of four increases this year. Any perceived hawkish message is anticipated to push the dollar higher and vice versa.

Before then, the US calendar will be busier, delivering initial jobless claims for the week ending June 29, ISM non-manufacturing PMI readings and the ADP employment report regarding the nonfarm private sector ahead of tomorrow’s all-important NFP report.

At 1215 GMT, June’s ADP employment figures are expected to show an addition of 190k job positions compared to 178k in the prior month. However, it should be noted that although the ADP is the only major gauge that provides a preview for the NFP print, the correlation between the two figures has fallen notably in recent years. The US dollar lost ground in the previous couple of days and today’s data could drive the greenback slightly higher if the data come in better than expected.

At the same time, initial and continuing jobless claims out of the US for the week ending June 29 will be available as well, with analysts projecting the number of people claiming unemployment benefits for the first time to increase moderately by 4,000. Later on, at 1345 GMT, the country will see the release of June services and composite PMI figures by IHS Markit. Those would pertain to their final readings though they are not expected to gather much attention – analysts expect the figures to be released unchanged relative to their flash estimates.

Another major release left on the agenda is the US ISM non-manufacturing PMI, which is due at 1400 GMT. Expectations are for the print to reach 58.3 in June, from 58.6 previously. Coming on top of recent encouraging US data, an increase in the non-manufacturing index would be one more factor supporting the case for the Fed to deliver more than three rates hikes this year and could thereby help the dollar to rise somewhat further.

The Energy Information Administration’s (EIA) report including information on US crude and gasoline stocks for the week ending June 29 is scheduled to be made public at 1300 GMT. Crude inventories are anticipated to decline by around 3.538 million barrels compared to fall of 9.891 million barrels seen in the preceding week.

In terms of public appearances, German Chancellor Angela Merkel will meet UK Prime Minister Theresa May in Berlin for talks that are likely to address the slow progress in talks on Brexit negotiations at 1200 GMT. Also today, US Secretary of State Mike Pompeo will hold a two-day meeting with North Korean leader Kim Jong-un.

{kind=link}