Here are the latest developments in global markets:

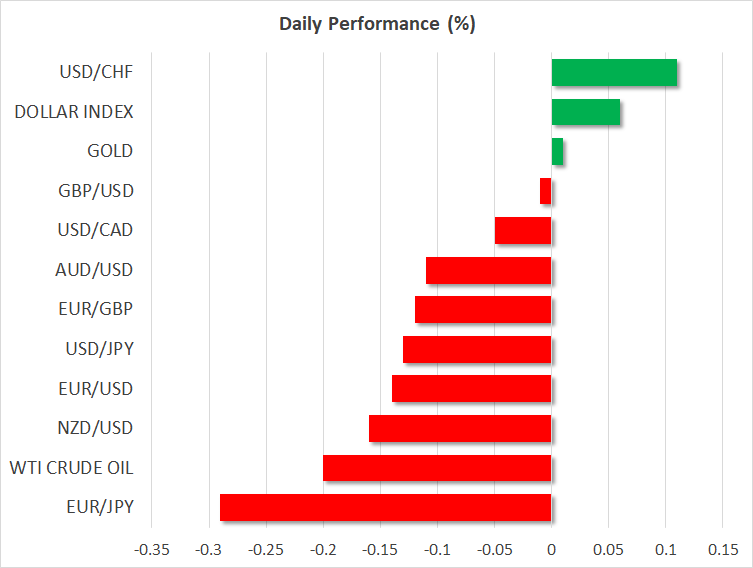

FOREX: The US dollar index is marginally higher on Monday (+0.06%), recovering some of the notable losses it posted on Friday following some relatively cautious remarks from Fed Chairman Powell that left the bulls disappointed. The euro capitalized on the dollar’s weakness and recovered across the board, while conversely, the yen retreated – weighed on by the boost in risk appetite that Powell fueled. Meanwhile, the British pound remained on the back foot, amid no signs of progress in Brexit talks.

STOCKS: Wall Street closed in the green on Friday, buoyed by some Fed signals that played down expectations for aggressive rate increases, thereby boosting risk appetite. The S&P 500 (+0.62%) and the Nasdaq Composite (+0.86%) both broke new record highs. The Dow Jones advanced too (+0.52%) but remained well away of its own all-time peaks. Futures tracking the S&P, Dow, and Nasdaq 100 are all currently safely in positive territory, pointing to a higher open today as well. In similar fashion, Asia was a sea of green on Monday. In Japan, the Nikkei 225 and Topix gained 0.88% and 1.16% respectively, while in Hong Kong the Hang Seng climbed by 2.17%. The same was true in Europe, where all the major indices were set to open much higher today, futures suggest.

COMMODITIES: WTI was down by 0.2% at $68.58 per barrel after posting its first weekly advance in around two months last week. A drawdown in US crude inventories, a strike in North Sea fields and upcoming US sanctions on Iran were factors supporting the precious liquid during the preceding week. Meanwhile, Brent crude traded lower by 0.1% at $75.73/barrel. In precious metals, dollar-denominated gold was flat at around $1.205.50 per ounce; in the previous week it gained on the back of broad dollar weakness.

Major movers: Dollar skids after Powell’s cautious remarks; NAFTA back in focus

The US dollar corrected lower on Friday, following some dovish-perceived comments from Fed officials, and most notably from Chairman Powell. Speaking at the Jackson Hole economic symposium, the Fed chief said he doesn’t see clear signs of inflation accelerating above the Fed’s target, and that the risk of the economy overheating is not major. His serene tone on the inflation outlook likely downplayed expectations for aggressive rate increases moving forward, sending the dollar lower and boosting risk appetite. Euro/dollar broke firmly back above the 1.1600 mark, while both the S&P 500 and the Nasdaq Composite touched new record highs in the aftermath as investors looked towards riskier assets.

The euro was the major beneficiary from the dollar’s weakness, advancing against all its major peers on Friday. Among the most notable movers was euro/sterling, which surged to reach a fresh one year high of 0.9057, before pulling back slightly today. Judging by the price action, sentiment towards the British pound remains highly fragile, amid a combination of a dovishly-priced BoE rate path and the continued lack of meaningful progress in the Brexit negotiations.

Turning to trade issues, recent media reports suggest that the US and Mexico are very close to completing a bilateral NAFTA agreement, setting the stage for Canada to finally rejoin the negotiations in order to finalize a trilateral deal. Adding credence to such expectations, US President Trump tweeted on Saturday that: “a big trade agreement with Mexico could be happening soon!”.

Indeed, seeing this through Trump’s eyes, a deal prior to the US midterm elections in November could be highly valuable, in the sense that it can be presented to the electorate as a victory with which to justify his administration’s confrontational trade policies. Any formal signs that a concrete agreement is inching closer could trigger a sizeable relief rally in the loonie, as trade uncertainty fades and investors price in a potentially more aggressive rate-hike path by the BoC.

Elsewhere, the yuan was little changed versus the greenback after surging on Friday to add 1.3%; the leg lower in USDCNH was spurred by the PBOC’s move to resume using a tool in its daily fixing of the pair that is supportive of the Chinese currency.

Day ahead: German Ifo surveys due; NAFTA deal on the horizon?

Monday’s calendar is rather light, featuring the Ifo surveys gauging business sentiment in Germany. Beyond releases, other developments, such as on NAFTA, will be closely monitored.

At 0800 GMT, the Ifo Institute’s surveys measuring business morale in Germany, the eurozone’s largest economy, will be made public. The business climate index, which barring a two-month period that remained steady, has been losing steam since reaching a record high in November, is anticipated to slightly improve in August. A minor improvement in August relative to July is also projected for the indices gauging current conditions and future expectations. Trade risks, including the threat of US tariffs on cars and auto parts, have been weighing on sentiment in previous months.

Dollar/peso started Monday’s trading with a gap lower as speculation that the US and Mexico are getting closer to a NAFTA deal continues to grow. Developments, which are also expected to affect the loonie, will be eyed.

Meanwhile, Brexit and trade are themes that remain in the background, with any commentary on these to fronts also having the capacity to move markets.

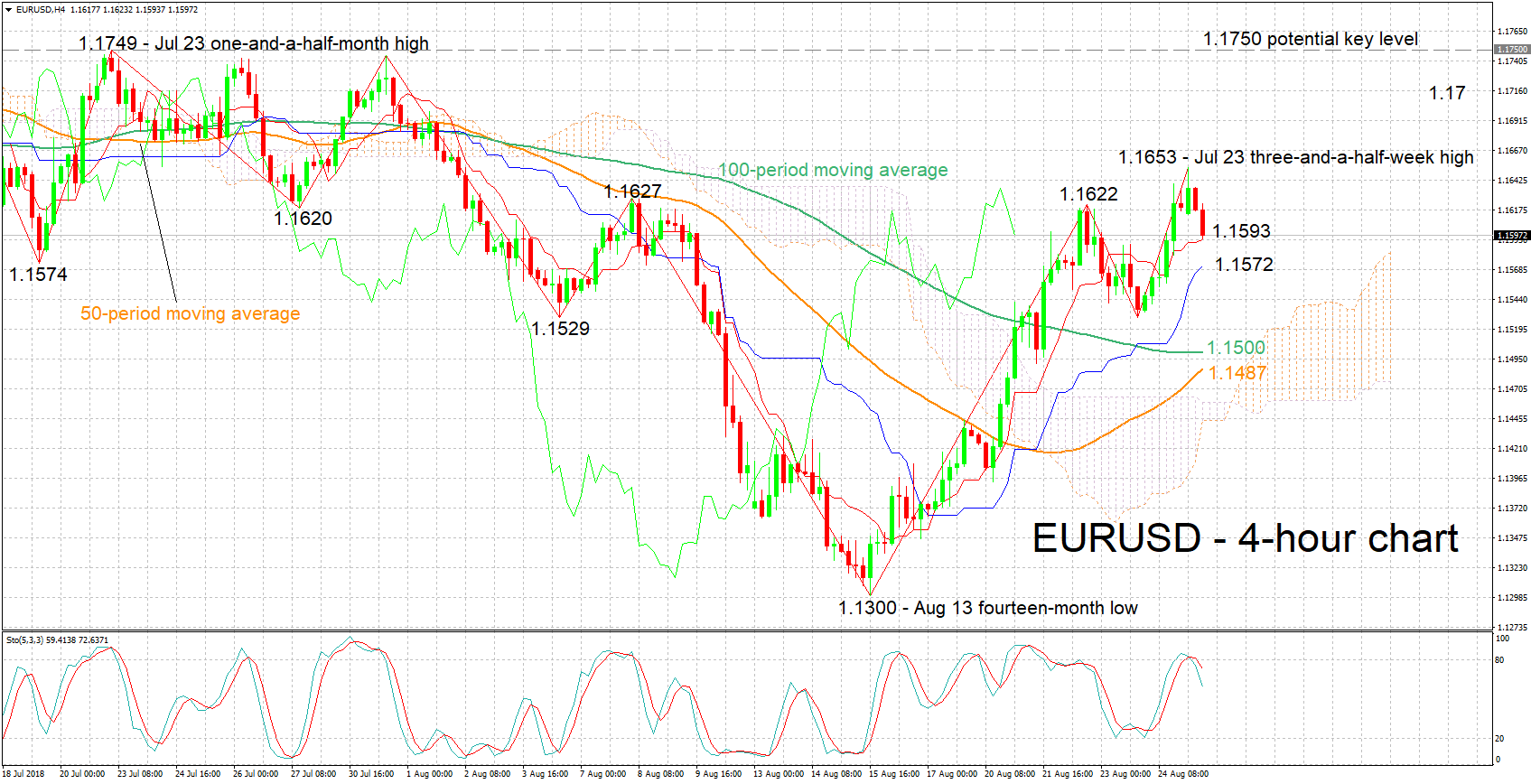

Technical Analysis: EURUSD eases a bit after touching 3½-week high; bearish signal by stochastics in very short-term

EURUSD has retreated a bit after hitting a three-and-a-half-week high of 1.1653 earlier on Monday. The Tenkan- and Kijun-sen lines remain positively aligned in support of a bullish bias, though the two have eased somewhat. In addition, the stochastics are giving a bearish signal in the very short-term, as the %K line has moved below the slow %D one.

Upbeat Ifo survey results out of Germany may boost the pair. Resistance to advances may come around the earlier hit three-and-a-half-week high of 1.1653, with stronger advances shifting the focus to the 1.17 round figure, and then to the zone around 1.1750 which encapsulates a few peaks from the recent past.

On the downside and in case of disappointing German data, immediate support seems to be taking place around the current levels of the Tenkan- and Kijun-sen lines at 1.1593 and 1.1572 correspondingly. Further below, the attention would turn to the area around the 100-day moving average at 1.1500.

{kind=link}