Here are the latest developments in global markets:

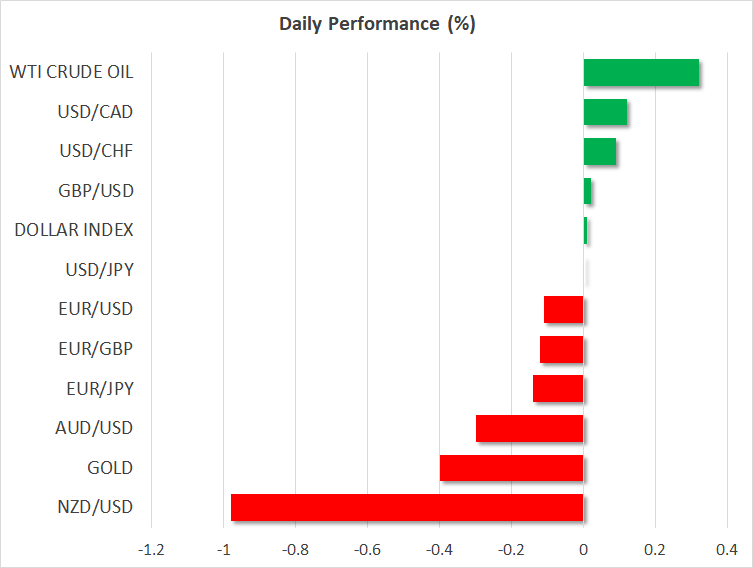

FOREX: The dollar is flat against a basket of six major currencies on Thursday, after it closed lower for a fourth consecutive session yesterday. The biggest mover was the British pound, which soared higher following comments from the EU’s chief Brexit negotiator suggesting that Europe is willing to offer the UK a special deal. Meanwhile, the kiwi plunged overnight after New Zealand’s latest business confidence data disappointed, amplifying expectations for a more dovish stance by the RBNZ moving forward.

STOCKS: Wall Street continued to rally into uncharted territory on Wednesday, with both the S&P 500 (+0.57%) and the Nasdaq Composite (+0.99%) hitting fresh record highs for the fourth consecutive session. The gains were led primarily by the tech sector. Meanwhile, the Dow Jones underperformed (+0.23%) its peers. As for today, futures suggest the S&P, Dow, and Nasdaq 100 may be set for a slightly lower open. The positive sentiment failed to extend to Asia though, which was a sea of red on Thursday. Japan’s Nikkei 225 and the Topix were both little changed, while in Hong Kong, the Hang Seng shed 0.86%. Markets in China were in the red as well. Europe was a similar story, with futures tracking all the major indices pointing to a negative open today.

COMMODITIES: Oil prices traded higher on Thursday, following a larger-than-projected drawdown in the weekly EIA inventory data released yesterday. WTI is up by 0.34% at $69.78 per barrel, while Brent crude rose by 0.28% to trade near $77.40/barrel. A warning from the IEA chief yesterday that oil markets may tighten further soon amid continued supply outages in Venezuela, as well as the dollar’s recent dip, may have also aided the move higher. In precious metals, gold is down by 0.40% today, hovering marginally above the psychological $1,200 zone, with no clear catalyst behind its underperformance.

Major movers: Sterling soars as Barnier stokes Brexit optimism; kiwi drops

The British pound exploded higher on Wednesday, following some comments from the EU’s chief Brexit negotiator, Michel Barnier. He said the EU is “prepared to offer Britain a partnership such as has never been with any other country”, stoking expectations that a Brexit deal may indeed be fleshed out in the coming months – something that was looking increasingly doubtful prior to his remarks. While his comments were vague overall, providing very few specifics, his apparent willingness to reach common ground with the UK was likely seen as a sign the EU is softening up its stance, thereby helping to reduce the political risk premium on the pound. Sterling/dollar surged roughly 180 pips to break back above the 1.3000 handle, while euro/sterling plunged by more than 100 pips, falling below the psychological 0.9000 zone.

Elsewhere, the yen retreated across the board, as the broader risk-on environment in markets led investors to decrease their safe-haven exposure. Dollar/yen touched a four-week high, propelled higher by yet another record close in US stock markets, even despite the greenback being an underperformer itself.

On the trade front, talks between Canada and the US appear to be gathering momentum. Canadian foreign minister Freeland said yesterday she had more productive talks with US trade representative Lighthizer, while President Trump said he thinks the negotiations are on track to bear fruit before Friday’s deadline. The loonie will remain sensitive to updates, with any hints from either Freeland or Lighthizer that a “preliminary deal in principle” may be achievable as early as tomorrow having the capacity to extend the currency’s latest gains.

Turning to the antipodeans, kiwi/dollar plunged by nearly 1.0% on Thursday, following disappointing business confidence data out of New Zealand. Business morale as gauged by the ANZ index continued to plunge, touching its lowest point in a decade and amplifying concerns that the pessimism may become self-fulling – leading to a slowdown in hiring and investment. The RBNZ has already stated that a rate cut remains on the table, and these data are likely to amplify such expectations, potentially keeping the kiwi under pressure. Aussie/dollar is also down by 0.32% today, after Australia’s capex data for Q2 surprisingly showed a decline in investment.

Day ahead: US core PCE, German inflation and Canadian GDP on the agenda; Brexit and trade also in focus

Thursday’s calendar is rather packed and includes the Federal Reserve’s preferred inflation gauge, German CPI readings and Canadian GDP. Beyond data releases, other developments, for example on the trade front and Brexit, are of importance and may act as major market-movers.

At 0830 GMT, the UK will be on the receiving end of data on consumer credit, as well as on mortgage lending & approvals, all for the month of July. However, Brexit developments in the aftermath of Barnier’s comments will undoubtedly be the primary driver of sterling pairs during today’s trading.

Numerous surveys gauging business sentiment in the eurozone during August are due out at 0900 GMT. All of them are expected to show a slight deterioration in morale relative to July. Meanwhile, final consumer confidence figures are anticipated to confirm eurozone consumer sentiment falling to its lowest since May 2017; the relevant index is forecast to stand at -1.9. For comparison, the US Conference Board’s consumer confidence index for August released earlier in the week jumped to a near two-decade high.

Of more importance for the euro are likely to be preliminary August inflation figures out of Germany at 1200 GMT. Month-on-month, CPI is expected to grow by 0.1%, below July’s 0.3% but leaving the year-on-year pace of growth unchanged at 2.0%. The Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, will also be monitored. It bears mention that these figures come one day ahead of the eurozone’s preliminary prints on August inflation and traders may thus use today’s German numbers to speculate on tomorrow’s euro-wide release, positioning themselves accordingly. It is also of note that unemployment data for August are also due out of Germany earlier in the day (0755 GMT).

Out of the US, the core PCE price index against which the Fed’s 2% inflation target is compared to, as well as data on personal income and consumption, all for the month of July, are slated for release at 1230 GMT. The core PCE price index is expected to expand by 0.2% on a monthly basis, above June’s 0.1%. This would put the year-on-year rate of growth at 2.0%, coinciding with the US central bank’s target and above the previously reported month’s 1.9%. In the meantime, personal income is forecast to ease to 0.3% m/m from June’s 0.4%, while consumption is predicted to remain unchanged at 0.4%. Overall positive data will probably boost the odds for a second quarter percentage point interest rate hike by the Fed in 2018; Fed fund futures currently put the probability for such an outcome at 68%. Lastly, weekly jobless claims data are also due at the same time.

Canadian monthly and quarterly GDP figures will be hitting the markets at 1230 GMT as well. Economic activity is anticipated to have expanded by 0.1% m/m in June, below May’s respective print of 0.5%. However, the economy is projected to have accelerated in Q2, growing by 3.0% on an annualized basis. This compares to Q1’s 1.3% and bodes well with the Bank of Canada’s view earlier in the year that the slowdown during the first quarter was temporary in nature.

At the moment, Canadian OIS show market participants having fully priced in another 25bps rate increase by the Bank of Canada in 2018, while they see the odds for a second such increase at roughly one-in-five. A data beat is likely to push that probability further up and consequently support the loonie; the opposite holds true as well. Also important for the rate trajectory and the currency’s direction are trade developments, which will also be closely watched. In this respect, will Canada swiftly join the US and Mexico with their trade plans or will it enter into long discussions that may even result in a no-deal outcome?

Elsewhere, President Donald Trump accused China of undermining US efforts to exert pressure on North Korea to proceed with denuclearization. The trade confrontation therefore seems to be moving into other directions. Will another chapter in the “US vs China” saga be written soon?

In emerging markets, the ongoing slide in the Turkish lira and the Argentine peso will be monitored; the fall in these currencies has the potential for spillover effects in other emerging economies.

The head of the Bundesbank, Jens Weidmann, whose name often comes to the fore as a possible successor to ECB chief Mario Draghi when his term expires in late 2019, will be speaking at 1730 GMT.

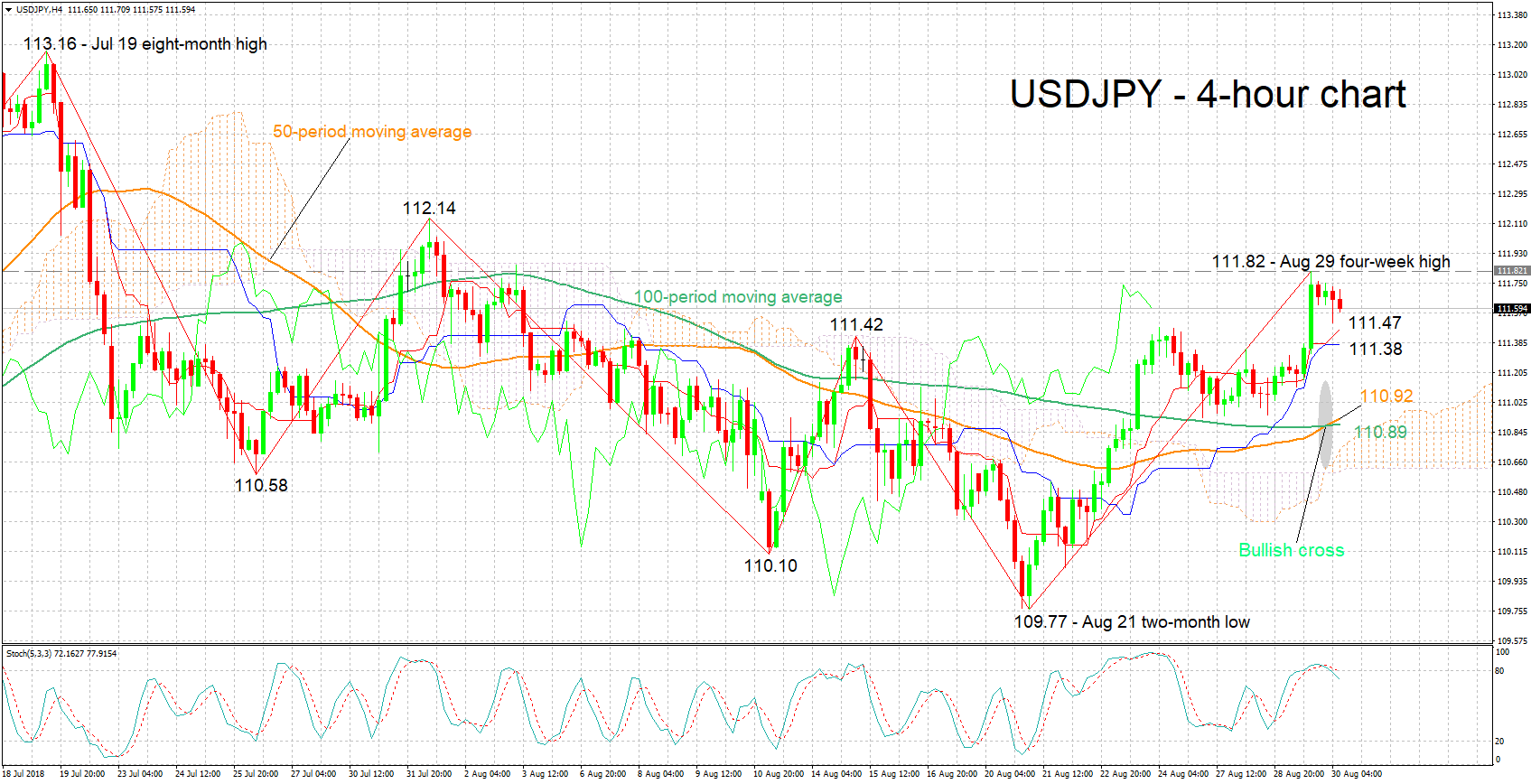

Technical Analysis: USDJPY bullish bias eases after pair touches 4-week high; bearish signal by stochastics in very short-term

USDJPY has eased a bit though it continues to trade not far below Wednesday’s four-week high of 111.82. The Tenkan- and Kijun-sen lines remain positively aligned – a bullish short-term signal – though the flattening Kijun-sen is a sign of weakening positive momentum. Moreover, the stochastics are giving a bearish signal in the very short-term as the %K line has moved below the slow %D one while both lines were above 80.

Upbeat US data later today will likely boost the pair. Resistance to rises may occur around yesterday’s peak of 111.82, including the 112 round figure; a previous top lies not far above at 112.14. Further above, the pair’s highest since the start of the year of 113.16 would increasingly come into scope.

On the downside and in case of disappointing US data, immediate support could come around the current levels of the Tenkan- and Kijun-sen lines at 111.47 and 111.38 correspondingly. Further below the zone around the current levels of the 50- and 100-period MAs at 110.92 and 110.89 respectively – including the 111 handle – would be eyed.

Rising tensions between the US and China can also affect the pair.

{kind=link}