Here are the latest developments in global markets:

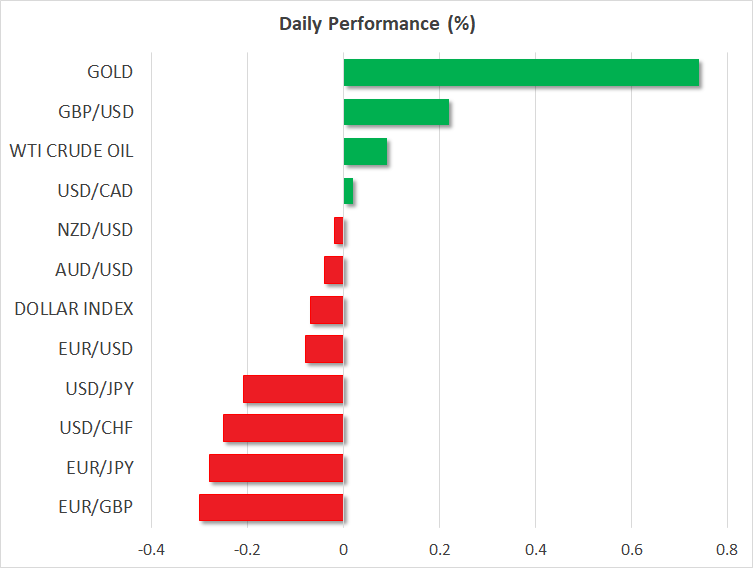

- FOREX: The pound continued the rally today that it posted yesterday on reports that Germany and the UK have dropped key Brexit demands after giving back some of them on Wednesday on new headlines that Germany has not changed position on Brexit. Pound/dollar rose by 0.26% above 1.2900, while euro/pound dropped by 0.29% below the 0.9000 round number. Furthermore, euro/dollar turned negative after it opened the day in the green, retreating by 0.06% to 1.1620 following disappointing German factory orders which fell by 0.9% in July instead of rising by 1.8% as analysts predicted. In June the gauge plunged by 4.0%. Dollar/yen was trading lower by 0.21% at 111.28 and the US dollar index was losing 0.07% ahead of a crucial trade deadline later today. In commodity-linked currencies, aussie/dollar, kiwi/dollar, and dollar/loonie held steady around their opening levels. It is worth to mention that on Wednesday, the BOC kept interest rates unchanged as was expected, while in the accompanying statement officials kept the door open for a rate increase at their upcoming gathering.

- STOCKS: European benchmarks were mixed at 1100 GMT. The pan-European STOXX 600 was steady and the blue-chip Euro STOXX 50 was down by 0.09%. Meanwhile, the German DAX, the French CAC 40 and the Italian FTSE MIB were trading higher by 0.07%, 0.16% and 0.31% correspondingly. However, the UK’s FTSE and the Spanish IBEX 35 declined by 0.14% and 0.65% respectively. In US stocks, the Dow Jones the S&P 500 and the tech-heavy Nasdaq 100 were poised to open higher according to E-mini futures.

- COMMODITIES: Oil prices were posting gains, though those were limited in magnitude. WTI crude edged up by 0.04% to $68.75 after the API weekly inventory report yesterday showed a 1.200-million-barrel drawdown. Brent rose by 0.26% to $77.47 per barrel. In addition, gold price is set to complete the second bullish day in a row, adding 0.74% to its performance as the dollar remained under pressure.

Day ahead: Trade deadline looms; ADP employment, factory orders, and ISM non-manufacturing PMI pending

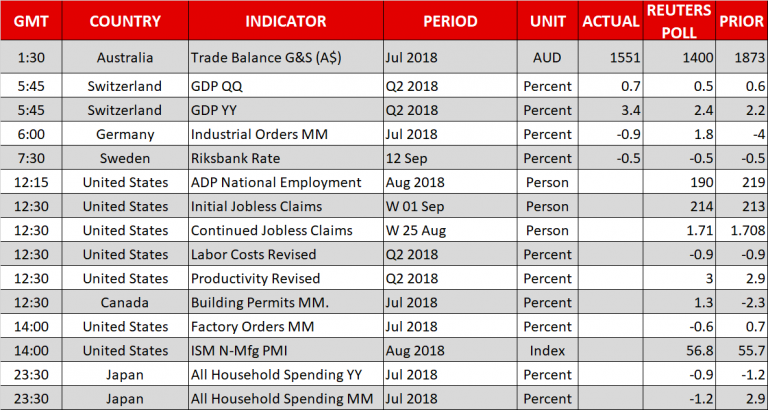

Thursday is expected to be another trade-dependent day for the markets as the US prepares to trigger another round of tariffs against China after the public comment period comes to an end today. Earlier, however, the ADP employment report, factory orders, and ISM non-manufacturing PMI out of the US could spread some volatility to the markets.

At 1215 GMT, the ADP research institute is expected to say that private non-farm job positions in the US increased by 190k in August after rising by 219k in the previous month, the highest growth recorded since April. While the report could be considered an early clue to the government’s jobs stats due on Friday, which are more comprehensive as they count for both public and private sectors, the correlation between the two has weakened over the past couple of years, with the ADP figure diverging more often from the NFP number.

A few minutes later at 1230 GMT, the US Department of Labor will publish its weekly jobless claims figures for the week ending September, while at the same time the Bureau of Labor Statistics will be issuing final quarterly estimates on labor unit costs and productivity for the second quarter. A bit later factory orders and ISM non-manufacturing PMI, which are of greater importance to investors, could bring some spikes to the markets. Forecasts are for the former to decline by 0.6% m/m in July after two straight positive months, while the latter is anticipated to climb from 55.7 to 56.8 in August. Recall that the ISM manufacturing PMI delivered on Tuesday surged to the highest in 14 years in the same month.

Still, traders could prefer to act cautiously during the day amid fears that trade risks could escalate to a new level following the end of the public comment on additional US import tariffs against China on Thursday. Should Trump press ahead with his threat of tariffs on $200 billion Chinese imports, marking the biggest attack against China in their month-long trade dispute so far, risk-off sentiment could fire up once again, with investors shifting funds out of riskier assets such as stocks. The action may raise voices in China as well, forcing Beijing to take countermeasures as China’s Commerce Ministry reiterated today; probably unleashing penalty duties on a $60 billion list of American products.

Out of the US, Brexit will be another persisting headache as the latest headlines on the topic brought some confusion to the markets. Yesterday, the German and the British governments softened their stance on Brexit demands according to people familiar with the matter, backing a less detailed agreement to get a deal done. While the statement increased optimism that the EU and the UK could come closer to solve their disagreements, shortly after a Reuters report said that German officials have not changed their views, pushing the pound back down.

In other areas of interest, Canada will see the release of building permits for the month of July at 1230 GMT. In Japan, July’s household spending will come out at 2330 GMT, while in Germany eyes will turn to industrial production and trade readings on Friday at 0600 GMT.

Emergency markets will be closely watched as trade uncertainties and political noises have weighed heavily on investors sentiment, with the Indian rupee collapsing to fresh record lows on Thursday. The Russian rubble was on the back foot as well, whereas the Turkish lira, the Argentine and the Mexican pesos, and the South African rand were somewhat recovering.

In oil markets, the Energy Information Administration will give its weekly updates on US oil inventories for the week ending September 1 at 1500 GMT.

In terms of public appearances, a number of speeches are scheduled for today. At 1145 GMT, Sabine Lautenschlager, member of the ECB’s Executive Board will be speaking at the Eurofi Financial Forum. At 1400 GMT, Federal Reserve Bank of New York President John Williams (permanent FOMC voting member) will be participating in a chat on the regional and national economy, while at 1845 GMT Bank of Canada Senior Deputy Governor Carolyn Wilkins will be commenting at Saskatchewan Trade and Export Partnership. A meeting between the French President Emanuel Macron and the Luxemburg Prime Minister, Xavier Bettel which will cover topics on the future of the European Union could be of interest as well.

{kind=link}