Here are the latest developments in global markets:

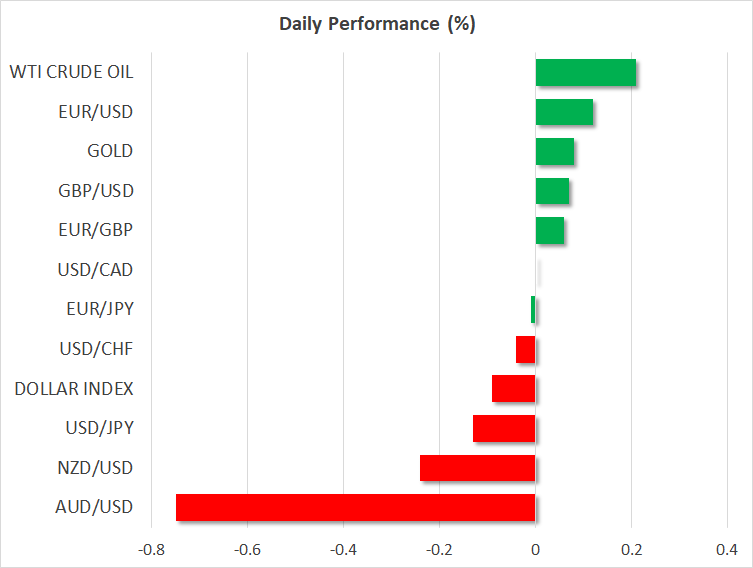

FOREX: The US dollar is marginally lower against a basket of six major currencies on Friday (-0.08%), ahead of the release of the all-important US payrolls report at 1230 GMT, where focus may once again fall primarily on the earnings figures. Safe-haven currencies like the yen and the Swiss franc rallied amid trade jitters, while the risk-sensitive aussie faltered, touching a fresh low last seen in early-2016 against the dollar.

STOCKS: US markets closed lower for the most part on Thursday, dragged down by tech-weakness amid jitters for regulation in the sector, and mounting concerns over fresh tariffs being imposed soon. The tech-heavy Nasdaq Composite (-0.91%) underperformed as tech leaders like Facebook (-2.78%), Twitter (-5.87%), and Google-parent Alphabet (-1.26%) extended their recent losses. Meanwhile, the S&P 500 fell by 0.37%, though the Dow Jones that is less exposed to tech managed to eke out a 0.08% gain. Asia was also mostly in the red on Friday, with Japan’s Nkkei 225 and Topix dropping by 0.80% and 0.48% respectively. In Hong Kong, the Hang Seng was down by a mere 0.10%. Europe was a different story though, with all the major benchmarks set for a modestly higher open today, futures suggest.

COMMODITIES: Oil prices edged lower on Thursday amid the broader risk-off market environment, even despite a larger-than-anticipated drawdown in the weekly EIA crude inventory data. Investors may have focused on a different part of that report, which showed gasoline inventories rising sharply, confounding expectations for strong US fuel consumption by drivers over the summer. In the near-term, oil will remain mindful of updates in the Sino-American trade standoff, with any escalation likely weighing on the liquid via speculation for slower demand growth. In precious metals, gold is up on Friday albeit by less than 0.1%, trading within breathing distance of the $1,200 handle and remaining in the relatively narrow range it established over the past three weeks, between $1,182 and $1,214.

Major movers: Yen advances as risk appetite falters; BoC’s Wilkins lifts loonie

Risk sentiment remained sour on Thursday, with safe-haven currencies such as the yen and the Swiss franc attracting inflows amid mounting concerns for further escalation in America’s trade standoff with its major partners. The public consultation period over US tariffs on an additional $200bn Chinese goods ended yesterday, and although the US has not moved forward with imposing those tariffs yet, investors likely took a defensive stance in anticipation for such action. Meanwhile, a WSJ report suggested that Japan is likely the next target on Trump’s trade radar, generating concerns that tensions may ratchet up even further before long.

Dollar/yen fell alongside US stock indices, breaking back below the 111.00 zone, while dollar/franc also dropped sharply to touch a fresh five-month low. As for risk-sensitive currencies, aussie/dollar is down by 0.75% on Friday, recording a new two-and-a-half year low.

The dollar remained sluggish though, ending Thursday’s session lower against a basket of six major currencies – unable to capitalize on trade worries like it did in recent months. On the US data front, developments were mixed but perhaps positive on the margin. The ADP employment report for August missed estimates, likely generating some angst that the NFP print may also disappoint today. That said, the ISM non-manufacturing print rose by much more than expected, and coming on top of a similarly encouraging manufacturing index, it pointed to a robust US economy in Q3.

In Canada, the loonie was on the back foot for most of Thursday’s session amid poor risk appetite and declining oil prices, but got a helping hand from BoC deputy Governor Carolyn Wilkins to end the day higher. She said policymakers debated dropping a reference of maintaining a “gradual approach” to rate increases at the latest BoC meeting, hinting at the prospect of faster hikes in the future amid an economy operating at full capacity. The loonie extended its gains a few hours later, this time on trade news after US President Trump said he believes Canada will be part of NAFTA. The negotiations continue today and the loonie will likely remain ultra-sensitive to any updates, with Canada’s employment data also being in focus later in the session (see below).

Day ahead: US employment data in focus; fresh trade-war twists to be expected?

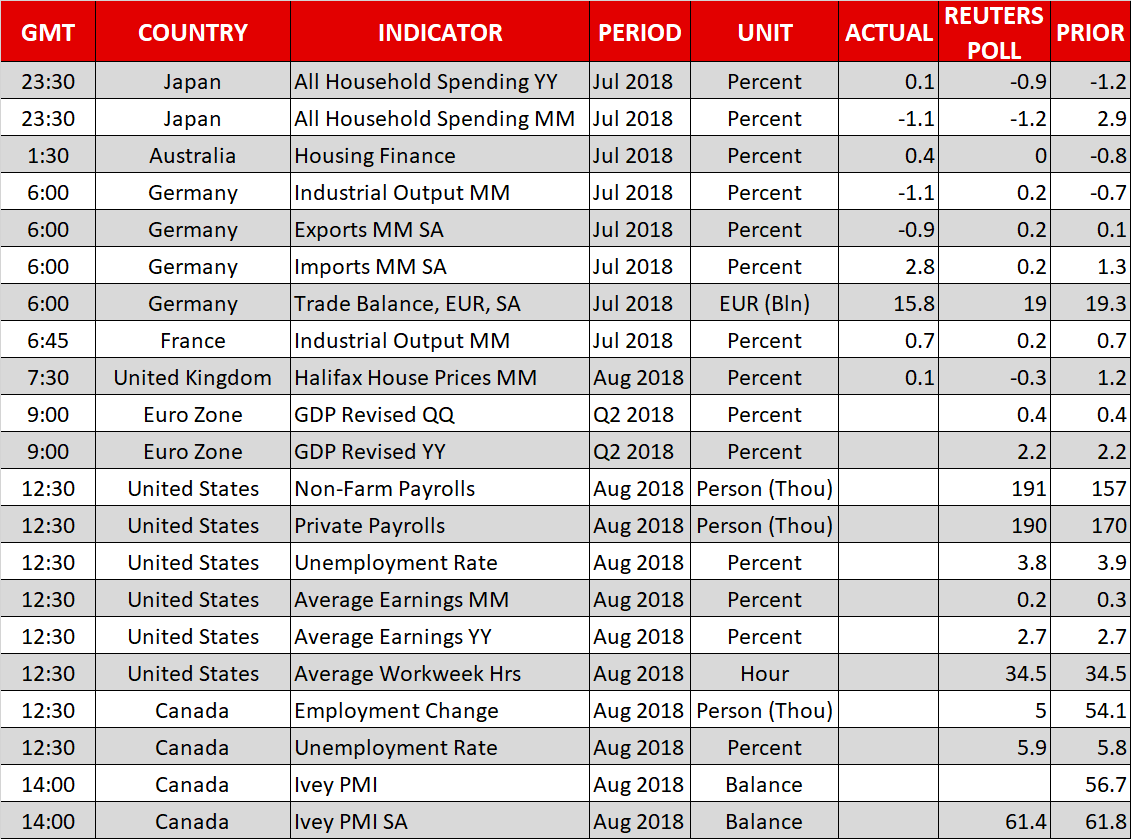

The lion’s share of attention out of Friday’s releases is expected to fall on the US jobs report for August. In the meantime, trade issues continue to remain in focus.

On the trade front, the public comment period for proposed US tariffs on an additional $200 billion in Chinese imports has expired and the levies could be implemented soon, likely leading to intensifying tensions between the world’s two largest economies. Moreover, a fresh twist in the trade war saga may emerge soon given that the Wall Street Journal reported that President Trump may now turn his attention on trade issues with Japan. Another theme that can affect broad market sentiment and which remains in the background is emerging market angst.

At 0730 GMT, the Halifax index gauging house prices in the UK during August will be made public. However, any Brexit headlines will again be eyed as those are the ones having the capacity to spur sharp movements in sterling pairs.

Revised eurozone GDP figures for Q2 hitting the markets at 0900 GMT are expected to confirm quarterly growth running at 0.4% q/q and 2.2% y/y – this compares to Q1’s annual pace of growth of 2.5%.

The highly anticipated US employment report is due at 1230 GMT. The economy is projected to have added 191k positions in August, above July’s 157k. Additionally, the unemployment rate is forecast to tick down to 3.8% from July’s 3.9%, matching a low last experienced in April 2000 (this level was also revisited in May of the current year). Wage growth, which is seen as having the capacity to stoke inflationary pressures, will again be coming to the fore. In this respect, average earnings are predicted to have grown by 0.2% m/m, below July’s 0.3%. This would still leave the annual pace of growth on earnings at 2.7%.

The Federal Reserve is widely anticipated to hike rates when it meets in late September, with markets pondering whether it will deliver a second 25bps increase during the remainder of the year. Fed funds futures project a 63% chance for a second rise. Strong jobs data later today, especially on the wage front, are likely to boost those odds and consequently lift the dollar. The opposite holds true as well.

Canadian employment numbers for August are also due at 1230 GMT. A considerable easing in the number of jobs added is expected; 5.0k vs 54.1k in July. Furthermore, the unemployment rate is forecast to rise to 5.9% from 5.8% in July. This would still leave it close to multi-decade low levels, pointing to a relatively tight labor market. Similar to the US, the data will likely shape investors’ near-term outlook on interest rates. The probability for an October hike by the Bank of Canada currently rests at around 58% according to Canadian OIS. Lastly, the country will also be on the receiving end of Ivey PMI data for the same month at 1400 GMT, with the loonie possibly proving most sensitive to NAFTA-related developments.

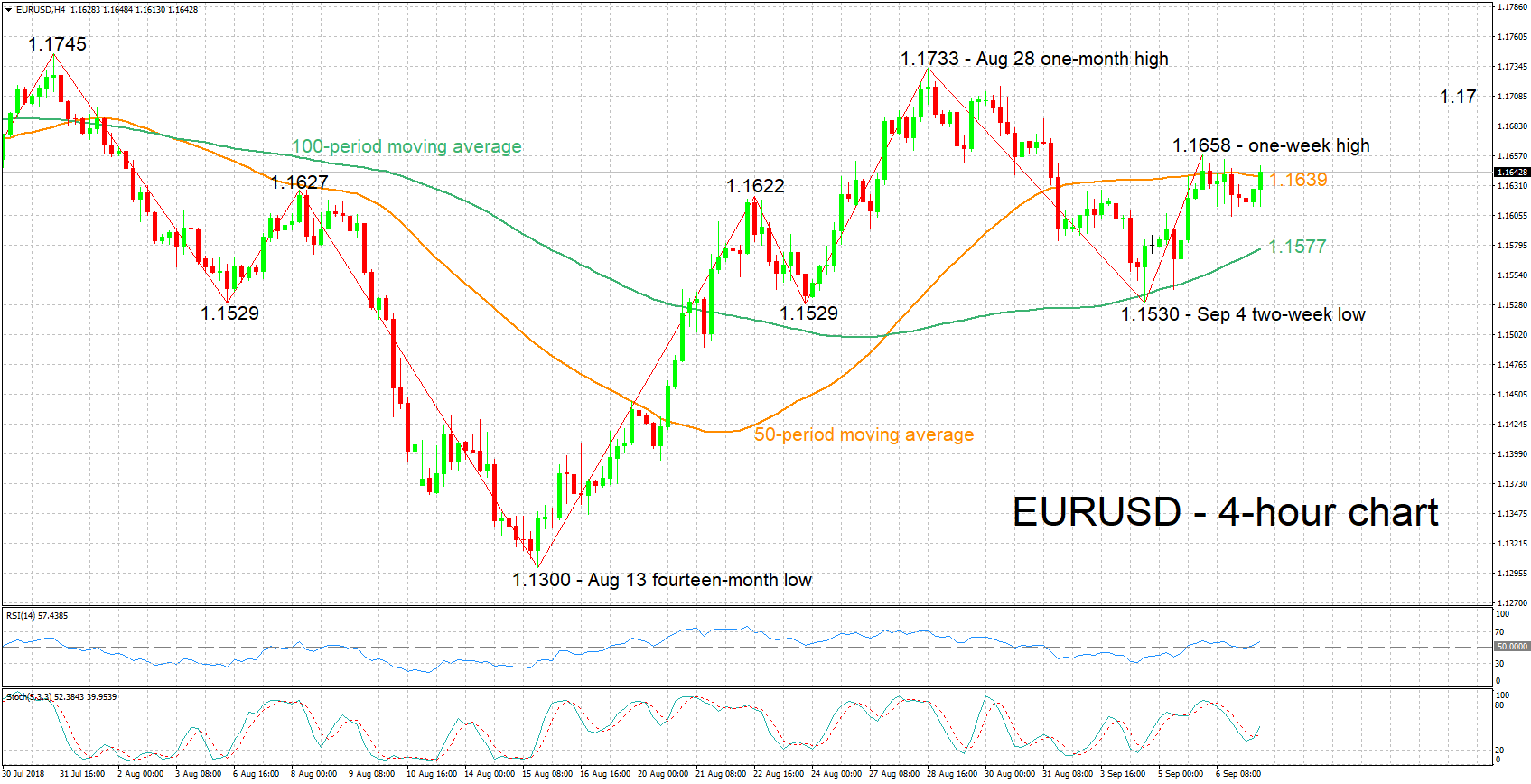

Technical Analysis: EURUSD attempts conclusive move above 50-period MA; bullish signal by stochastics in very short-term

EURUSD is currently trading marginally above the 50-period moving average line. The RSI seems to be attempting a move higher which could be an early sign of short-term momentum turning positive. Turning to the stochastics, the %K line has moved above the slow %D one. This is a bullish signal in the very short-term; a decisive move up by both lines would confirm the strength of the signal.

Strong US jobs data are likely to weigh on the pair, pushing it down. Support to declines may come around the current level of the 100-period MA at 1.1577; the 1.16 round figure is also part of the area around this point. Further down, the two-week low of 1.1530 from earlier in the week would be eyed for additional support.

Conversely, disappointing figures could boost the pair. Immediate resistance may take place around yesterday’s one-week high of 1.1658. Further above and given a move above the 1.17 handle, the one-month high of 1.1733 from late August would come into scope.

Regional Fed presidents Eric Rosengren (non-voting FOMC member in 2018), Loretta Mester (voter) and Robert Kaplan (non-voter) will be making public appearances at 1230 GMT, 1300 GMT and 1720 GMT respectively. Elsewhere, RBNZ Governor Adrian Orr will be giving a speech at 2130 GMT.

Meanwhile, a meeting between French President Emmanuel Macron and German Chancellor Angela Merkel touching on Brexit, immigration and the eurozone might be of interest.

In energy markets, the Baker Hughes weekly report on active oil rigs in the US is due at 1700 GMT.

{kind=link}