Here are the latest developments in global markets:

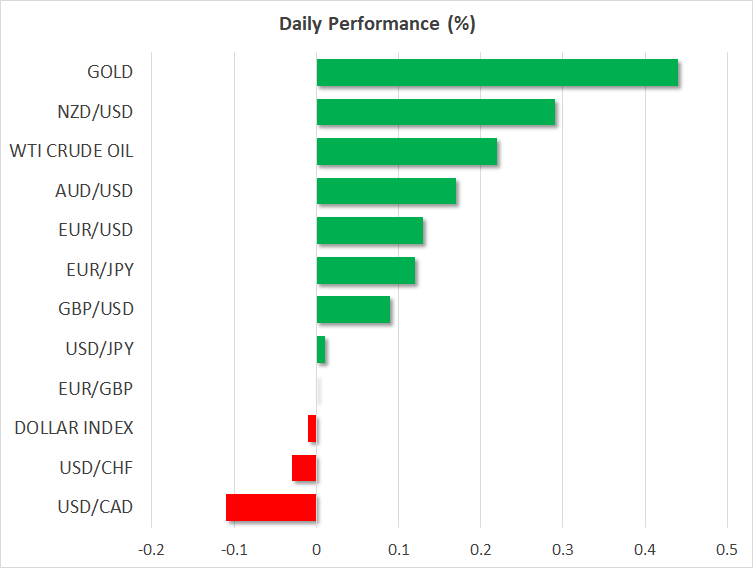

FOREX: The US dollar index is nearly unchanged on Friday (-0.02%), holding on to the losses it posted in the previous session following a disappointment in the US CPI inflation data. The yen also retreated across the board, as risk appetite remained firm and investors rotated funds out of haven assets and into riskier ones. Meanwhile, the euro gained slightly after the ECB confirmed its normalization plans remain on track yesterday, while the pound was little changed after the respective BoE policy gathering.

STOCKS: Wall Street closed in the green on Thursday, with risk appetite boosted by China’s foreign ministry welcoming the invitation for trade talks with the US. The tech-heavy Nasdaq Composite (+0.75%) surged the most, aided by a rebound in Apple (+2.42%), while the Dow Jones (+0.57%) and the S&P 500 (+0.53%) also advanced. Futures suggest the S&P, Dow, and Nasdaq 100 are all set for a significantly higher open today as well. Asia was a sea of green on Friday, with Japan’s Nikkei 225 (+1.20%) and Topix (+1.09%) posting notable gains, while the Hang Seng in Hong Kong (+0.97%) also climbed. In Europe, all the major indices were set to open higher today, futures suggest, with the only exception being the Italian FTSE MIB.

COMMODITIES: Oil is trading slightly higher on Friday, recovering some of the notable losses recorded in the previous session. The tumble came after the International Energy Agency (IEA) warned that mounting risks around emerging markets and global trade are clouding the outlook for future oil demand. WTI is up by 0.22% at $68.86 per barrel today, while Brent rose by 0.14% to $78.37 a barrel. In precious metals, gold is higher by 0.44% on Friday, last seen around the $1,207 per ounce zone. The dollar-denominated yellow metal has firmed in recent days, albeit only marginally, drawing strength from a continued pullback in the greenback.

Major movers: Yen sharply lower as risk appetite firms; dollar dips after CPIs

The BoE and the ECB delivered no surprises at their respective meetings on Thursday, with both Banks largely reiterating previous forward guidance. The BoE stood pat, noting that signs of greater uncertainty around Brexit are causing investment plans to soften. On a more positive note, it also upgraded its Q3 GDP estimate, striking a rather balanced tone overall. Hence, the pound barely reacted, though sterling/dollar did close the session higher amid dollar-weakness. Market-implied pricing (UK OIS) suggests the BoE will hike again in September next year – an expectation so pessimistic relative to the healthy state of the UK economy that it likely incorporates some jitters around Brexit as well.

The ECB gathering was equally uneventful, with the Bank revising marginally lower its growth forecasts, as had been expected. Draghi repeated the ECB is proceeding with tapering its QE program – highlighting that although protectionism and EM wobbles pose risks, they aren’t dire enough to derail the Bank’s normalization plans. Meanwhile, he shrugged off the lower GDP forecasts, noting instead that policymakers are becoming more confident in their core inflation forecasts amid rising wages. He maintained a neutral tone in general, which likely surprised some investors that expected him to lean dovish amid softer growth projections. Hence, the euro rose in the aftermath, touching a two-week high against the dollar.

Surprisingly, it was the Japanese yen that was the biggest mover – and underperformer – in Thursday’s session. The safe-haven currency plunged across the board, recording a six-week low against the dollar, euro, and pound amid strong risk appetite in markets. On the trade front, China welcomed the US invitation for trade talks, which may have aided the rotation out of haven assets. While Trump said a few hours later he feels “no pressure” to strike a deal with China, his comments were likely perceived as more posturing, evident by the limited market reaction.

In the US, the dollar dipped after the US CPI data for August disappointed, with the headline inflation rate falling by more than expected, and the core CPI rate unexpectedly declining to 2.2% in yearly terms, instead of holding steady at 2.4% as expected. While the dollar did tumble on the news, it’s interesting to note that market pricing for further Fed rate hikes this year remained surprisingly stable.

In EM, the Turkish lira soared yesterday after the nation’s central bank raised interest rates by 625bps to 24.00%, in an attempt to stabilize the battered currency and rein in double-digit inflation.

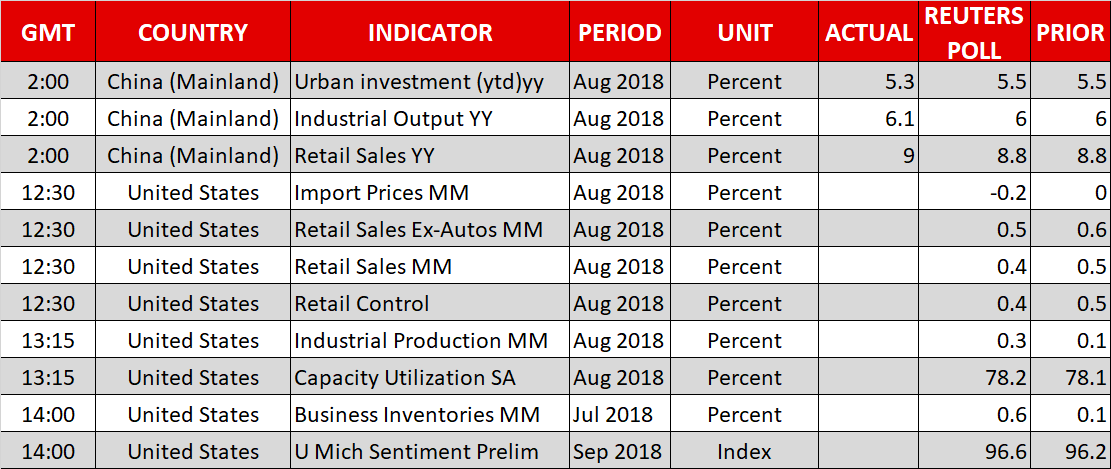

Day ahead: US retail sales, industrial output and U of M consumer sentiment due; trade remains in focus

The highlight out of Friday’s calendar are US retail sales data, with the figures on industrial and manufacturing output out of the country, as well as the University of Michigan’s (U of M) index that gauges consumer morale, attracting attention as well. Besides economic releases, trade developments will again be in focus.

On trade, news that the US and China are preparing to enter a new round of trade talks boosted market sentiment. However, the two parties’ confrontational stance may not easily change; President Trump yesterday tweeted that the US was under “no pressure” to reach a trade deal with China, something which led US stocks to give back some of their earlier gains.

In terms of US retail sales due out at 1230 GMT, those are anticipated to grow by 0.4% m/m in August, down from 0.5% in July. Core retail sales – the measure of sales that excludes automobiles and which more closely aligns with the consumer spending component of GDP – are projected to expand by 0.5% on a monthly basis, again reflecting a slowdown compared to July’s 0.6%. More data disappointment, building on PPI and CPI misses from earlier in the week, is likely to lead to further losses in the dollar; the dollar index is looking set to finish the week in the red after advancing during the preceding week. Elsewhere, import and export price data for August will also be released at 1230 GMT.

US industrial production figures for August will be hitting the markets at 1115 GMT. The numbers are forecast to show output accelerating to 0.3% m/m from 0.1% in July. The prints on manufacturing production, a subset of industrial output, will also be generating attention. In light of Trump’s trade policies and the disruptions they cause on global supply chains, it would be interesting to see whether such actions materially affect factory activity. The reading on August’s capacity utilization will be released at the same time.

Also out of the US, the U of M’s preliminary survey on September consumer sentiment is due at 1400 GMT and is anticipated to show a slight improvement in morale relative to August. Furthermore, the survey’s sub-indices measuring inflation expectations will also be monitored. Meanwhile, data on July’s business inventories will be made public at the same time.

In terms of policymakers’ appearances, Bank of England Governor Mark Carney will be giving a lecture at 1000 GMT, while Chicago Fed President Charles Evans (non-voting FOMC member in 2018) will be speaking at 1300 GMT.

In energy markets, the weekly report by Baker Hughes on active US oil rigs is due at 1700 GMT, while traders will also be keeping an eye on Hurricane Florence’s path to the US east coast.

Lastly, EM-market action will be watched: Thursday’s surge in the Turkish lira after the country’s central bank raised its benchmark rate by 625bps helped lift other EM currencies as well.

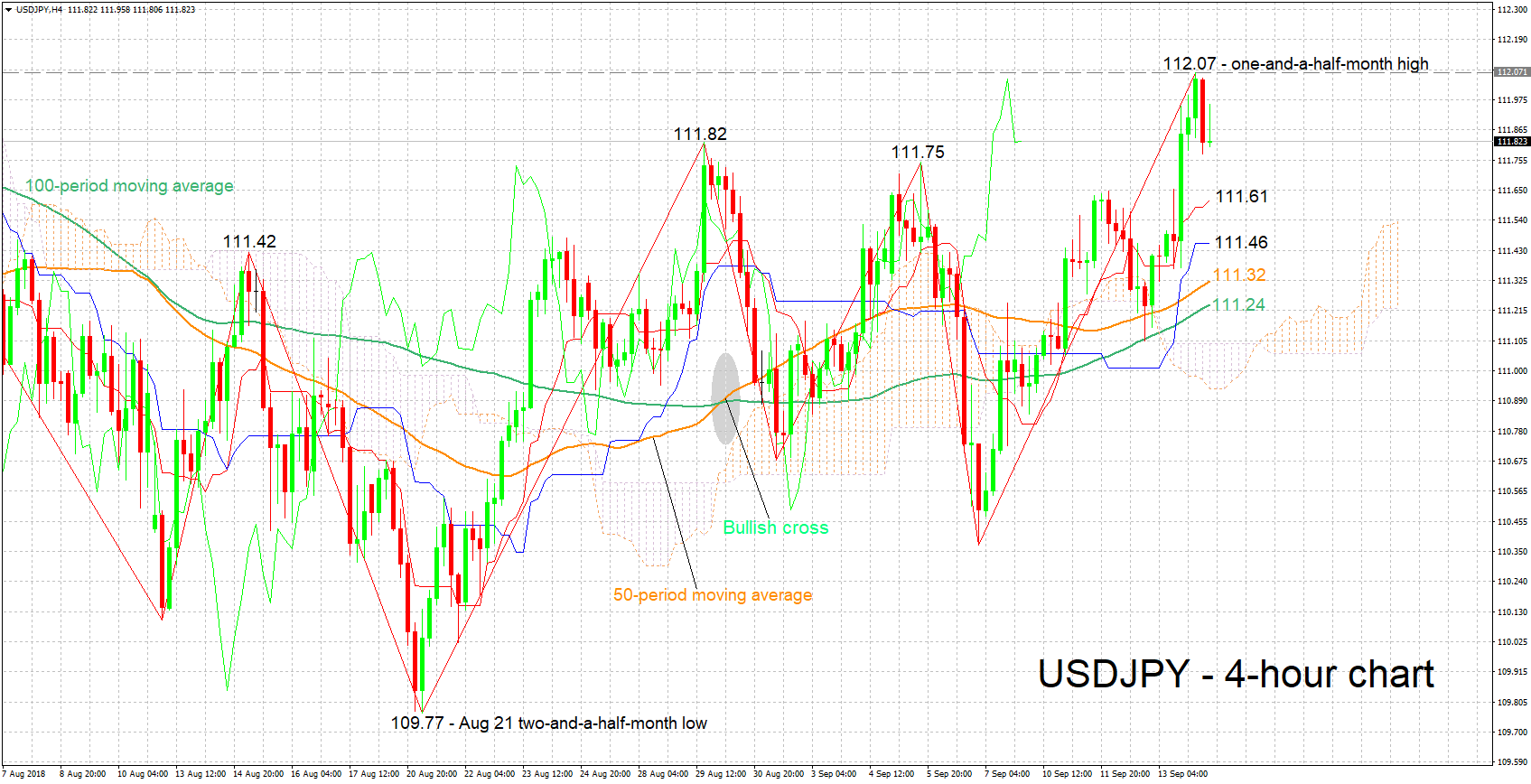

Technical Analysis: USDJPY hits 1½-month high but bullish momentum appears to ease

USDJPY hit a one-and-a-half-month high of 112.07 earlier on Friday before pulling back somewhat. The Tenkan- and Kijun-sen lines are positively aligned, supporting the view for a bullish bias. The latter though has flatlined, signalling that positive momentum has weakened.

Overall positive US data later today – especially on the retail sales front – are expected to boost the pair. The area around the earlier recorded peak of 112.07 may act as resistance to gains, with an upside violation increasingly bringing into view the 113 round figure.

On the downside and in case of disappointing US data, the range from 111.61 to 111.24 encapsulates the Tenkan- and Kijun lines, as well as the 50- and 100-day moving average lines, and may thus be of significance, providing support to losses. At the moment, the zone around a previous high at 111.82, which also captures another top at 111.75, may be offering immediate support to losses.

Developments on the trade front can also move the pair.

{kind=link}