Here are the latest developments in global markets:

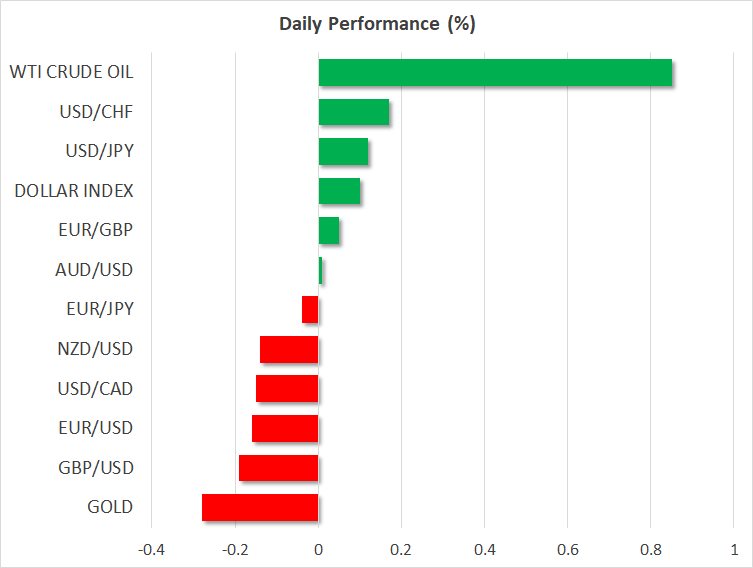

- FOREX: Dollar/yen moved off one-month lows, trading marginally up at 112.32 (+0.13%) as US 10-year Treasury yields slightly rebounded despite US President’s criticism on monetary policy and as risk aversion eased. Trade fears also somewhat calmed down after Chinese exports in September surprised analysts, showing a double-digit growth of 14.5% y/y, the highest since February, while imports appeared weaker than expected. News that the US and the Chinese President could hold a meeting in November and headlines stating that the US Treasury Department will not accuse China of manipulating its currency at its twice-yearly currency report to be issued next week were supporting sentiment. The dollar index was flat at 95.09 as the euro and the pound were giving up gains. Euro/dollar retreated to 1.1577 (-0.16%), shrugging off upbeat EU industrial production figures which returned to positive territory in August, growing about 1.0% in both monthly and yearly terms. Meanwhile speaking at the IMF’s annual meeting in Bali, ECB chief Mario Draghi reiterated that inflation risks are receding, and underlying inflation is expected to pick up steam by the end of the year, adding though that monetary stimulus is still needed. He also mentioned that a cliff-edge Brexit could potentially threaten financial stability. Although markets were positive that Brexit talks could make progress in the coming weeks, pound/dollar shifted back down to 1.3212 (-0.18%) after hitting a fresh 3-week high of 1.3258. Earlier today the British Finance Minister said that Brexit negotiations have improved pace recently, but significant differences remain to be solved. Dollar/loonie fell to 1.3009 (-0.14%). In antipodean currencies, aussie/dollar was steady, while kiwi/dollar was also down by an equivalent percentage even after New Zealand’s finance minister said that he is comfortable with the currency. In emerging markets, the Turkish lira strengthened by 1.06% versus the dollar on speculation that the American pastor detained in Turkey would probably get released soon. The South African rand was the best performer, surging by 1.38% against the greenback

- STOCKS: The calm in the markets helped European stocks to recover significantly on Friday after a strong sell-off on Thursday and before the earnings season kicks off later today, with US banks reporting earnings results for the third quarter before the US bell. At 1140 GMT, the pan-European STOXX 600 and the blue-chip Euro STOXX 50 were trading higher by 0.65% and 0.56% respectively with all sectors being in the green, though both were set to close weaker for the third consecutive week near 2-year lows. The German DAX 30 was up by 0.59%, the French CAC 40 rose by 0.76%, while the Italian FTSE MIB gained 0.66%. UK’s FTSE 100 climbed by 0.71%. In Asia, equities closed in positive territory, with South Korean stocks (+2.0%) outperforming their Japanese and Chinese rivals. In the US, stocks were ready to open strongly equities index futures suggest.

- COMMODITIES: Crude oil prices were in bullish mode on Friday but on track to mark the biggest weekly loss since February following sharp declines in the past two days. The Paris-based energy watchdog EIA cut oil demand growth forecasts for 2018 and 2019 by 0.11 million bpd to 1.28mn and 1.36mn correspondingly. The institute also said that the market is “adequately supplied” for now as the US and Russia have increased production sharply since May. OPEC also boosted production to offset shortages in Iran and Venezuela. Yet it admitted that the world’s spare capacity is already down by 2.0% of global demand. Chinese crude daily imports hit the highest in four months to build up inventories before winter trade data showed. WTI crude was up by 0.85% at $71.57 and Brent was higher by 0.47% at $80.64. In precious metals, gold pulled back from a 2 ½-month high of $1226.25/ounce to trade at $1221 (-0.22%).

Day Ahead: IMF and World meeting in focus; University of Michigan consumer sentiment pending

Friday will be relatively quiet in terms of data releases in the rest of the day, with the US being the only one to give clues on economic trends.

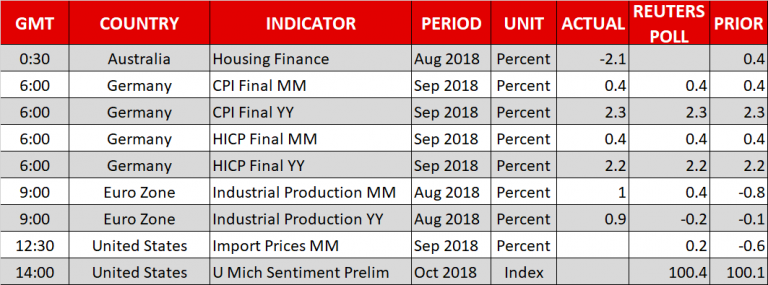

At 1400 GMT, the University of Michigan will deliver preliminary readings on consumer sentiment and inflation expectations for the month of October. Estimates on consumer sentiment are forecasting that the index might inch up to 100.4 compared to 100.1 in the previous month, while the survey related to inflation expectations will attract interest following disappointing but still strong US CPI numbers on Thursday. Earlier at 1230 GMT, US import and export prices for September will also give an indication on inflation. A weaker than expected rise in consumer prices drove the dollar lower against major currencies yesterday, with traders turning somewhat cautious about the Fed’s future rate hikes.

In energy markets, the US Baker Hughes oil rig count is due at 1700 GMT.

In terms of public appearances, Federal Reserve Bank of Chicago President Charles Evans (non-voting FOMC member in 2018) speaks on current economic conditions and monetary policy at 1330 GMT and Federal Reserve Bank of Atlanta President Raphael Bostic (voting member) participates in a discussion at 1545 GMT. Moreover, on the agenda is the Bank of England’s chief economist, Andy Haldane, who will be participating in an event at 1400 GMT.

In Bali, Indonesia, the International Monetary Fund and World Bank will start their annual meeting to discuss work on global financial and economic issues, with many influential central bankers attending the event, among them the ECB Mario Draghi who will be speaking on Saturday as well.

Traders will be watching US-Turkish political developments too, as the American pastor detained in Turkey with terrorism charges returns to court on Friday. Sources stated that a deal is likely on the table and the pastor could be released in the coming days. Note that his detention caused damage to US-Turkish relations, with the countries exchanging sanctions, and the Turkish lira plummeting in the aftermath. Any news proving speculation could boost the lira.