Here are the latest developments in global markets:

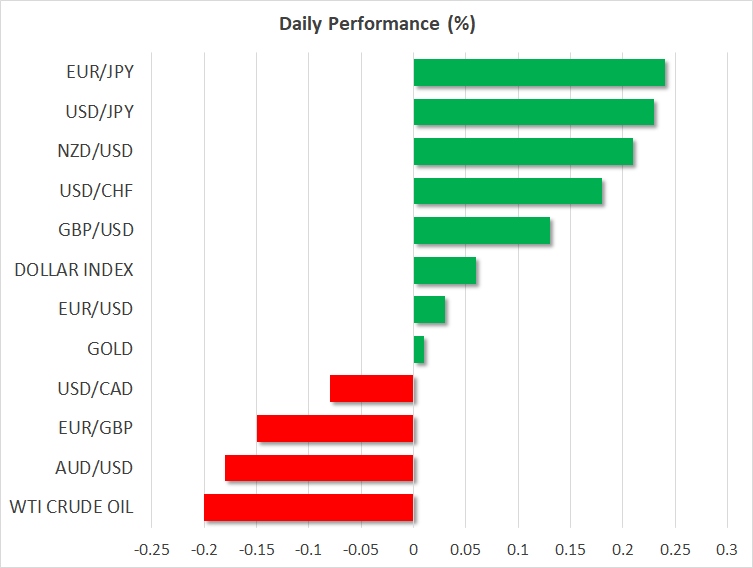

FOREX: The dollar index was fractionally higher early on Tuesday (+0.06%), attempting to recover some of the losses it posted in the previous session. Meanwhile, the yen is losing ground across the board, as a rebound in risk appetite seems to be diverting funds out of the safe-haven currency. Elsewhere, the loonie advanced despite lower oil prices, after an upbeat survey by the BoC sealed the deal for a rate hike next week in the eyes of investors.

STOCKS: Wall Street closed lower on Monday amid lingering concerns regarding elevated bond yields, with the tumble being led by the technology sector. Accordingly, the tech-heavy Nasdaq Composite (-0.88%) was the worst performer, while the S&P 500 (-0.59%) and Dow Jones (-0.35%) followed in its footsteps. Risk appetite seems to have recovered somewhat on Tuesday, as futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a positive open today. Asia was mixed on Tuesday, with Japan’s Nikkei 225 (+1.25%) and Topix (+0.74%) advancing, but the Hang Seng in Hong Kong surrendering ground (-0.46%). In Europe, all indices were set to open lower today according to futures, albeit only modestly so.

COMMODITIES: Oil gave back early gains to close the session lower on Monday, and is trading on the back foot today as well. The reversal seems owed to traders wagering that the rift between the US and Saudi Arabia over the disappearance of a journalist won’t grow much further. Indeed, President Trump implicitly said the US won’t damage its relationships with the Kingdom over such a matter, likely calming some nerves. In precious metals, gold is practically flat on Tuesday at $1,228 per ounce, holding on to the gains it recorded yesterday as the US dollar retreated. The yellow metal briefly probed the $1,233 territory, and seems to be regaining some of its haven luster in the midst of market turmoil.

Major movers: Dollar drifts lower; kiwi and loonie jump on upbeat releases

The dollar started the week on a soft note, underperforming all its major peers on Monday besides the British pound, which was on shaky legs itself amid Brexit uncertainties. There was no single fresh catalyst for the greenback’s weakness, though disappointing US retail sales data likely added some fuel to the drop.

Of note, is the fact that while the dollar had been acting as a haven asset in recent months, gaining on escalations in the trade conflict for instance, this pattern seems to have reversed in recent sessions. The US currency now appears to be positively correlated to risk sentiment, moving in the same direction as major equity indices over the past week, much like the dollar/yen pair typically does. Indeed, the dollar is a little higher today, alongside US equity futures.

Elsewhere, the pound mostly held onto its early losses , though it managed to recover against the weak dollar. While there are several UK data releases this week, including employment data today, political developments may eclipse economic ones in driving the pound, given the critical juncture the Brexit process is at. Sterling’s fortunes will likely be tied to how the EU summit plays out, and whether investors are left with the impression that a deal may be finalized in November, or not.

In euro land, Italy submitted its controversial budget proposal to the EU Commission. The ball is now in the EU’s court, which has two weeks to review it. A rejection seems almost inevitable. The most crucial variable for the euro may be whether this will morph into a full-fledged standoff, or whether both sides opt for a compromise. Separately, ratings agencies like Moody’s and S&P will be reviewing Italy’s credit position in the final week of October, with any potential downgrade likely to spell more pain for Italian assets.

Elsewhere, kiwi/dollar jumped overnight after New Zealand’s inflation data for Q3 were stronger than anticipated. In Canada, the loonie advanced despite a pullback in oil prices, after the BoC’s quarterly business outlook survey was surprisingly upbeat, adding the finishing touches to market expectations regarding a rate hike next week, now priced in with a 91% probability (Canada OIS).

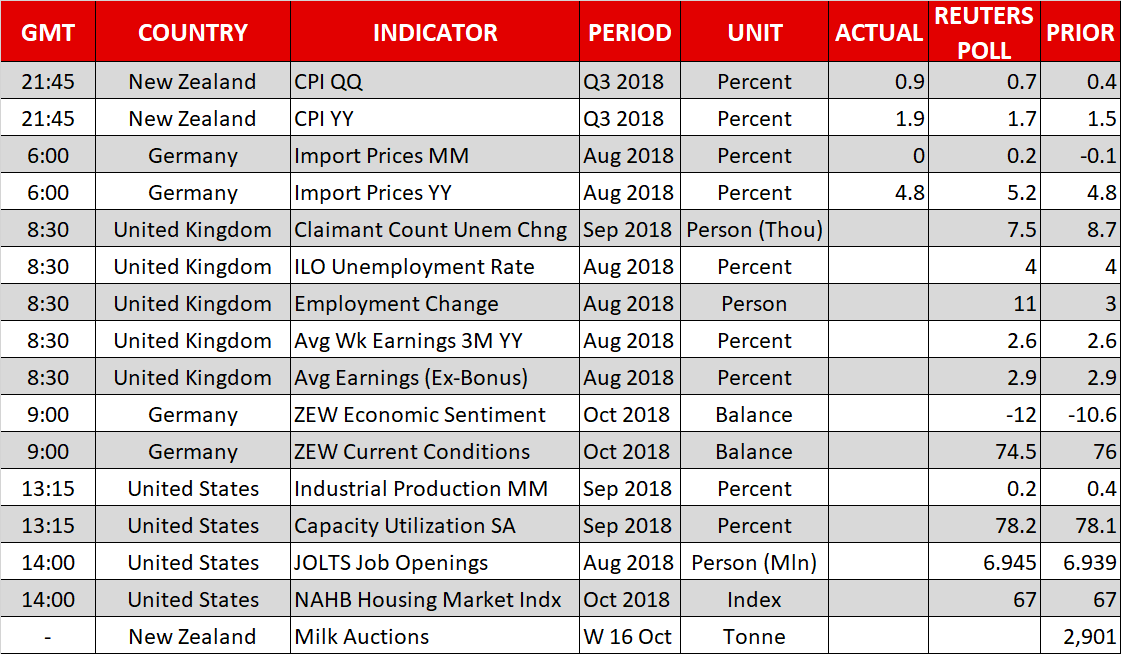

Day ahead: UK employment & Brexit in focus; German ZEW surveys, US industrial production and job openings figures also due

Key UK data on employment will be on tap on Tuesday. Meanwhile, surveys on German investor morale and US industrial output will be among releases attracting attention as well.

At 0830 GMT, UK jobs data for August, as well as September’s claimant count will be made public. Overall, projections point to a relatively strong labor report. More specifically, the unemployment rate is forecast to have remained at the multidecade low of 4.0% in August. Meanwhile, average weekly earnings in the three-months to August, both including and excluding bonuses, are anticipated to have expanded at July’s pace of 2.6% and 2.9% respectively in annual terms. The prints on wages tend to gather additional attention as they have the capacity to stoke inflation expectations.

Last month’s wage growth beat projections and employment levelled off, with the addition of just 3.0k positions in the three months to July; August’s respective number is expected to stand at 11.0k. For the record, important UK data on inflation and retail sales will follow on Wednesday and Thursday correspondingly. The figures can definitely provide near-term direction to sterling pairs. Of more significance through, are likely to prove any Brexit developments, with a crucial EU summit commencing tomorrow being eyed.

The ZEW institute’s surveys gauging investor sentiment in Germany are due at 0900 GMT. Both the economic sentiment and current conditions indices are expected to deteriorate a bit in October relative to September. Trade and political uncertainty are factors that may weigh on the readings.

Out of the US, September’s industrial production numbers are due at 1315 GMT, with a 0.2% m/m growth being expected after August’s 0.4%. Manufacturing production, a subset of industrial output, will also be monitored, especially in light of Trump’s tariff action that could affect the sector. The figures on September’s capacity utilization are slated for release at the same time.

Also out of the US, at 1400 GMT, JOLTS job openings are anticipated to come in at 6.945 million, slightly above July’s figure and at a fresh record high. October’s NAHB housing market index is also due at 1400 GMT.

New Zealand related, the outcome of today’s bi-weekly milk auction may move the local dollar, in light of the fact that dairy products are the nation’s largest goods export earner; higher prices are generally seen as kiwi-positive. The data lack a specific time of release.

San Francisco Fed President Daly, a voting FOMC member in 2018, will be giving a lecture at 2015 GMT. Elsewhere, Asia-Pacific Economic Cooperation (APEC) finance ministers will be meeting in Papua New Guinea.

In equities, BlackRock, Goldman Sachs, Morgan Stanley, Johnson & Johnson will be reporting quarterly earnings before Wall Street’s opening bell, with Netflix’s respective report hitting the markets after the market close.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT. The US-Saudi dispute over the disappearance of prominent Saudi journalist Khashoggi can also prove instrumental for oil price movements.

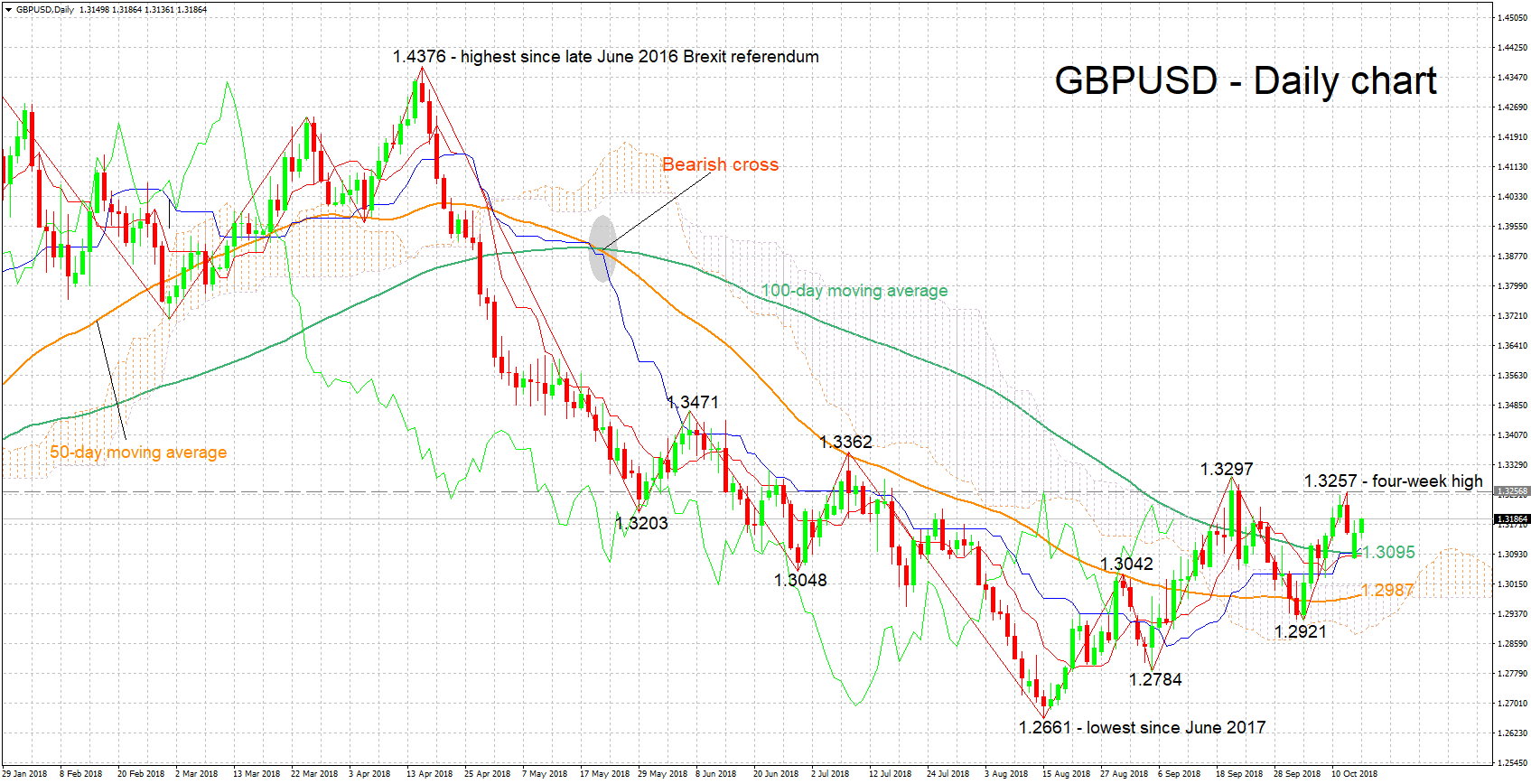

Technical Analysis: GBPUSD looking mostly neutral in the short-term

GBPUSD has retreated a bit after hitting a near four-week high of 1.3257 last week. The Tenkan- and Kijun-sen lines are negatively aligned at the moment, though they have both levelled off, overall projecting a predominantly neutral picture in the near-term.

Encouraging data releases out of the UK are likely to lift the pair. The area around Friday’s high of 1.3257 could act as resistance. Not far above lies another peak at 1.3297, while the next hurdle in the event of more bullish movement may be 1.3362, the pair’s highest since mid-June.

On the downside and in the event of weaker-than-projected readings, support could come around 1.3095. This is the current level of 100-day moving average line, with the Tenkan- and Kijun-sen lines roughly coinciding with this point. Lower still, support could come around 1.3042 – a previous top – and then from the 50-day MA at 1.2987; the zone around the latter includes the Ichimoku cloud top at 1.3011 and consequently the 1.30 round figure.

US prints and of course any Brexit updates can also move GBPUSD.