Political risk to dominate thin calendar of economic events

The US dollar will finish the week ending May 12 higher across the board against major pairs. Despite the dollar rally losing steam as softer economic data was released the U.S. Federal Reserve kept the June rate hike on the table boosting the greenback on a monetary policy divergence basis. The central banks of New Zealand and England issued statements this week and made it clear that there are no rate changes coming soon, unlike the US central bank. The miss in inflation and sales could only highlight a temporary problem as the May 7 U.S. non farm payrolls (NFP) added 211,000 jobs still points to a solid recovery.

The market is pricing in a 73.8 percent probability that when it meets on June 14 it will raise interest rates to a 100-125 basis points range. Weaker US data has brought it down from 83.1 percent yesterday but taking Fedspeak into consideration it remains a firm possibility. Federal Open Market Committee (FOMC) members have seen the number of speeches they deliver increase which better prepares the market for upcoming decisions. The FOMC meeting in March was a great example as Fed members warned investors that they were not pricing in an upcoming rate hike. The meeting in June become a test of trust. The Fed has been typically vague in their timing but is now dropping far more hints without resorting to outright guidance.

The week of May 15 to May 19 will feature little in the way of economic events. The market will focus on data out of the UK, with UK inflation to be released on Tuesday, May 16 at 4:30 am EDT and retail sales on Thursday, May 18 at 4:30 am EDT. The Bank of England (BoE) kept rates unchanged last week and the central bank issued a warning of the lack of wage growth as inflation is rising to a forecasted 2.8 percent in 2017. The BoE also reduced economic growth forecasts to 1.9 percent as the pound has been weaker ahead of Brexit.

The EUR/USD lost 0.601 in the last five days. The single currency is trading a 1.0932 after investors sold the EUR following the results of the second round of the French presidential election. The victory of Emmanuel Macron was correctly forecasted by pollsters and while the market breathed a sigh of relief it also took sold the EUR as it deemed the currency would not keep gaining ground.

Dovish comments from European Central Bank (ECB) president Mario Draghi kept the currency from appreciating versus the USD. In the other hand U.S. Federal Reserve members are keeping the June interest rate hike alive by talking about the need to act sooner rather than later and keep the hope of four rate hikes alive this year.

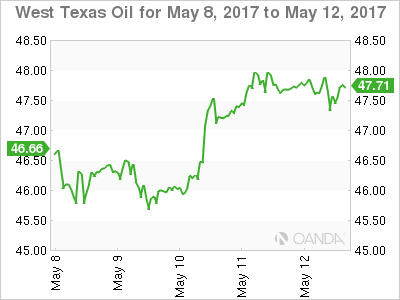

The price of crude gained 3.08 in the last week. West Texas is trading at $47.59 after a massive drawdown of weekly inventories in the US ended a string of losses for energy prices. The Organization of the Petroleum Exporting Countries (OPEC) has also been active with comments around the success of its production cut agreement and the high probability of an extension to be announced at the meeting with other major producers on May 25.

The Energy Information Administration (EIA) reported a 5.2 million barrels draw for the week ending May 5. Gasoline inventories fell by 200,000 which is feeling optimism ahead of the start of the US driving season. The drawdown in US energy stocks boosted the price of oil as it lined up with OPEC’s release of data confirming their production limits, but the fact that there is low demand for energy and US producers, not bound by any agreement, are ramping up production to take advantage of current price levels will keep the price of crude volatile.

The USD/MXN lost 1.372 percent in the last five days. The currency pair is trading at 18.7523 after the political uncertainty in the US is removing downward pressure on the Mexican currency as the topic of trade and immigration is not top of the US political agenda until the turmoil in the White House can be resolved. Oil prices have also boosted the performance of the peso with lower inventories in the US driving crude prices higher. Mexico is part of the OPEC production cut and is expected to take part in the extension that will be announced on May 25.

The MXN was trading higher after the disappointing sales and inflation data out of the US on Friday morning. The Mexican peso went form being one of the worst performers during the US presidential elections and up to the inauguration of Donald Trump, only to quickly regain ground in 2017. Economic fundamentals have not changed much in that time frame, but political risk and risk aversion have dictated the price of the peso as it is used as proxy for other emerging market currencies.

Market events to watch this week:

Sunday, May 14

- 6:45 pm NZD Retail Sales q/q

- 10:00 pm CNY Industrial Production y/y

Monday, May 15

- 9:30 pm AUD Monetary Policy Meeting Minutes

Tuesday, May 16

- 4:30 am GBP CPI y/y

- 8:30 am USD Building Permits

- 6:45pm NZD PPI Input q/q

Wednesday, May 17

- 4:30 am GBP Average Earnings Index 3m/y

- 8:30 am CAD Manufacturing Sales m/m

- 10:30 am USD Crude Oil Inventories

- 9:30 pm AUD Employment Change

- 9:30 pm AUD Unemployment Rate

Thursday, May 18

- 4:30 am GBP Retail Sales m/m

- 8:30 am USD Unemployment Claims

Friday, May 19

- 8:30 am CAD CPI m/m

- 8:30 am CAD Core Retail Sales m/m

*All times EDT