Here are the latest developments in global markets:

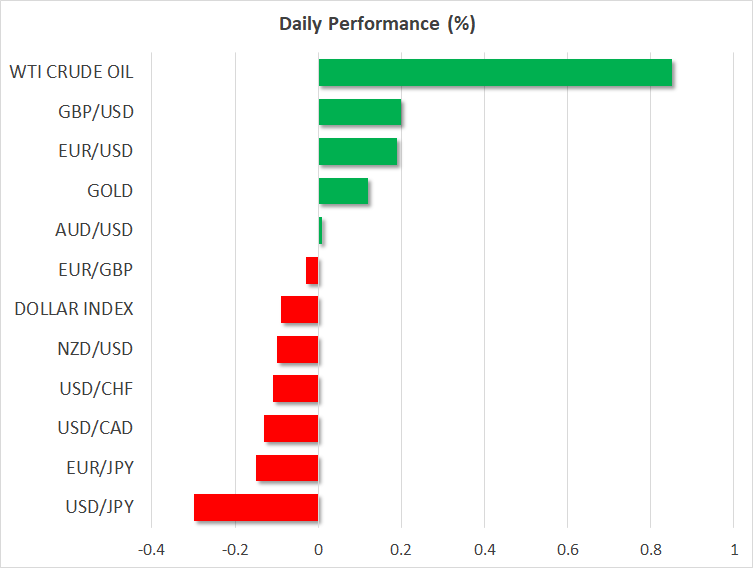

FOREX: The British pound plunged on Thursday after the UK Brexit Secretary quit in protest of the Brexit deal, and amid growing speculation PM May could soon face a leadership challenge. Meanwhile, the commodity-linked currencies – aussie, kiwi, and loonie – all gained ground on the back of a report that the US will pause its next round of tariffs on China. The dollar was little changed, unable to draw much strength from a beat in US retail sales data.

STOCKS: Wall Street pared early losses to close in the green on Thursday, following a report that the next round of US tariffs on Chinese goods had been put on hold. While that was later refuted by the top US trade official, markets largely held on to their gains. The tech-heavy Nasdaq Composite outperformed (+1.72%), while the S&P 500 (+1.06%) and Dow Jones (+0.83%) followed in its tracks. Asia was mixed on Friday, with Japanese indices posting moderate losses but Chinese markets inching higher. Meanwhile, all European benchmarks were set for a higher open today, futures suggest.

COMMODITIES: Oil prices rebounded on Thursday and are extending their recovery today, disregarding a bigger-than-expected build in the EIA weekly inventory data. It may be that investors largely anticipate strong inventory builds going forward as the “oversupply theme” has dominated for a while, or that continued speculation for OPEC supply cuts overshadowed stockpile considerations. WTI is currently trading at $57.35 a barrel, and Brent at $67.62. In precious metals, gold prices are a little higher at $1,216 an ounce today (+0.11%), looking set to post a fourth session of advances. Technically, bullion is trading within a symmetric triangle formation, with a break on either side needed to determine the short-term bias.

Major movers: Sterling crashes as Brexit Secretary quits; antipodeans cheer trade news

The British pound slumped on Thursday, in another hectic session marked by a relentless barrage of Brexit-related headlines. Sterling/dollar plunged from near 1.3000 to stabilize around 1.2790, following news that the chief UK negotiator in the EU-UK talks, Brexit Secretary Raab, had resigned – citing “fatal flaws” in the deal. Clouding the political landscape further, reports continue to suggest PM May might soon be faced with a motion of no-confidence by members of her own party. Summarizing, it’s becoming increasingly evident to investors not only that Parliament will likely reject the Brexit deal as things stand, but that Theresa May could also have a Tory mutiny on her hands before long.

Hence, political uncertainty may be set to heighten even further, which in isolation is negative for the pound. The caveat is that if May’s position weakens enough to make a General Election more likely, that may actually prove positive for the pound as the probability for a second referendum may rise in tandem, assuming a Labour government takes power for instance.

Outside of the UK, global risk appetite rebounded on a report that the top US trade official, Robert Lighthizer, told industry executives the next round of tariffs on China had been put on hold. US equity indices jumped to close higher, while risk-sensitive currencies such as the aussie and kiwi outperformed. Funnily enough, while Lighthizer later denied the report, investors apparently didn’t take his words at face value, as markets did not retrace much. All eyes remain on the Trump-Xi Jinping meeting later this month, where expectations are riding high that a “trade ceasefire” may be called.

Flying under the radar, the euro outperformed all its major peers outside of the aussie and kiwi, even despite Brexit worries dominating headlines. It seems that “no news is good news” in Europe presently, as markets await to see whether the EU-Italy standoff will morph into a full-fledged conflict, given Italy’s adamancy to stick to its deficit targets.

Day ahead: Brexit firmly in focus; eurozone final inflation figures and US industrial & manufacturing output on tap

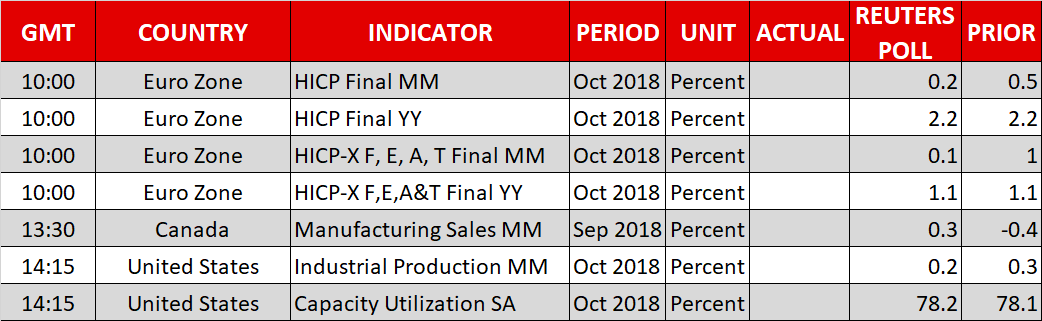

Friday’s economic calendar is relatively light, with revised inflation readings being due out of the eurozone and the US being on the receiving end of prints on industrial and manufacturing production. Beyond releases, Brexit will remain firmly in focus.

Sterling will likely stay hostage to UK political and Brexit developments. Thursday saw the resignation of key ministers from PM May’s government over her Brexit plan, while there are efforts to topple her leadership via a no confidence vote. Consequently, sterling crashed across the board. May’s efforts to ‘sell’ her plan to parliament will be monitored, though the odds she passes it look somewhat remote at the moment, given there’s hostility from opposition as well as Tory lawmakers.

It is notable that the latest twists have led market participants to price out a quarter percentage point rate hike by the Bank of England in 2019.

Final October inflation readings out of the eurozone are due at 1000 GMT. Barring a significant deviation from the flash estimates, which tend to be fairly reliable, the euro is not likely to react much to the numbers. The headline Harmonised Index of Consumer Prices (HICP) is expected to be confirmed at 2.2% y/y, above September’s 2.1%, while core HICP that excludes food, energy, alcohol and tobacco from its calculations is forecast to come in at 1.1% y/y, above the previous 0.9%.

News relating to the EU-Italy budget standoff perhaps have greater capacity to move the euro rather than today’s inflation prints. In this respect, reports saying that Italian PM Conte was looking to work with the EU over his government’s 2019 budget are seen as euro-positive, given they deviate from the previous confrontational rhetoric. The differences between the two sides may not leave much room to maintain the positive momentum for much longer though.

Out of the US, industrial and manufacturing output figures for October will be hitting the markets at 1415 GMT. Industrial production growth is anticipated to expand by 0.2%, slower than September’s 0.3%, though it is of note that this would mark its fifth straight month of increases. Data on October’s capacity utilization are due at the same time.

On the Sino-US trade dispute, China appears to be proceeding with concessions to US demands that may pave the way for a meaningful de-escalation of tensions.

Canadian manufacturing sales for September are due at 1330 GMT.

ECB chief Mario Draghi will be giving a speech at 0830 GMT, with Bundesbank President and ECB policymaker Weidmann making a public appearance at 1300 GMT. Meanwhile, non-voting FOMC member in 2018 Evans will be participating in a Q&A session at 1430 GMT.

In energy markets, Baker Hughes data on active oil rigs in the US are due at 1800 GMT.

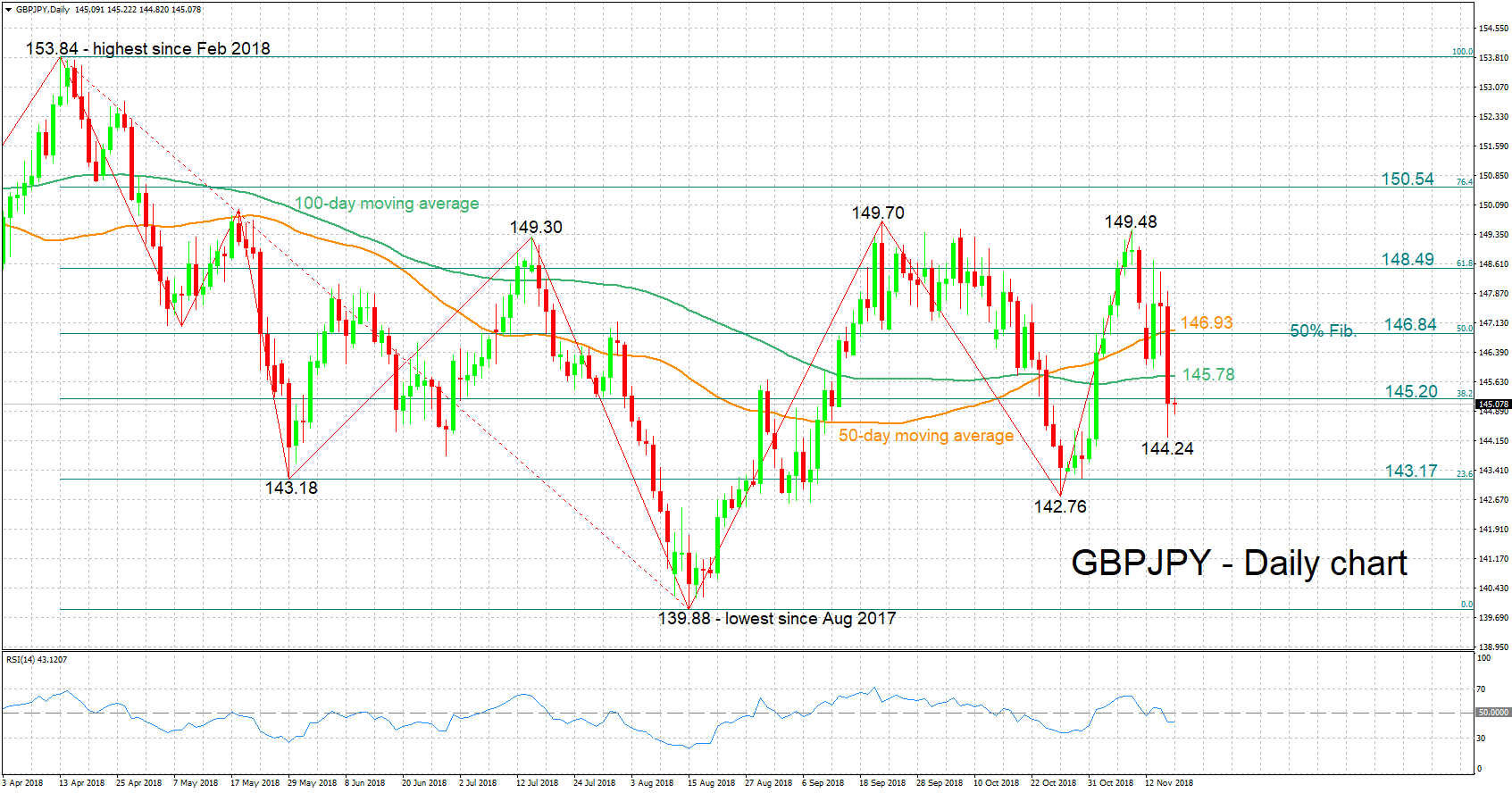

Technical Analysis: GBPJPY momentum moves to the downside

GBPJPY reversed course after rising to its highest since early October of 149.48 last week. On Thursday, it hit a two-week low of 144.24. The RSI has been heading lower in recent days, entering bearish territory below 50 and suggesting a negative bias in the short term. Notice though that it has stalled its decline, which may be an early sign of weakening negative momentum.

More Brexit complications are likely to push the pair even lower. Support to losses may occur around yesterday’s low of 144.24. Further below, additional support could emerge around 143.17, the 23.6% Fibonacci retracement level of the downleg from 153.84 to 139.88. Notice that a couple of bottoms from previous months at 143.18 and 142.76 lie close to the 23.6% Fibonacci point. Steeper losses would increasingly bring within scope 139.88, the pair’s lowest since August 2017.

Conversely, receding uncertainty is expected to support GBPJPY. Immediate resistance could take place around the 38.2% Fibonacci mark at 145.20, with the 100-day moving average line at 145.78 being part of the area around this level. Higher still, the zone around the 50% Fibonacci at 146.84 would be eyed; the 50-day MA at 146.93 is also part of this zone. More bullish movement would turn the attention to the 61.8% Fibonacci point at 148.49.

{kind=link}