- Dollar upswing continues unabated, but caution gradually warranted

- US stocks retreat after soft data, Chinese markets up on stimulus news

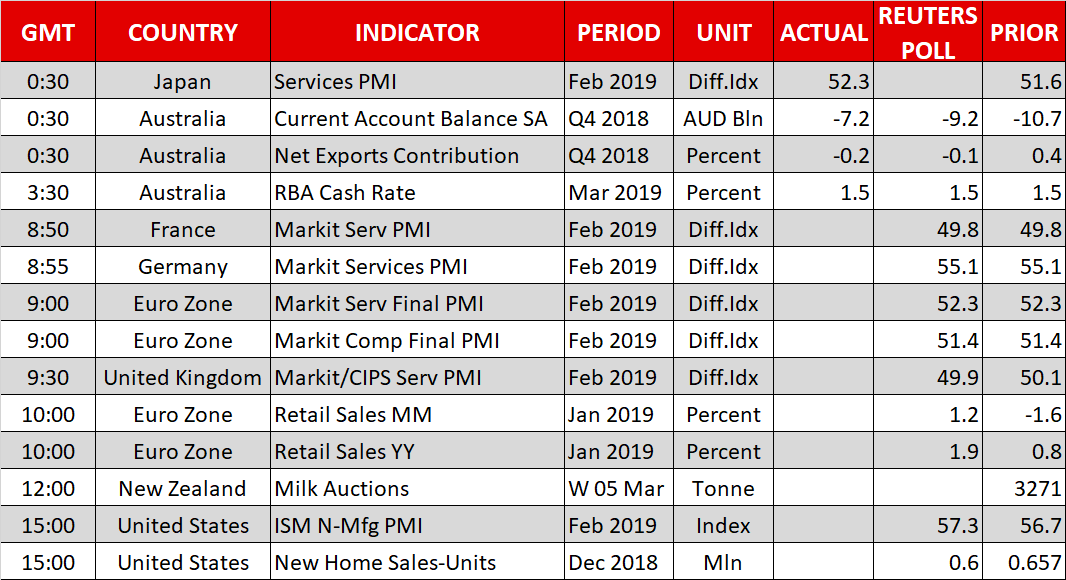

- RBA stays on hold, aussie yawns

- UK services and ISM non-manufacturing PMIs coming up today

Dollar rally in full throttle, but speed bumps may lie ahead

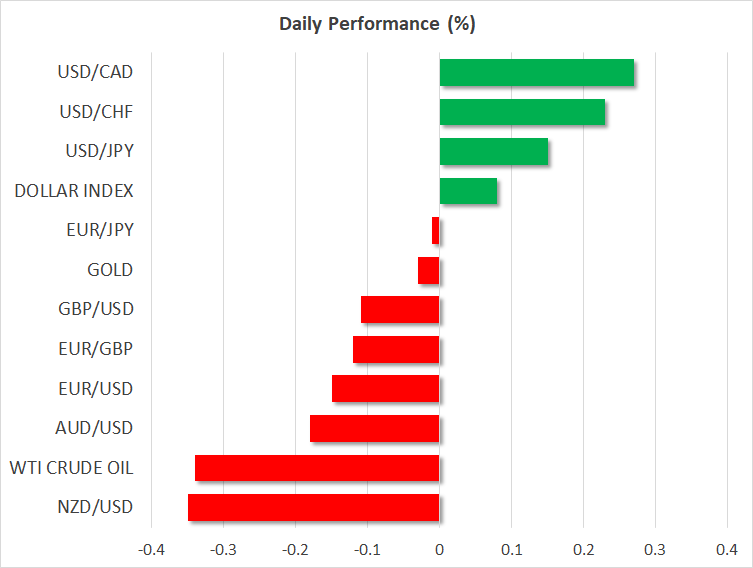

The US dollar registered another session of strong gains to kick off the week, gaining ground against all its major counterparts besides the defensive Japanese yen, which was the best performer as risk sentiment turned sour. The dollar seems to have attracted some defensive flows itself, considering that it advanced without any positive news and even as the yields on US Treasuries retreated – once again demonstrating its unparalleled ability to act both as a safe-haven and a carry currency.

The US fundamental picture remains bright for now, as even accounting for the latest slowdown, the American economy is still easily outgrowing its G10 peers. Alas, that doesn’t mean it’s all plain sailing higher from here for the dollar. Declines in euro/dollar in recent months have consistently run into an impenetrable wall of buy orders around 1.1250, which is owed to the slightly narrower spread between short-dated US and EU bond yields since November, de-facto keeping a floor under the pair. This implies that even if euro/dollar sellers manage to push the pair towards the November lows near 1.1213 – for instance on the upcoming ECB meeting – they will likely have a difficult time piercing below that level, and may require a greater catalyst to do so.

Stock markets pull back after testing key resistance areas

US equity markets closed in the red on Monday, with both the S&P 500 (-0.39%) and the Dow Jones (-0.79%) retreating after challenging some crucial resistance zones that capped the rally in these indices back in November. The trigger for this retreat seems to have been the US construction spending print for December, which fell unexpectedly, igniting speculation for a downward revision in the Q4 GDP. Some headlines that House Democrats are opening an investigation into whether the Trump administration engaged in obstruction of justice may have contributed too, via amplifying political uncertainty.

Across the Pacific Ocean, Asian markets are mixed on Tuesday. Whereas Japanese indices are lower, Chinese ones are notably higher, extending their spectacular year-to-date gains. The latest leg higher was seemingly fueled by hopes for more stimulus, following overnight announcements at the National Congress tax cuts across the board, for instance on VAT. Yet, stock gains were likely kept in check by signals that this will be a measured dose of stimulus aimed at avoiding a more severe slowdown, as opposed to a “deluge” of stimulus to re-accelerate growth.

No material news from RBA meeting, aussie snoozes

Overnight, the Reserve Bank of Australia (RBA) kept its policy unchanged once more, providing practically no new information. Although the accompanying statement did contain some more optimistic language, on the margin, there was nothing noteworthy enough to trigger any market reaction. Looking at market pricing, a 25bps rate cut by year-end is still priced in with an 85% probability. As for the aussie, the next market mover may be a speech by RBA Governor Lower today, at 22:10 GMT.

Coming up: UK services PMI and US ISM non-manufacturing index

It will be another (relatively) light day in terms of economic releases, with the most noteworthy indicators coming out of the UK and the US.

In the UK, the services PMI for February is expected to have entered contractionary waters, below 50, highlighting that Brexit uncertainties are starting to bite. Some comments by BoE Governor Carney at 15:35 GMT could be important for the pound as well.

In the US, the ISM non-manufacturing PMI for February is due, with some remarks by regional Fed Presidents Rosengren (12:35 GMT) and Kashkari (14:30 GMT) also attracting attention.

{kind=link}