- NFP – Jobs data wipes all rate hike expectations

- USD – Dollar bottom may be in place

- China – Trade emphasizes need for a trade deal

- Oil – Norway’s fund concerned of permanent decline in prices

NFP

The US dollar and equities plummeted after the US nonfarm payroll report posted the weakest reading since the fall of 2017. US hiring in February only saw 20,000 jobs created, much lower than the 180,000 eyed by analysts. The unemployment rate also declined from 4.0% to 3.8%, very close to the 1969 low of 3.7%. The closely watched wage data impressed as the annual reading rose 3.4%, the highest level since financial crisis. Housing also provided a positive picture with housing starts recapturing the 1.2 million mark.

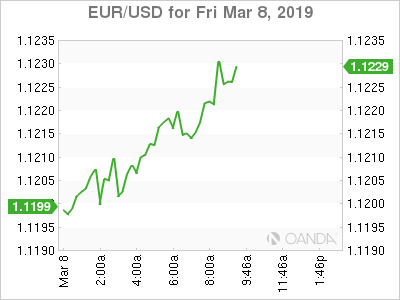

USD

Safe haven assets rallied with the yen being the biggest beneficiary. The dollar also weakened against the euro after initially tentatively breaking below its key range, a possible sign that we could see a key bottom in place. With rate hikes off the table for the Fed, many may look to see if we are at the beginning of a major pullback.

China

February’s Chinese trade data was much worse than expected, highlighting the effects from the trade war. Analysts are focusing on the 20.7% drop in exports, much worse than the expected 5% decline. The trade deficit narrowed to $4.12 billion compared to an expected $26.2 billion and imports fell 5.2%, worse than the analysts’ forecast of a drop of $0.6 billion.

The softer than expected Chinese trade data emphasizes the need for China to end the trade with the US. The NPC’s policy summit unveiled fiscal stimulus and while the market is also expecting monetary stimulus with cuts to interest rates, we may see China hold off on the monetary stimulus until they see the market reaction to a trade deal.

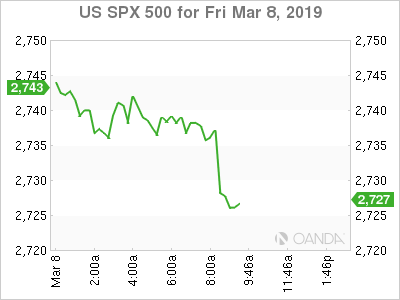

Stocks

US equities are poised to open significantly lower following a poor jobs report. The soft jobs number removed all expectations for a rate hike. The Fed Funds futures now see a 25.4% chance of a rate cut in the January 2020 meeting. The Fed’s dovish pivot is likely not going to be enough of a reason for investors to buy the dip. The pressure continues to grow for a trade deal to be reached.

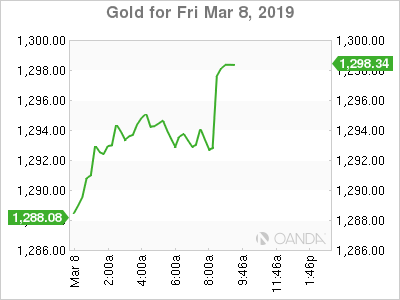

Gold

The precious metal rebounded sharply after a poor US jobs number triggered safe-haven demand. Gold prices may have formed a key bottom and could continue to benefit if markets are ultimately disappointed in the framework agreement the US and China come up with.

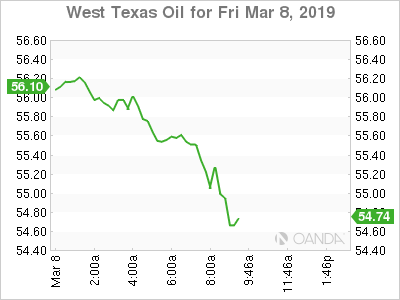

Oil

This week crude prices are struck in the narrowest range seen since December 2017. Oil was lower early on the session as global growth concerns remain the dominant theme in financial markets and prices should be capped as US production continues to rise. The other driver for lower oil prices came after Norway’s Sovereign Wealth Fund announced they will be abandoning many of their oil equity positions, they will maintain positions in Norway’s Equinor.